Another week is on the horizon, and all eyes are on the SP500's next symbolic milestone - will we breach Mach 5 this week?

Even though Sharpe Two steers clear of making grandiose directional bets, it’s hard to see how we wouldn’t.

As usual, we’d rather focus on more predictable market patterns. With the earnings season winding down and the major macroeconomic announcements out of the way, the market is likely to remain tranquil - VIX 14, remember?

What does this mean for options traders? Avoid the long side and look for good overpriced opportunities on the sell side; it's more likely to be profitable.

With this in mind, today's focus is on XRT, an ETF that nearly made our list of favorite ETFs for premium collection last year if it wasn’t for a very average end-of-year - more on that in the performance section.

Let's dive in.

XRT keeps a large sampling strategy, with the top 10 holdings representing 16% of the total assets.

This approach positions XRT predominantly within consumer cyclical and consumer defensive stocks. These sectors attract value investors seeking stable cash flows, especially in challenging macroeconomic conditions. After all, consumers will always need to shop at places like Macy's or purchase items for their pets from Chewy.

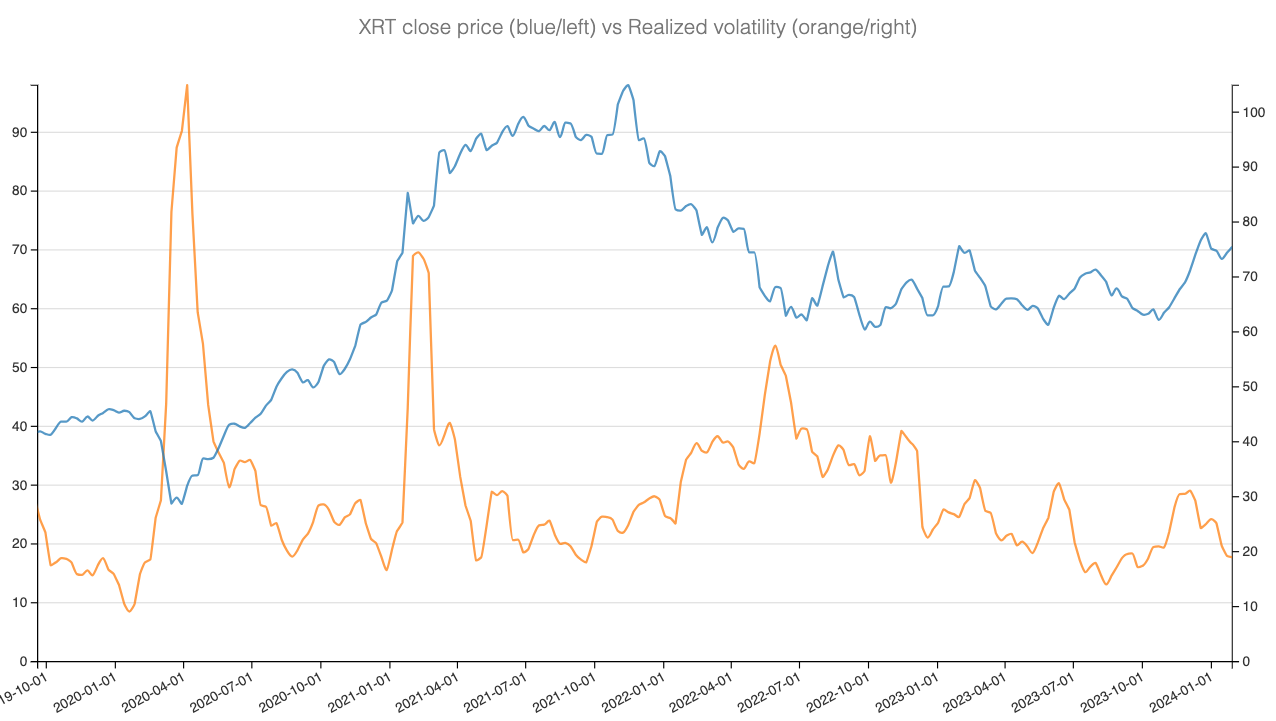

XRT saw significant growth during the COVID-19 pandemic, as consumer spending on essentials was amplified by substantial stimulus checks. However, as the economy reopened, the ETF's momentum waned, leading to a period of stagnation.

This transition is reflected in its realized volatility, which has mostly stayed under 20 since July 2023. A notable exception was in Q4 when volatility spiked to nearly 30. This spike might explain the subpar performance of selling straddles in XRT towards the year's end

Given that realized volatility has now dropped to some of the lowest levels in three years, the variance risk premium—an essential metric for options traders—might have shifted in favor of selling volatility.

Let’s now dive into the options data.

The signal and the trade methodology

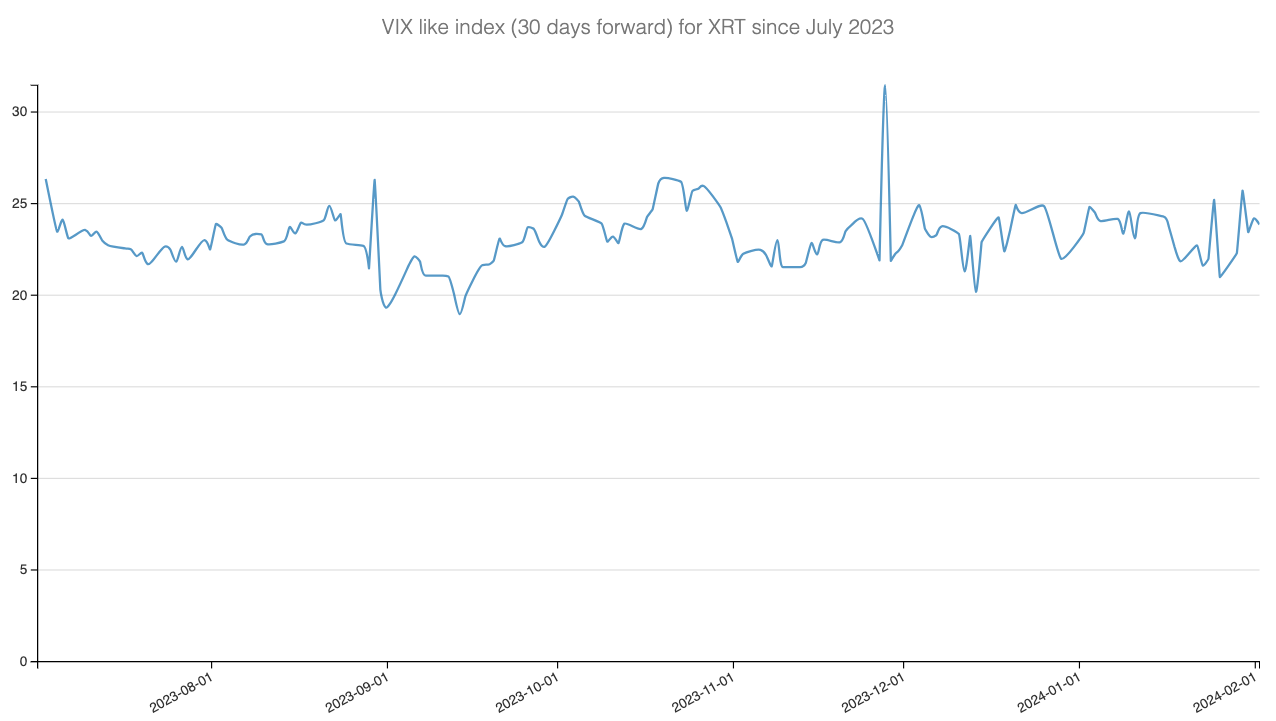

We began our analysis by constructing a VIX-like index for XRT, applying the CBOE methodology to calculate the index using 30-day-to-expiration XRT option prices.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.