How to use the volatility term structure to improve your Sharpe Ratio

Not too steep, not too flat; just right there.

As the ski season hits its stride in the northern hemisphere, Sharpe Two finds itself stationed in Mexico City, perched at an altitude of 2250 meters. Yet, despite the elevation, racing down snowy slopes at breakneck speeds won't be part of our agenda this year.

No problemo; we’ve never been massive fans of winter sports anyway. Besides, the insurance premiums against potential injuries are as steep as the slopes themselves. Enough reason for us to take a pass.

Yet, there is one domain where our interest in slopes and steepness remains as fresh as morning snow: the volatility term structure.

For volatility traders, the term structure serves as a beacon, much like the North Star. If you’ve found yourself lost while venturing off-trail, just look at the term structure, and you’ll be back on the right track. Mastering this tool offers not just an edge but also robust guidelines for capital protection.

With the markets currently as flat and sleepy as North Dakota in winter, there is no better time to brush up on these essential principles. This way, when turmoil returns, we’ll have our bearings, ready to navigate the challenges and seize opportunities with precision and calm.

Let’s dive in.

What can we learn from the volatility term structure?

The volatility term structure is a fancy term that can be intimidating, but once demystified, it becomes a powerful tool in your trading arsenal.

It is essentially a snapshot of how the market values future uncertainty over different time frames. The most famous example is the VIX term structure, which can be seen through VIX futures or various VIX indices calculated by the CBOE.

This structure, combined with other factors, forms the foundation of our five volatility regimes, frequently discussed in our Forward Notes.

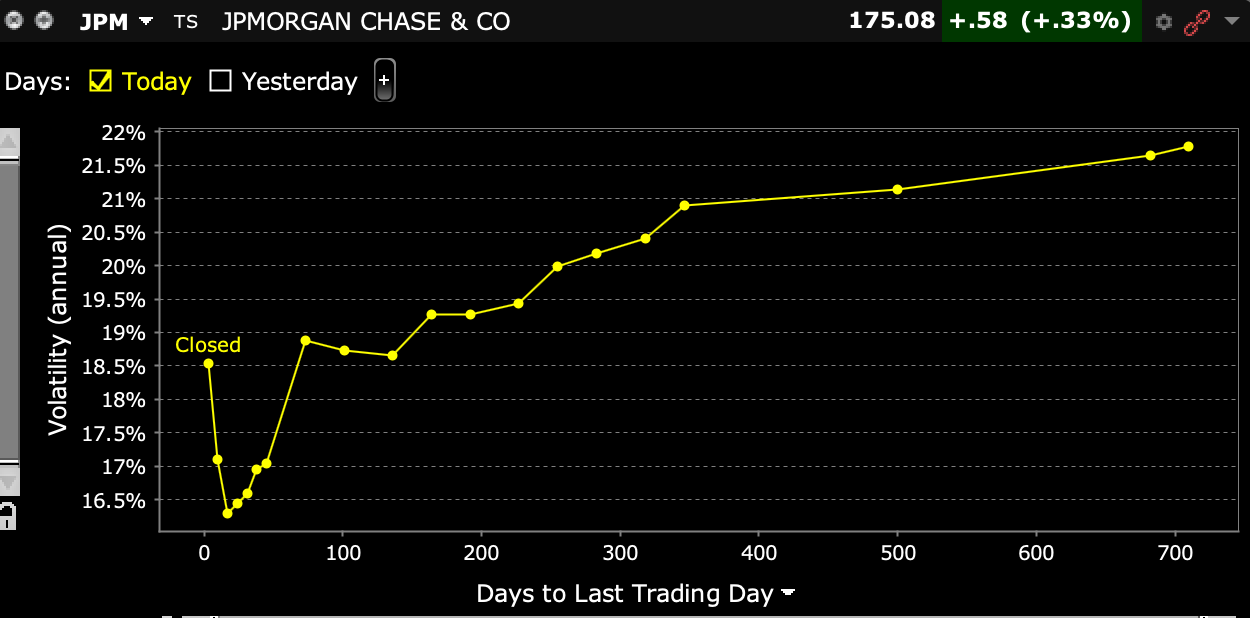

When you trade options on an underlying, the term structure is often a chart showing the different levels of implied volatility for different expirations. In IBKR, it looks like this:

Options prices, often seen as future expectations of market risks, give the term structure its unique shapes:

Contango: Future prices increase with time, indicating higher expected volatility or risk in the distant future compared to the near term.

Flat: Prices across different time frames are similar, suggesting uniform risk expectations.

Backwardation: Short-term options are priced higher than long-term ones, reflecting immediate concerns over market risk that outweigh long-term uncertainties.

A side note - volatility in short-dated options (0-15dte) tends to be higher than 25d to 60d): that is because the short term is often much harder to apprehend than the longer term. Unless very specific situation, do not read that as an imminent crash.

While these configurations can change rapidly, they generally remain consistent over periods, providing crucial insights into market sentiment and risk expectations.

Now, what does each of these distinctive regimes tell us?

In a contango situation, the market typically displays a normal risk appreciation. This means traders are willing to pay more for future risk due to the simple fact that, with more time, more variables can come into play. This increase in cost isn't linear; it tends to follow a ‘logarithmic’ curve, where the price difference between six months and a year (or more) becomes increasingly marginal. This pattern usually signals a healthy market.

However, when the curve flattens, it's often a sign of rising tension. This flattening usually comes with an overall rise in implied volatility, indicating growing market apprehensions. Short-term options become particularly expensive as traders brace for potential immediate risks.

But a flattening curve needs context to be fully understood. If a previously contango curve is flattening, it indicates growing short-term concerns. Conversely, if a backwardated curve flattens, it may suggest a shift toward normalization.

Indeed, a backwardated curve is a red flag, signaling acute short-term concerns. In this scenario, investors are willing to pay a premium for immediate protection, anticipating a stabilization in the future. This highlights the market's inherent cautious or even pessimistic outlook.

These regimes usually hold true across geography and asset classes. With that in mind, we can glean valuable insights into market sentiment.

Now, let's proceed to examine the data and see how these theoretical concepts play out in practice.

Going down the steepness curve

If you are a regular reader of Sharpe Two, you must now be familiar with our concept of a ‘naive’ short volatility strategy. This involves shorting a basket of at-the-money (ATM) straddles across a diverse range of ETFs every Friday, with each straddle having 28 days until expiration. Positions are held for two weeks before being closed out.

Let’s have a look at the results.

This 'naive' approach serves as a stark reminder that shorting options isn't a surefire path to profit—except, perhaps, for your broker. Markets are remarkably efficient, and a well-thought-out strategy is crucial to be profitable over time. We've previously explored how leveraging the variance risk premium significantly outperforms this basic approach. Today, we shift our focus to the volatility term structure's slope as our strategic linchpin.

To do this, we examine the average returns in relation to the slope between 1-month implied volatility (IV) and 3-month IV. For both time frames, we use options prices to calculate a VIX-like index following the CBOE's methodology.

One standout observation is the strategy's underperformance when the ratio exceeds 1.40. But what does a 1.4 ratio signify? It indicates a backwardated state, where the 1-month IV is priced at least 40% higher than its 3-month counterpart. This reinforces the lesson that indiscriminately selling IV, simply because it's 'expensive'’ lacks wisdom. The market's pricing of insurance premiums is not arbitrary—if they're high, there's usually a justified reason behind it.

It doesn’t mean there is no edge in selling volatility — in fact, this chart reveals a significant edge when the slope between 1-month and 3-month implied volatility lies between 0.7 and 1.1. This range typically signifies a contango or flat term structure, which traditionally indicates a healthier market sentiment.

However, the chart doesn't tell the whole story, particularly regarding the curve's direction towards backwardation or a return to contango. Engaging in straddle sales as we edge towards backwardation could be precarious. It’s more prudent to wait for the curve to normalize, leveraging this return to stability as a conducive backdrop for our trades. This highlights why understanding the broader context is crucial, especially when navigating the subtle shift from a flat to a slightly backward regime or vice versa (1 to 1.2).

The challenge with an overly steep curve is not to be underestimated either. Experienced traders are well aware that implied volatility is prone to mean reversion and a notably steep curve often signals that a reversal might be on the horizon. While it might be tempting to sell straddles in these conditions, context is king. If the curve is showing signs of flattening, it’s a signal to exercise caution. A volatility spike can dramatically affect your short positions, turning them from manageable to an active nightmare in no time.

A side note — some pronounced steepness isn't an outright call to go long on volatility. A steep curve can persist longer than anticipated. Timing is hard and resource-intensive, and the execution is often expensive. But it can get you followers on Twitter.

Given these considerations, we're fine-tuning our approach. We’ll focus on executing trades only when the curve’s steepness is comfortably within the 0.7 to 1.1 sweet spot, optimizing our strategy for conditions that historically indicate more favorable outcomes.

Adjusting our strategy to focus only on trades within the 0.7 to 1.1 steepness range significantly improves our metrics, yielding an attractive Sharpe ratio of 1.25.

Concluding remarks

However, there are a couple of nuances worth discussing.

Firstly, this strategy hinges on the assumption of executing trades across a diversified set of ETFs, which can pose execution challenges. While cost is often cited as a primary concern, we believe the real risk lies in execution pitfalls — the missed opportunities and the implications of not securing a position at the desired price.

Secondly, the strategy's reliance on specific parameters introduces a degree of uncertainty. Why settle on 0.7 instead of 0.6 or 1.1 instead of 1.2? These decisions, easily made in hindsight, lack forward-looking reliability. What's more, a parameter that works for SPY might not apply to CORN, highlighting the variability across different instruments. This underscores the limitations of a one-size-fits-all approach in volatility trading.

What our analysis really suggests is that there's a significant edge to be had in selling 28-day ATM straddles within a carefully chosen regime — neither too steep nor in the middle of a storm.

We urge traders to take this insight further, tailoring the approach to suit each specific ETF in their portfolio.

Be sure to follow us on Twitter @Sharpe__Two for more of our insights. If our work resonates with you, don't hesitate to share it with others who might find it helpful.