Forward Note - 2024/12/22

"This Christmas, I gave you my PnL. And on the very last day, you gave it away."

We will take a break and come back in early January. Happy holidays to everyone. If you are not subscribed yet, here is a 46% discount until the end of the year and the story behind it.

There’s one thing the markets hate more than bad news: uncertainty.

This week served as a perfect reminder. When Chair Powell took the stand to outline the rate trajectory for 2025, the markets responded with a violent nosedive—one of those moments where you’d think a crisis had erupted.

But the message itself? It wasn’t disastrous. The economy remains strong, Powell said. Yet inflation remains stubborn, and the Fed’s outlook has shifted: next year won't bring the four rate cuts the market eagerly anticipated. There might be two cuts, eventually—but even their timing is uncertain.

To anyone outside the financial world, this seems like a reasonable stance. A leader openly admits that he can’t predict everything, especially how the economy will react to policies beyond his control (yes, Mr Trump, he is looking at you.)

However, markets rarely behave rationally, despite what modern finance theory assumes about its participants. What started as a bad day before Powell's press conference quickly devolved into a bloodbath. The SP500 plummeted nearly 3% in the final minutes before the close, while the VIX surged an eye-popping 12 points.

A 12-point jump is no small feat—especially in a market primed for a Santa Rally, with champagne bottles ready to toast what was shaping up to be the best year for the SP500 since COVID-19.

The tension didn’t ease as the week progressed. The VIX hovered comfortably above 25, building suspense ahead of Friday morning’s core PCE number. At that point, after erasing five weeks of profit in just 48 hours to hedge our book, a new concern emerged: our Christmas holidays. After all, who wants to be glued to their laptop during Christmas week, just in case the market decides to implode? Certainly not us.

It turned out we weren’t alone in our concerns. Once the inflation numbers came in lower than expected, the market collectively exhaled. The VIX swiftly dropped below 20, and, as if by magic, the chaos evaporated overnight.

This begs the question: what on earth just happened? And more importantly, is this really over?

First, let’s admit it: we were wrong, again. And unfortunately, it happened at the worst possible time of the year. There’s no ideal moment to misread the market, but expecting tranquility only to witness weekly realized volatility settling at 17%—and the last three trading days clocking in at 25%—is a stark reminder of how unpredictable and irrational the market can be.

Complacency often makes the consequences of an unexpected event far worse. It’s not that the improbable becomes more frequent; it’s that you’re ill-prepared to handle it when it does occur.

Being wrong in this business is part of the game. It happens more often than we’d like, but over time, reflecting on missteps and paying attention to subtle market signals can make you better.

A few weeks ago, right after Trump’s election, we noted how quickly the market had been moving. We hinted that the market had become acutely aware of the volatility trade—more so than ever before—and was ready to exploit it at the slightest opportunity.

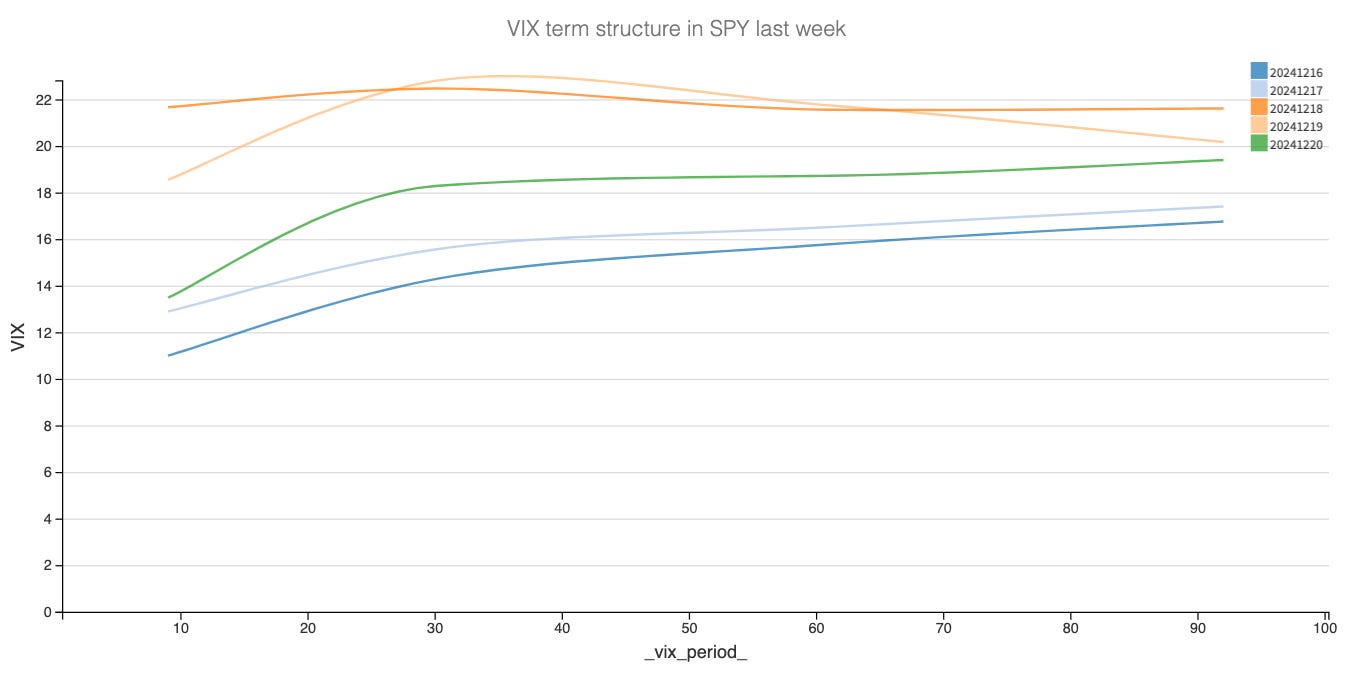

This week provided yet another textbook example: the VIX term structure was elevated, stretched to the limit, and then mercilessly crushed, all within just two and a half trading sessions. The speed and severity of these moves reflect how efficient the market has become at capitalizing on volatility, leaving little room for complacency.

We don’t claim to have seen everything the stock market has to offer, nor do we expect you to take our words at face value. However, these recent movements in the VIX term structure are anything but typical—or at least, they’re uncommon enough to raise an eyebrow.

For a data-driven publication like ours, “uncommon” is insufficient. We needed to quantify just how rare these movements are and, if possible, uncover any subtle signals or clues that might explain them.

Our first step? We computed a simple standard deviation of the various VIX indexes over a long enough time frame to capture both ordinary fluctuations and the outliers that occasionally shake the market.

You don’t need an MIT PhD to grasp that last week was exceptional. The agitation in implied volatility was far greater than the spike we saw in July. Back then, realized volatility in SPY hit an astounding 80 on August 5, compared to just 25 on Wednesday and Thursday this week.

Even more striking, this week’s activity dwarfed the tremors following the U.S. elections—the most recent peak on the volatility chart.

Taking a step further, if you adjust the scale, apply a log transformation to the VIX, and measure the daily standard deviation of log increments across the term structure, the only comparable event in recent memory was Volmageddon back in February 2018.

Another striking feature of this chart is the two-year period between early 2022 and mid-2024 when spikes above 0.03—corresponding to the 90th percentile in the distribution—were virtually nonexistent. In contrast, such spikes occurred much more regularly in the years preceding Covid.

There are plenty of hypotheses to explain this phenomenon: the rise of 0DTE options absorbing volatility, a more "efficient" market due to an increased presence of market makers (sic), a flawlessly executed battle against inflation (sic bis), or simply the normalization of markets after the Covid trade.

In the grand scheme of things, the specific cause doesn’t matter. What’s evident is that this period of calm marked the longest stretch since 2011, and, as the past six months have shown, it’s now over.

The temptation to claim that something catastrophic is brewing is hard to resist—markets don’t spike like this without consequences, right? We’ve read some rather dramatic comparisons to tectonic plates shifting, hinting at the "big one" looming on the horizon. Only time will tell if these predictions hold any weight.

We’ll take a more measured approach. The era of two years of calm is behind us, and 2025 demands a mindset reset. Markets move, and sometimes they move erratically. It appears we’re entering a phase where those who are careless in their positioning or who underestimate the unpredictable nature of implied volatility will face swift and unforgiving consequences.

In other news

Bitcoin took a hit last week, and so did MicroStrategy (MSTR). Yet, despite the tumble, the company—now boasting a market cap of $90 billion—remains on track to join the Nasdaq 100 next year. Quite the remarkable turn of events for what started as a software seller. Yes, because MSTR still sells software: around $116 million in annual revenue, albeit with an operational loss of $18 million. But who cares, right? The playbook is simple—issue debt to buy Bitcoin, and watch the company’s value soar in tandem with crypto prices.

The Financial Times called it a feat of “financial engineering,” and we couldn’t help but raise an eyebrow at the term. Isn’t this just a masterclass in white-collar opportunism for all the crypto bros out there? A sleeker, boardroom-approved version of the classic pump-and-dump?

In a traditional pump-and-dump scheme, you’d face hard questions—why sell all your coins if you’re such a believer? That’s the kind of thing that lands people in trouble. But with some well-crafted financial engineering, you don’t need to sell the coin. You sell the shares of the company holding the coin instead. After all, isn’t that just “maximizing shareholder value”?

As we close out this year, we wish you only the best for 2025—for yourself, your family, and your portfolio. We also want to thank all our readers. Thank you immensely for your kind words, support, and encouragement.

Please share this newsletter with your friends and whoever you think can benefit from it.

We will see you in the new year.

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.