Everything started off well following last week’s quarterly expiries. Even the Fed’s downward revision of U.S. GDP growth—underscoring the policy risks posed by the Trump administration, not just to the American economy but to the global order—wasn’t enough to derail things. Markets edged higher, drifting without a clear direction until… patatra.

By Friday, the S&P 500 had dropped 2.5%, the Nasdaq more than 3%, and here we are again—dangerously close to correction territory.

The VIX jumped 3 points, finishing the week just below 22.

At this point, it’s clear we’ll have to get used to these whipsaw moves to the downside until there’s more clarity on multiple fronts. On Friday, core PCE inflation came in slightly higher, but what really rattled the market was confirmation of the dismal consumer sentiment reading from the University of Michigan. A typically unremarkable number (the revision, not the number itself), but this time, it sent a chill down traders’ spines and accelerated the sell-off—a reflection of the broader mood.

And yet, the paradox remains: while the most seemingly innocuous data points keep sending the market another leg lower, traders still refuse to buy hedges—until, suddenly, they wake up.

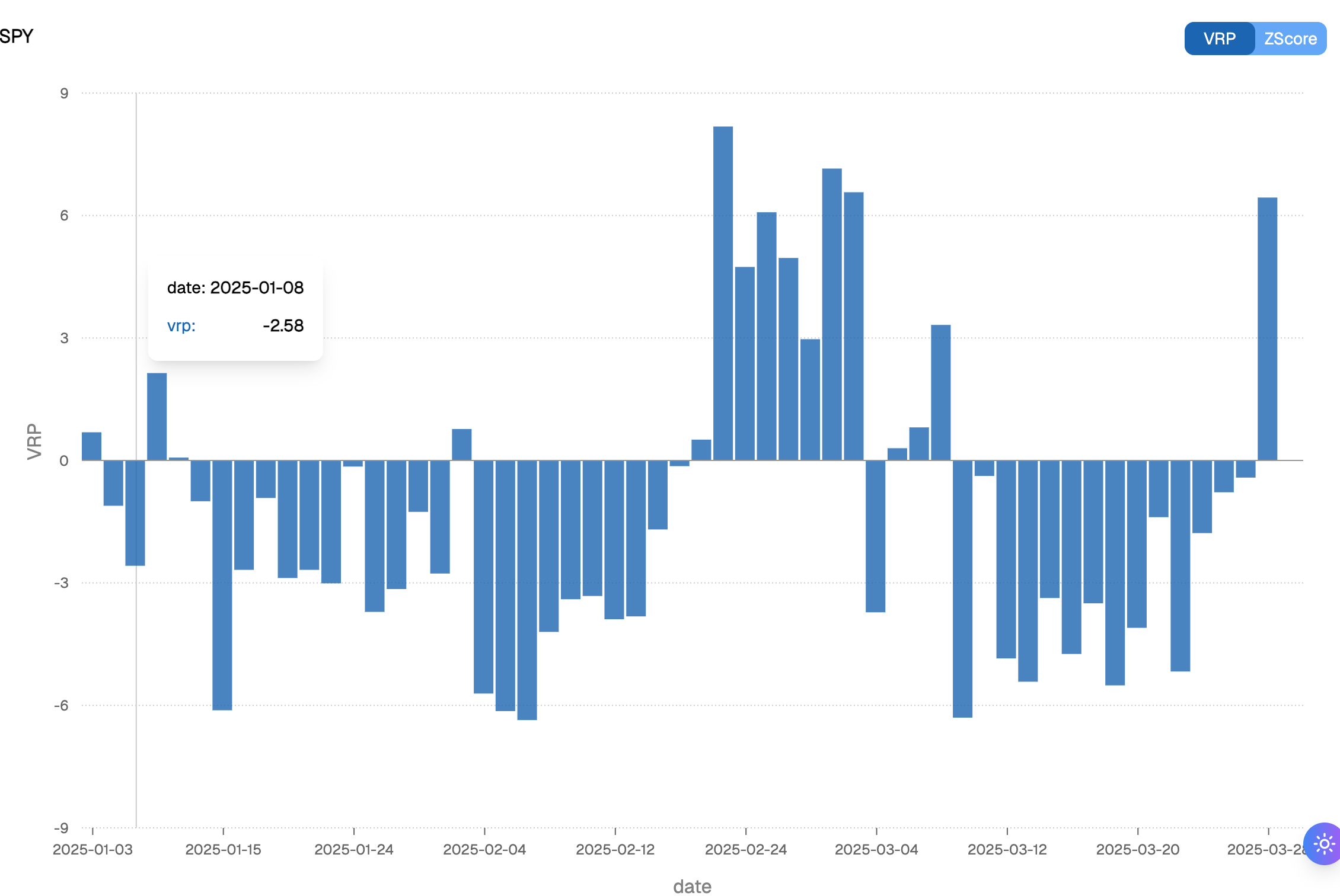

A quick rewind of the 30-day VRP over the past three months tells the story. After January’s complete denial, VRP came roaring back in February to early March—only to vanish again, creating some solid long-volatility opportunities. Those trades paid off handsomely on Friday and could extend into next week if realized volatility continues expanding. With quarter-end flows on Monday and NFP on Friday, there’s no shortage of catalysts, keep that in mind.

But let’s not get ahead of ourselves. At this stage, a full-blown panic is unlikely, and the moment VRP returns, the usual crowd of vol sellers—ourselves included—should be back in force, ready to (re)sell the very options the market wanted nothing to do with just a week ago.

So, what do we make of this? Last week, we took the easy, comfortable route: the trade is overcrowded. But this is a marketplace—it takes two to tango. While excess supply is a plausible theory, we can’t ignore the other side of the equation: a lack of demand may be just as much to blame.

Think of it this way—why would a fund manager buy options if they’ve already decided it’s time to trim exposure? If they started selling in December, they’ll keep doing so for as long as they feel like prices do not reflect the current economic reality. But when you’re divesting, you don’t need protection because you’re not planning to hold.

Put even more simply: if you’re selling your house, why would you keep buying insurance on it?

That is to us a much more reasonable explanation as to why VIX isn’t blowing off the chart right now (yet) or why it wasn’t in 2022. There is some truth behind the “orderly fashion sell off” - if you sell because you are not interested in the assets anymore, you don’t need to buy insurances as much as you would in other circumstances.

That’s just a hypothesis we had to put out there—not only because last week’s argument didn’t fully satisfy us, but also to get a better read on what the biggest market movers are thinking. Sure, VIX at 21 on a Friday might feel a bit unsettling, but a 3-point jump on the back of bad data, landing at 21.65, isn’t exactly outrageous either.

Let’s state the obvious—we have absolutely no desire for a repeat of 2022, where realized volatility stayed elevated and VIX hovered in the high 20s to low 30s for extended stretches. If you found early March exhausting, you haven’t seen anything yet. And frankly, we wouldn’t wish that kind of environment on retail traders—especially beginners—where the constant mood swings aren’t just disheartening but also… pretty expensive.

Still, we have to trade. Partly because we’re degenerate gamblers, but also because some opportunities are just too good to pass up—and, frankly, much easier to execute. Lately, we’ve seen a resurgence of structures offering protection across different corners of the market, particularly calendar spreads. We’ve long encouraged their use to ensure you're always covered.

But there’s another effective—and often misunderstood—way to trade calendar spreads, especially in the retail trading community. Selling short-term volatility while hedging with longer-term volatility is essentially a bet that short-term vol will converge to the actual realized volatility faster than longer-term vol.

This setup tends to be especially profitable in markets where the volatility term structure remains in contango. And interestingly, it’s the very mechanism behind the ever-popular “short VXX” trade—one that traders love to discuss.

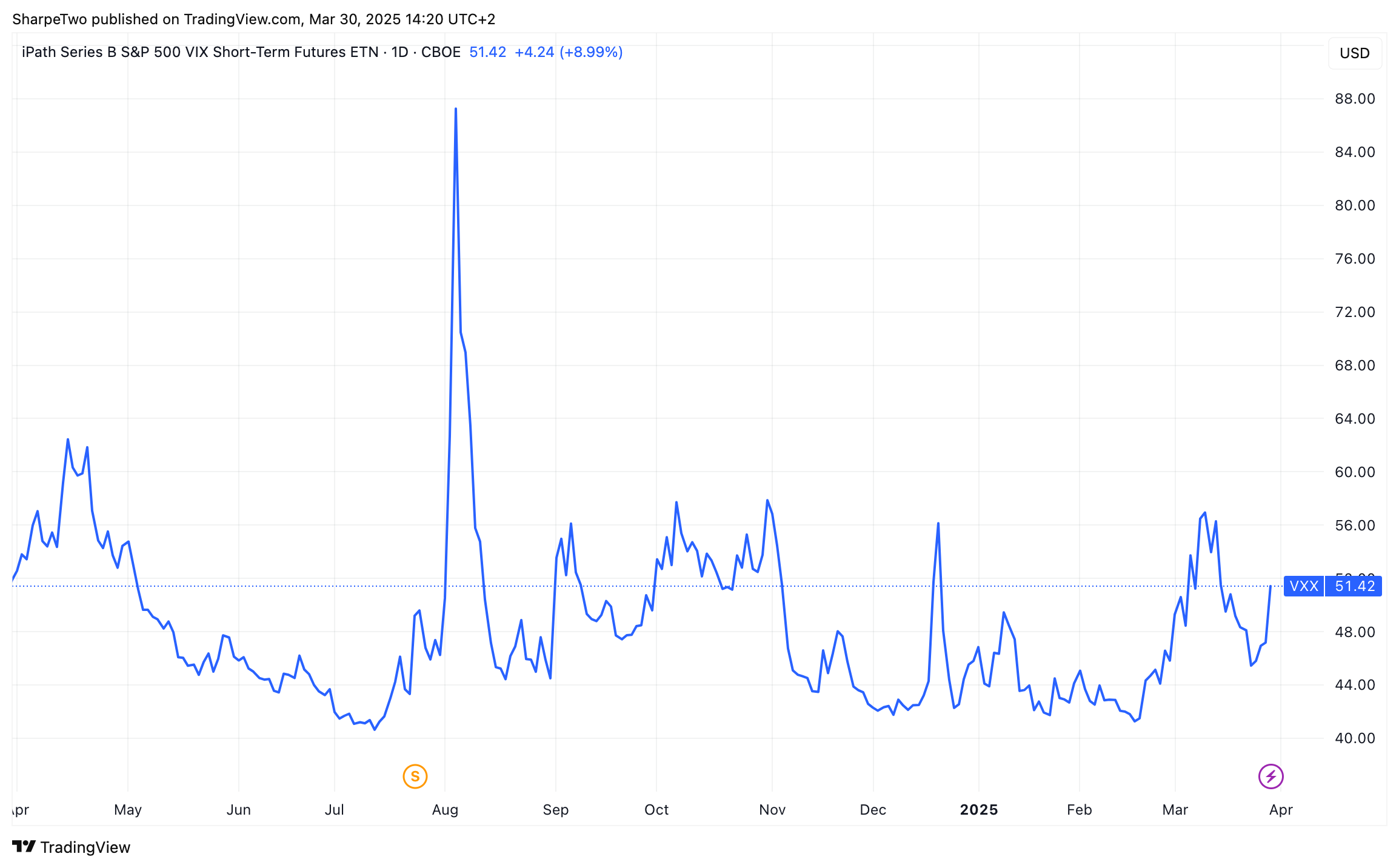

But why does VXX typically decline, and why has it struggled to do so recently?

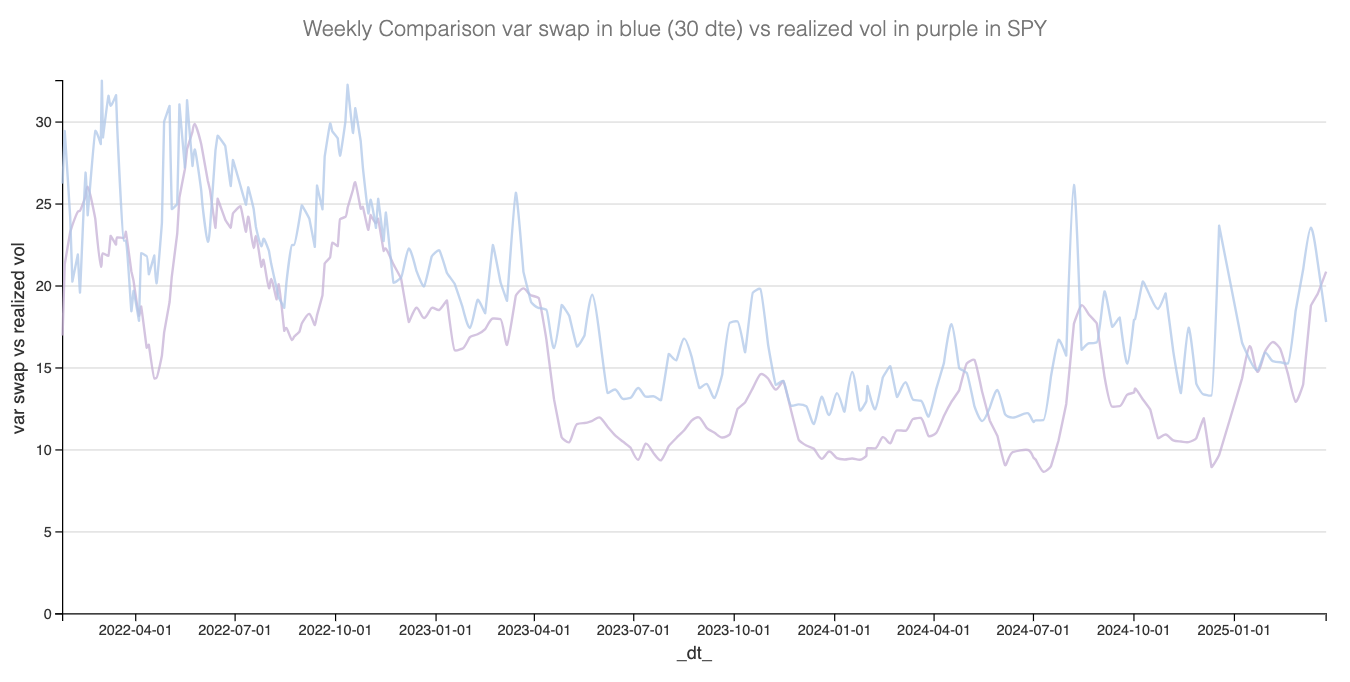

VXX’s mandate is straightforward: it systematically sells short-term VIX futures while buying longer-dated futures, continuously rolling these positions to maintain exposure to implied volatility. The unintended consequence? A persistent performance drag whenever volatility markets are stable or in contango. Simply put, in contango conditions, the fund keeps selling cheaper short-term futures and buying more expensive long-term futures—a structural headwind that steadily grinds VXX lower under normal market conditions.

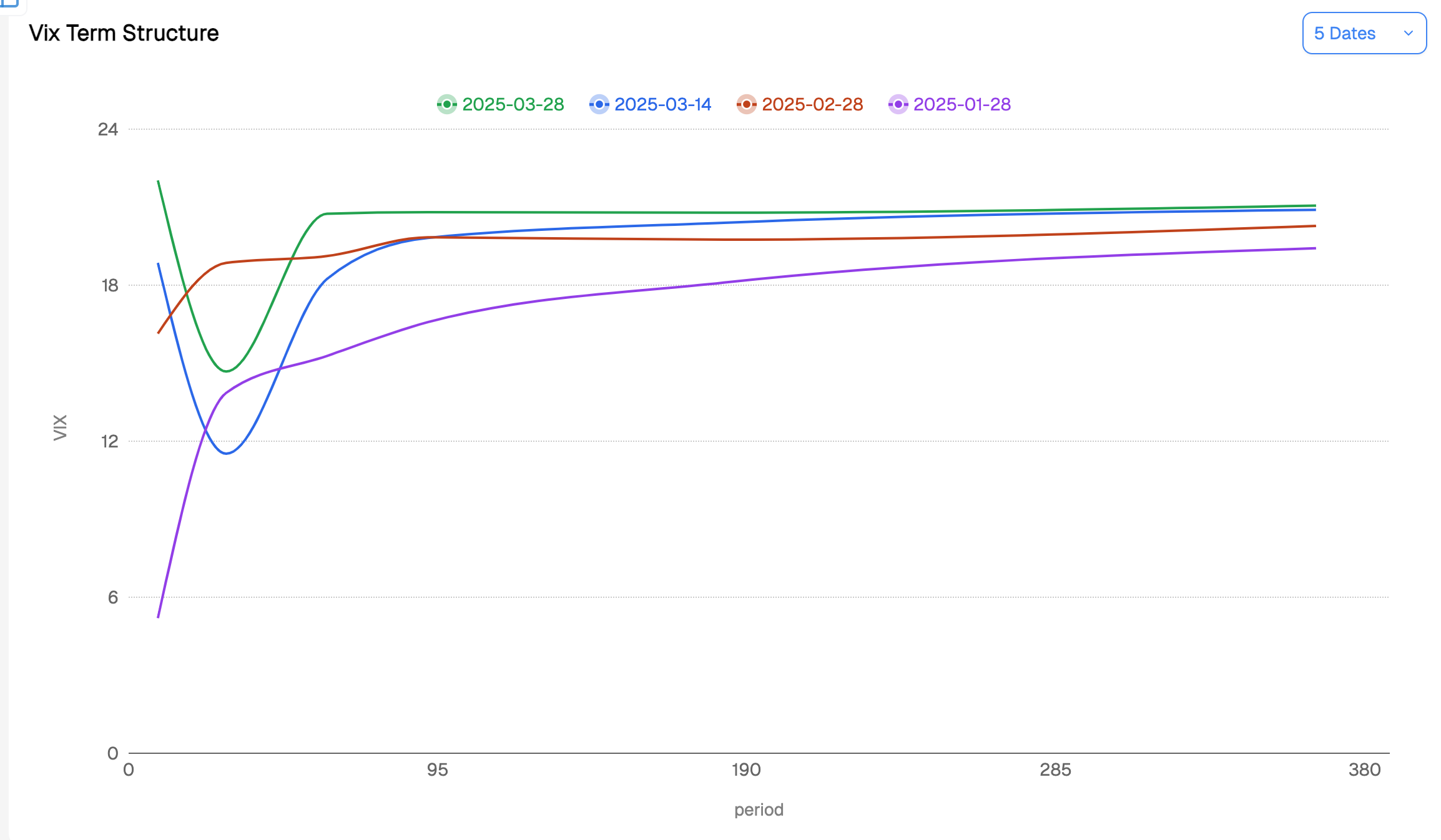

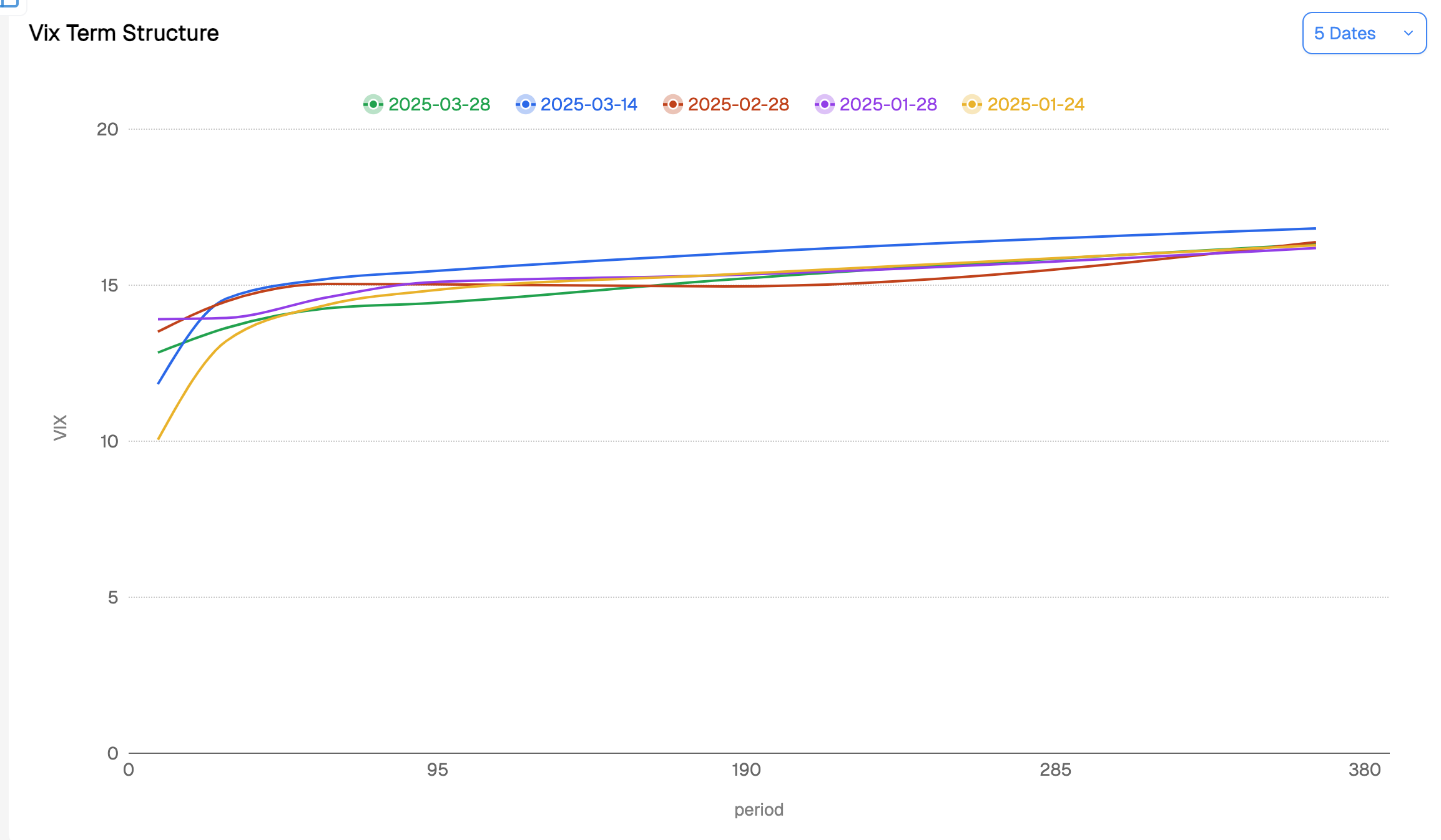

And that’s precisely why VXX has remained unusually stable over the past six months. The VIX term structure has been as flat as a North Dakotan pancake, eliminating the usual drag. If you’ve struggled with this strategy lately, you’re not alone—any market exhibiting a similarly flat term structure has been a tough environment, and… well, you guessed it, U.S. equities fit that bill perfectly.

But it turns out there’s a big winner in the midst of Trump-induced chaos. Well, actually, two.

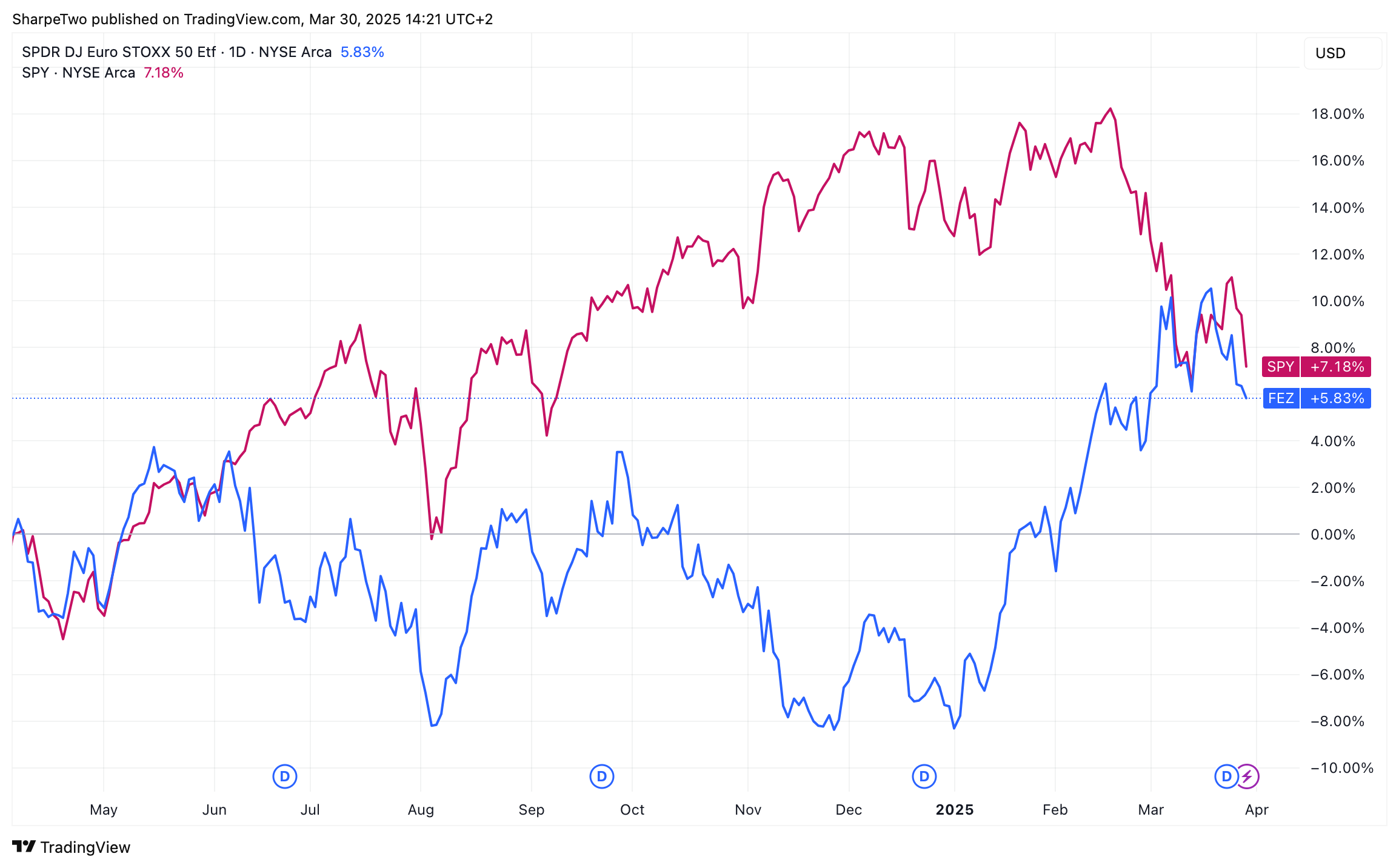

Ironically, Europe. While Americans busy themselves trashing it in their more or less private Signal groups, Europe is… moving. We’re not saying they’re out of the woods—not by a long shot—but the market is taking notice. Not only has European performance outpaced its American counterparts in recent months, but its volatility term structure has also remained smooth and stable—at least, as long as you avoid the very short end (sub-21-day options), which remain hypersensitive to fresh geopolitical headlines.

The other winner? Bonds. While everyone’s been caught up adjusting their equities exposure, the bond market has been remarkably stable. And with the term structure’s steep contango, it’s shaping up to be a perfect slope for a well-placed calendar spread.

We know ski season is coming to an end, but if you’re still looking for the right slope to ride, this vintage trade might be just the thing—low maintenance, easy to manage, and with the kind of gradient that tends to print nicely.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In other news

When it’s not about Trump, it has to be about Musk. And today, buried in a tiny Financial Times note, we got confirmation of something we’ve long suspected—Musk has officially sold X (formerly Twitter) to his AI group for the modest sum of $45 billion. Technically, he can book a profit on the deal, but that’s not where the real story—or rather, the real confirmation—lies.

Back in 2022, plenty of people scratched their heads when he decided to buy Twitter for $44 billion. And in hindsight, many (mostly correctly) point out that it turned out to be the perfect investment for influencing the presidential election. But we can’t help thinking there was something else at play. Six months before the release of ChatGPT—a project Musk, as a founder of OpenAI, was almost certainly aware of—he urgently needed access to something… a massive human-generated dataset, much like the one OpenAI used to train its own models.

Wondering how Grok took a massive leap forward over the last year? Now, with this transaction finalized, the objective is official—X’s text, images, and videos will be used to train the very same AI models Musk hopes will let him compete with Anthropic and the rest.

Thanks for sticking with us until the end. As always, here are a few good reads from last week:

- When speaks, we listen. That hasn’t changed. Here’s her latest piece on stagflation risks and the Fed’s possible course of action—a must-read.

- We may be degenerate gamblers, but we still have a heart. Here’s a touching story from , reminding us of what truly matters.

- And as a bonus—a great video on vol trading.

That’s it from us this week. Wishing you a great (NFP) week ahead and, as always, happy trading.

Ksander