A casual 300-point rally in 5 sessions, a VIX dipping into the 14s, and 4 overnight gaps exceeding 0.5%—what happened to Pessimism Central? Vanished. Disintegrated. Annihilated. Since the inflation report came in softer than expected, and with growing sentiment that Trump’s policies might not be as detrimental as initially feared, US equities have been carried along by a euphoric rhythm.

This is why we love the market: never dull, never married to yesterday’s opinion, and certainly never accountable for what was fervently priced just a day prior. Who cares about yesterday anyway? It doesn’t put food on the table.

Yet, this morning, we’re bringing you a long volatility trade. Not because we foresee a collapse into tears and chaos (that’s not really our style), but simply because the market has been moving quite a bit—up, down, and everywhere in between—while implied volatility remains stubbornly low.

Let’s dive in.

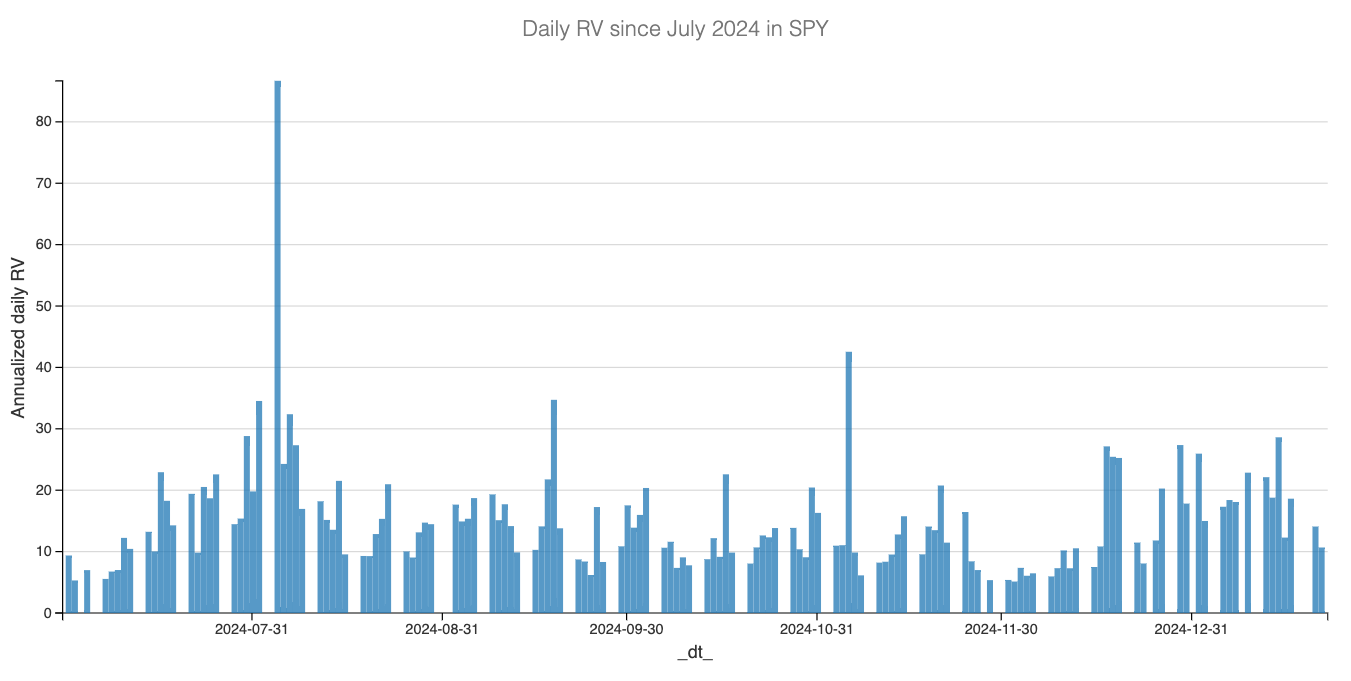

Usually, volatility is more closely associated with dramatic downside moves and less so with upward momentum. Yet, despite the serious mood improvement sparked by last week’s not-worse-than-expected inflation numbers, realized volatility has come down but still remains elevated.

Yesterday marked the first session where realized volatility dipped just above 10%, significantly lower than the 17% average observed over the past six weeks. Still, these numbers remain high compared to what “calm” looked like in 2024. And while longer-term realized volatility is gradually easing from last week’s peaks, we don’t anticipate it settling at 11% anytime soon.

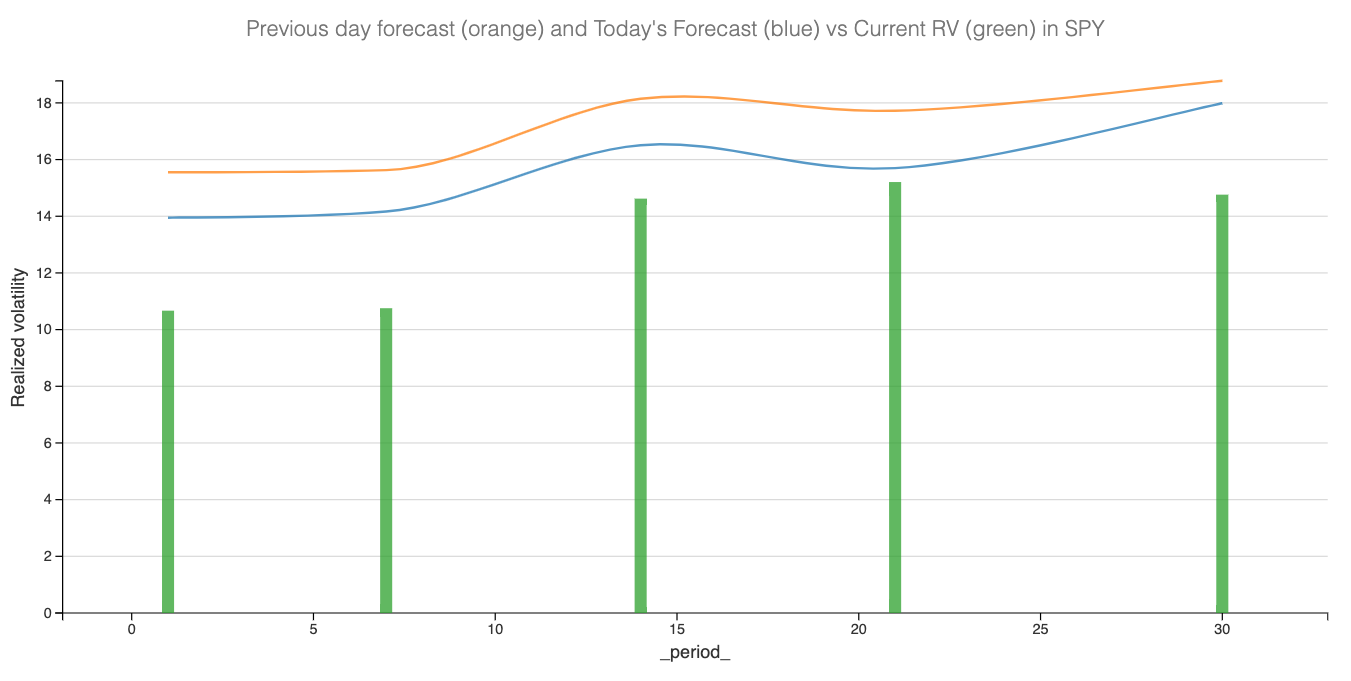

Of course, there’s no guarantee our forecast will pan out. However, it’s useful to put things into perspective and focus on the upcoming calendar events that could reignite market whipsaws. Needless to say, next Wednesday’s first FOMC meeting of the year stands out as a key potential catalyst. We anticipate Powell being pressed to clarify some of the statements he made in December or to comment on how the Fed plans to navigate the incoming wave of Trump’s executive orders.

If that’s not enough, there’s also an inflation report just a couple of days later, not to mention a packed earnings calendar. META, MSFT, and TESLA all report on FOMC day, while AAPL follows the next day.

With all these potential catalysts in mind, let’s take a closer look at the options prices and how we could structure a trade.