Let’s start there—we are not long volatility experts. The number of times we've gone short vol far outweighs the long volatility signals we take in any given year.

By early December 2024, as accounting season kicked in, we realized our hit rate on long vol signals was abysmal—bad enough to make us question whether it was even worth trying again in 2025. A few days later, the market delivered a harsh warning: in 2025, you’ll need to approach things differently and pay closer attention to volatility spikes. Then, in January, we got lucky. External events handed us exactly what we needed to justify the long drought of failed signals in prior years.

We don’t have a crystal ball—what we do have though is a sizeable options dataset. And while the market just experienced a collective cold sweat, the eerie quiet that followed isn’t a sign that we’re out of the woods. If anything, we might be deeper in.

Ouhou, spooky spooky! Let’s check a few data points.

The last two weeks have offered a breather to market participants. Is it going to last?

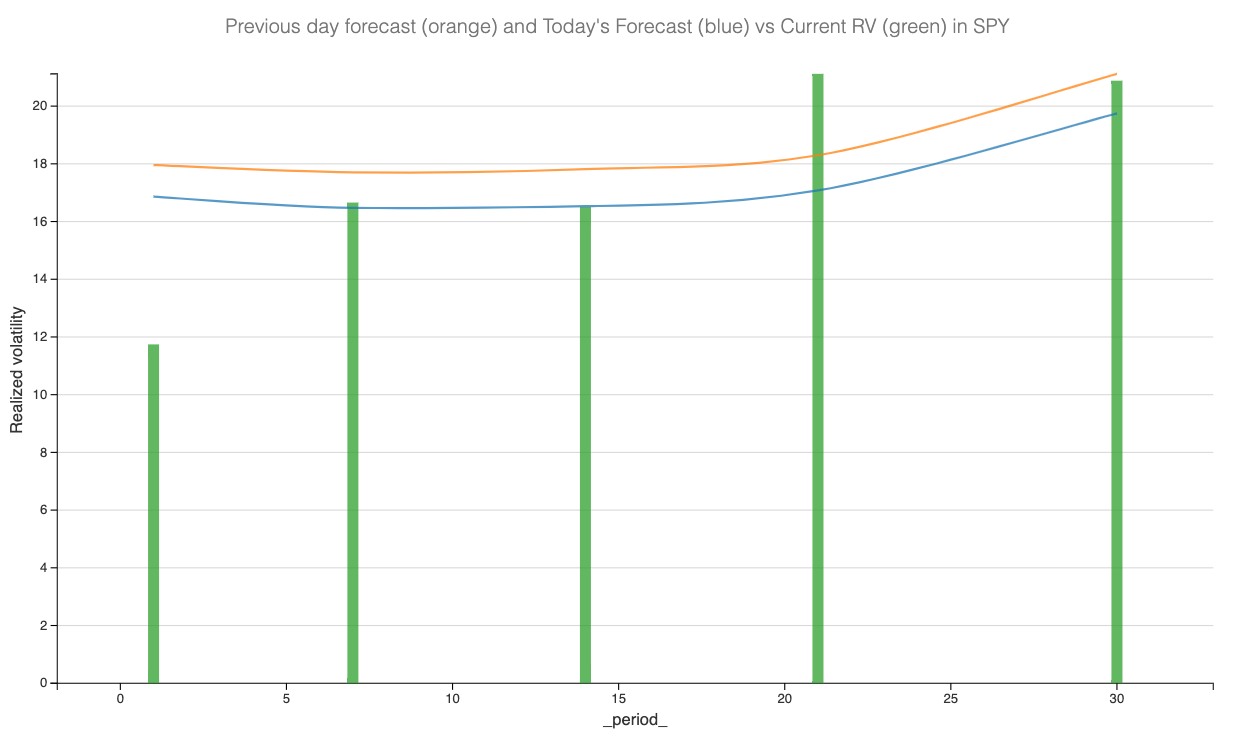

That said, it’s probably too early to call the end of volatility. As we know all too well, volatility tends to cluster—and with 30-day vol sitting in the low 20s, it's far more likely to hang around there for a while rather than dropping straight back to 14 or 15.

But before blindly following a model, we like to think through potential catalysts—and needless to say, there are plenty. In the next few minutes, we’ll get the latest GDP figure. In exactly a week, the next unemployment report drops. And with earnings season kicking off, there will be no shortage of fresh data for the market to digest—especially as it reassesses the impact of Trump’s policies on businesses and weighs growth expectations against the Fed’s stance.

And that’s just the obvious stuff. If the past three months have taught us anything, it’s that the real market movers might be the ones no one sees coming—especially with this administration in play.

Yet, the options market seems pretty casual about risk—not just to the downside, which everyone’s fixated on, but also… to the upside.

Let’s take a look.