Mastering Low Volatility: Strategies for Consistent Options Trading

Boost your performance by leveraging market filters, expiration buckets, and the VRP

Yesterday's CPI report didn't break the market, and the VIX closed well below 14. Our regimes indicate that we are in a low-volatility environment more than ever, and contrarians are still desperately searching for a catalyst. Remember last week's article: Trade the regime you are in—not the one you may be in.

Going long on volatility here may not be the best strategy.

Paradoxically, we concluded last week's article by demonstrating how combining moderately high implied volatility with expanding realized volatility created an excellent setup for volatility sellers.

Today, we'll explore a completely different segment of our matrix—the low implied /neutral historical volatility segment, which aligns more closely with current market conditions. If you haven't read our previous article yet, you may want to start there before diving into this second section.

Let's get started.

First, a little bit of (business) intuition.

Let's face it: things are far more exciting when markets are agitated, but this isn't good for business. Fund managers hate it because they must buy insurance at a steep premium and explain why they failed to beat the benchmark.

Despite popular belief, this isn't the favorite moment for option sellers either—risks are more difficult to assess, and the likelihood of booking a significant loss is much higher than in calmer situations.

You need to be an experienced trader to make money in chaos. This is another lesson I learned as a young trader. When MF Global went bankrupt, there was a stark difference in PnL at the end, which could be explained by a simple feature—seniority.

As we've mentioned many times before, when you're a volatility trader, you're first and foremost in the business of selling short-term insurance contracts to fund managers anxious about their long-term performance. Boring and predictable is the bread and butter of any insurance business, and the options market is no different.

Let's be specific: who would be the better customer? Nicola, a mid-thirties yoga expert and recently promoted mid-level manager in the tech industry, with 347 Facebook friends, no children yet, and about to be married in three months? Or Steve, also in his mid-thirties, an adept of any substance to sustain his long weekends of partying, out of shape since he left Columbia 15 years ago, in and out of jobs, and recently appointed CTO of a reasonably successful crypto company?

Sure, insurance providers will ask for a higher premium in Steve's case, but unfortunately, they may very well have to pay out this premium later when Steve faces health complications. In Nicola's case, though, her lifestyle is so predictable that even with a discount to convince her to sign a contract, the insurance company will still make a hefty profit. One is expensive but volatile, while the other looks cheap on paper but is still very lucrative.

Last week, we concluded that you needed to avoid Steve. Today, we'll try to identify our Nicola—not very volatile, predictable, apparently cheap, but super profitable.

Let's look at the data.

Some (more) intuition around Vega and Beta

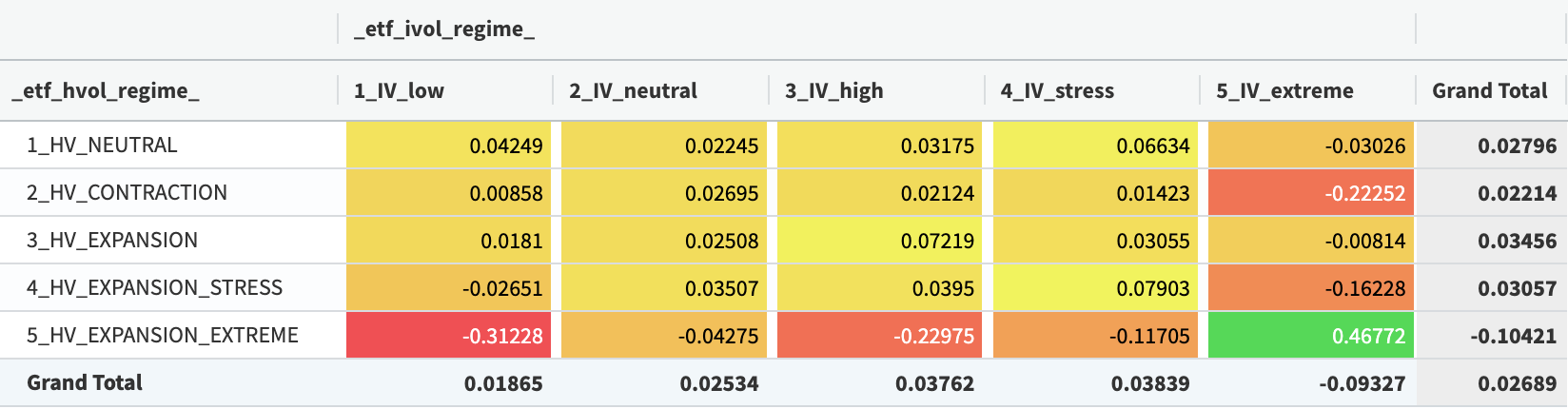

As a reminder, we've segmented implied volatility and realized volatility into five segments. We created a matrix showing the performance of selling every straddle across a universe of 60+ ETFs and holding them for two weeks for each of the 25 segments of the matrix. We standardized our position to $1 of credit collected per trade. Here's what the results look like:

The conclusion was that a Sharpe ratio of 2 could be achieved by targeting a moderately high level of implied volatility while historical volatility was expanding.

This strategy cannot entirely avoid the ebbs and flows of early 2022, but it didn't destroy capital, which is a great start.

Now, let's focus on the first segment of the matrix—low implied volatility and neutral historical volatility. The average return is around 4% per trade, well below the 7% observed in the IV_High/HV_Expansion segment, but still significantly higher than most other segments.

The results are far less impressive, as predicted by the average return in the matrix. In particular, this strategy suffered a severe drawdown in the first part of 2022, when things were up in the air.

This may seem counterintuitive to the attentive reader—weren't we targeting ETFs in a low IV state where historical volatility was neutral? Why does it seem that the segment is still affected by the "bigger picture" in the market, such as the Ukraine War and the Fed's fight against inflation?

This is an excellent opportunity to build more intuition about the marketplace. Even if you only target ETFs that may be uncorrelated with what is driving the market, and even if they seem to be in a low volatility regime, the overall market sentiment still impacts how things will develop for a particular product.

If you're familiar with the concept of beta, which measures the relationship between an asset's returns and the overall market (often using the S&P 500 as a benchmark), you can draw a parallel and see this as the expression of volatility beta.

Of course, the best scenario would be to identify completely independent products; however, finding an asset class that won't be affected is rare when things are up in the air. Remember, the market is a place to allocate and redistribute capital based on macro and microanalysis. Fund managers will take money out of one place and bring it elsewhere. This simple risk-on/risk-off mechanism is exacerbated during periods of high uncertainty and is likely to touch every asset class and geography.

The question then becomes: how do you counteract that effect?

VVIX to the rescue

You could, for instance, focus on a product with a low volatility beta compared to your index (often the S&P 500), which will be the subject of another article.

Alternatively, you can do something much more straightforward. The advantage of options is that you can choose how close you want to be to expiration. It is well known that the closer you are to expiration, the higher the reward (as volatility is often grossly mispriced) and the higher the risk (as gamma tends to be at its maximum).

Let's see how this strategy performs when we segment our straddles according to three buckets: the front month (less than 30 DTE), the back month (30 to 60 DTE), and the far month (60 to 120 DTE).

Staying in the far month often guarantees less volatility for your returns, especially when the marketplace is agitated overall. One could argue that getting closer to expiration when things have calmed down is a sensible strategy to maximize performance.

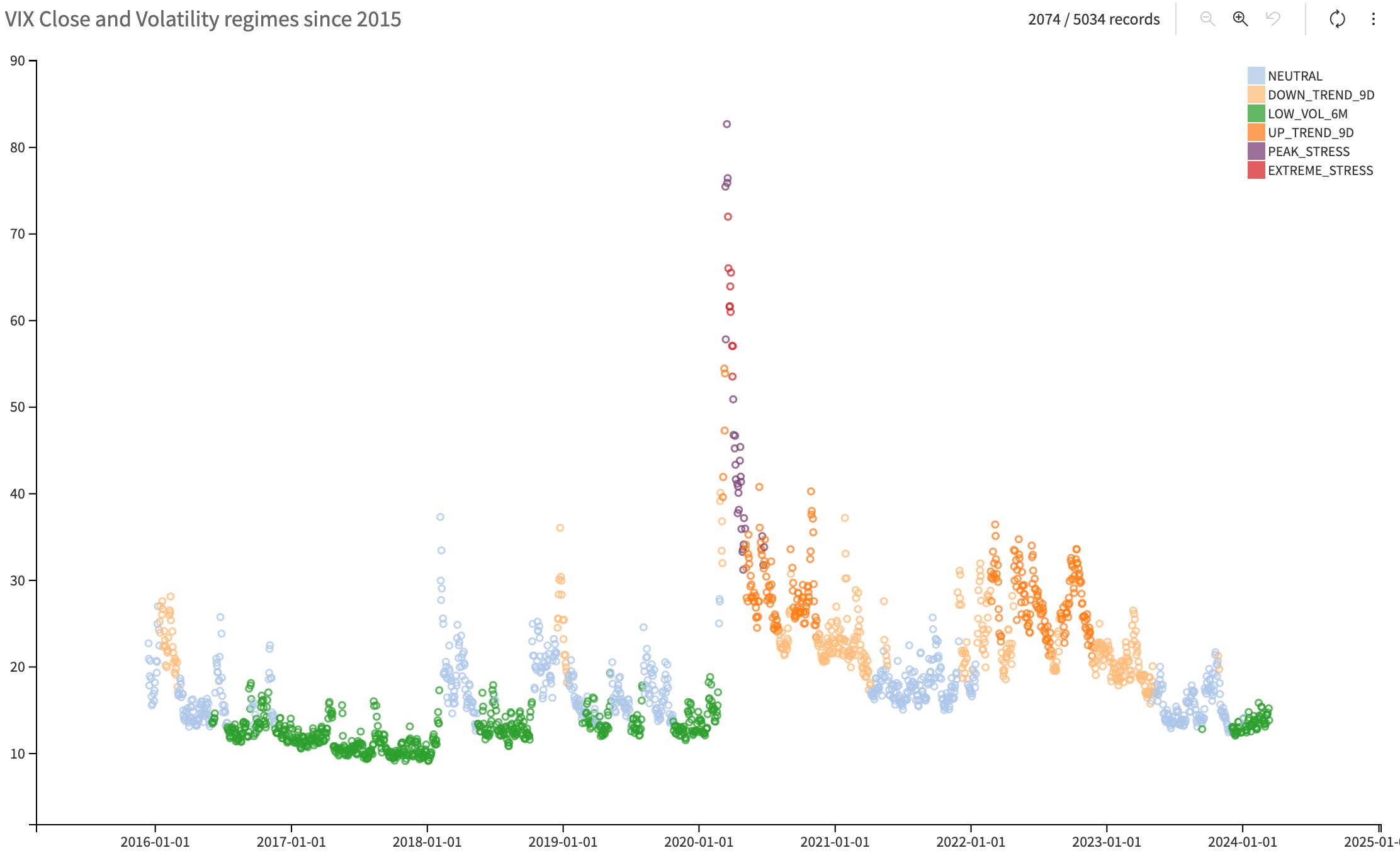

The question becomes: is there a simple and objective way to measure whether things are up in the air? Taking the VIX or, even better, the VVIX is usually a great place to start. These products provide an immediate indication of the current risk perception in the US market and, by extension, the different markets overall. Their mean-reverting nature also makes them super easy to interpret. They play a significant role in our calculation of the volatility regimes in the US market and help us build this chart that we publish occasionally in our Forward notes..

Let's take another look at this performance graph, this time when VVIX is only below 100 (which is above the long-term mean of 90 but often a critical "threshold" in the index to define if things are "scary" or not).

A side note: VVIX is an excellent filter, but remember that when things are "scary," they are usually all over the financial press, and your gut feeling will tell you something is off. So, if your social media timelines don't look depressed and the Financial Times or Bloomberg aren't fueling the fire, you can safely conclude that VVIX is below 100 and that things are okay.

This looks much better, particularly in the far month, but there is still a long way to go before reaching Sharpe Two in the front month.

Enters the VRP for the win.

Now that we have examined the general state of the market to filter our signals within the low IV/neutral HV regime, we can improve our performance using traditional techniques employed by volatility traders.

The most famous technique is to consider how stretched the VRP is. Selling straddles regardless of the VRP in the high IV/HV expanding regime was relatively okay because when the IV is high, you can infer that the VRP is stretched. However, this is still a "dangerous" assumption, and you should always check before putting on a trade.

This assumption certainly doesn't hold when the implied volatility is low and will conflate with historical volatility for certain asset classes.

Let's see what the performance looks like when we only focus on times when the z-score for the VRP (computed as the ratio between the straddle prices and the recent movement in the underlying) is above 1.

This now looks like a sensible strategy we would want to trade, particularly in the far month if we wanted to decrease the volatility of our returns, but even in the front month if we were focused on maximizing profit.

Next week, we will focus on the names that performed well in these specific regimes. Of course, past performance is never a guarantee of future success, but we may gain some interesting insights about asset classes overall. So, make sure to subscribe to stay updated!

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.