In a recent discussion with one of our readers, the old saying about "picking up pennies in front of a steamroller" came up. It has been a while since we heard that one, and we decided to make it the focus of this article.

This phrase is typically thrown around to criticize volatility traders, but it actually highlights a widespread misunderstanding between two closely related yet fundamentally different trading strategies: trading volatility and trading the tail.

For seasoned traders, the distinction might seem clear-cut, but a brief scroll through social media reveals that many retail traders blur these lines. So here is our attempt at demystifying these concepts.

In true Sharpe Two’s spirit, we won’t use any advanced mathematical explanation: as my prep school math teacher often said, 'Intuition before equation.'

If you had to take just one thing from this piece, it’s this: despite the allure of passive income and having your money work when you sleep, promoted all over the internet, retail traders should avoid trading the tails.

At all costs.

Sometimes, the VRP is here (above 1), and you should sell big delta options.

However, most retail traders don’t trade volatility that way. They look for far out-of-the-money options with a “high probability of success” and sell them with no hedging more than “Well, my strike is 10% below, it is unlikely that I will be challenged, and if something wrong happens, I’m happy, to wait until expiration and see where we are.”

There is nothing wrong with that.

Until there is.

The only little problem is that the market doesn’t have time to wait. Time is money, your loss is someone else profit, and the margin call mechanism makes sure that all counts are squared at the end of the day.

A tale of two different regimes.

To really understand the difference between volatility and tail trading, one has to understand the two very distinct regimes in which the market tends to operate: normal days and very abnormal days.

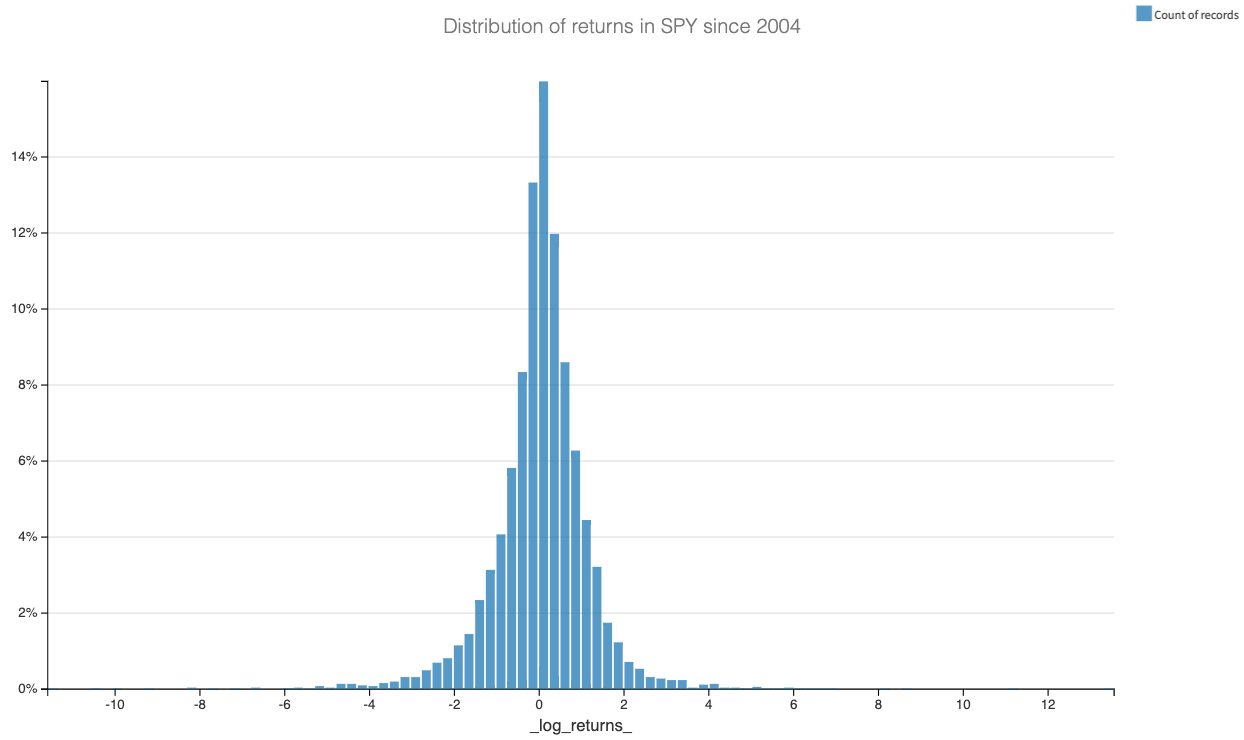

Under normal circumstances, asset returns follow a somewhat of a normal distribution akin to the classical bell curve. Essentially, this assumption implies that movements magnitude (not direction) in asset prices are somewhat predictable, with significant swings being the exception rather than the norm.

Roughly 60% of the trading days fall in the category +/- 1 standard deviation of returns (what we call realized volatility) and is well captured by the price of an at-the-money straddle: a straddle priced at $100 suggests an expected 100-point fluctuation in the stock's price, over that period of time.

This is a good enough simplification; for those interested in a deep dive into this topic, comprehensive article offers valuable insights.

You can see that the belly of the curve is somewhat normal. But the assumption doesn’t hold true at all at the tail, though: see the abnormal cluster right below -4%, or how from 2 to 4% it is almost the exact same frequency of occurrence? This means that in abnormal circumstances, the market just does its own thing, and anything can happen.

This post is public, so feel free to share it: the more retail traders see it, the more you help us in our mission to narrow the gap with professionals.

A matter of errors

If asked about the market's return for tomorrow, assuming normal circumstances, you may guess a range within -/+1% or perhaps 2%, and even if the market were up 3%, your error would be marginal.

The challenge arises when unexpected events occur. If a major earthquake hits California, the market will plummet. But by how much? -10%, -20%, or even -30%? It becomes difficult to predict, and the margin of error in these extreme scenarios greatly exceeds that of more routine daily predictions.

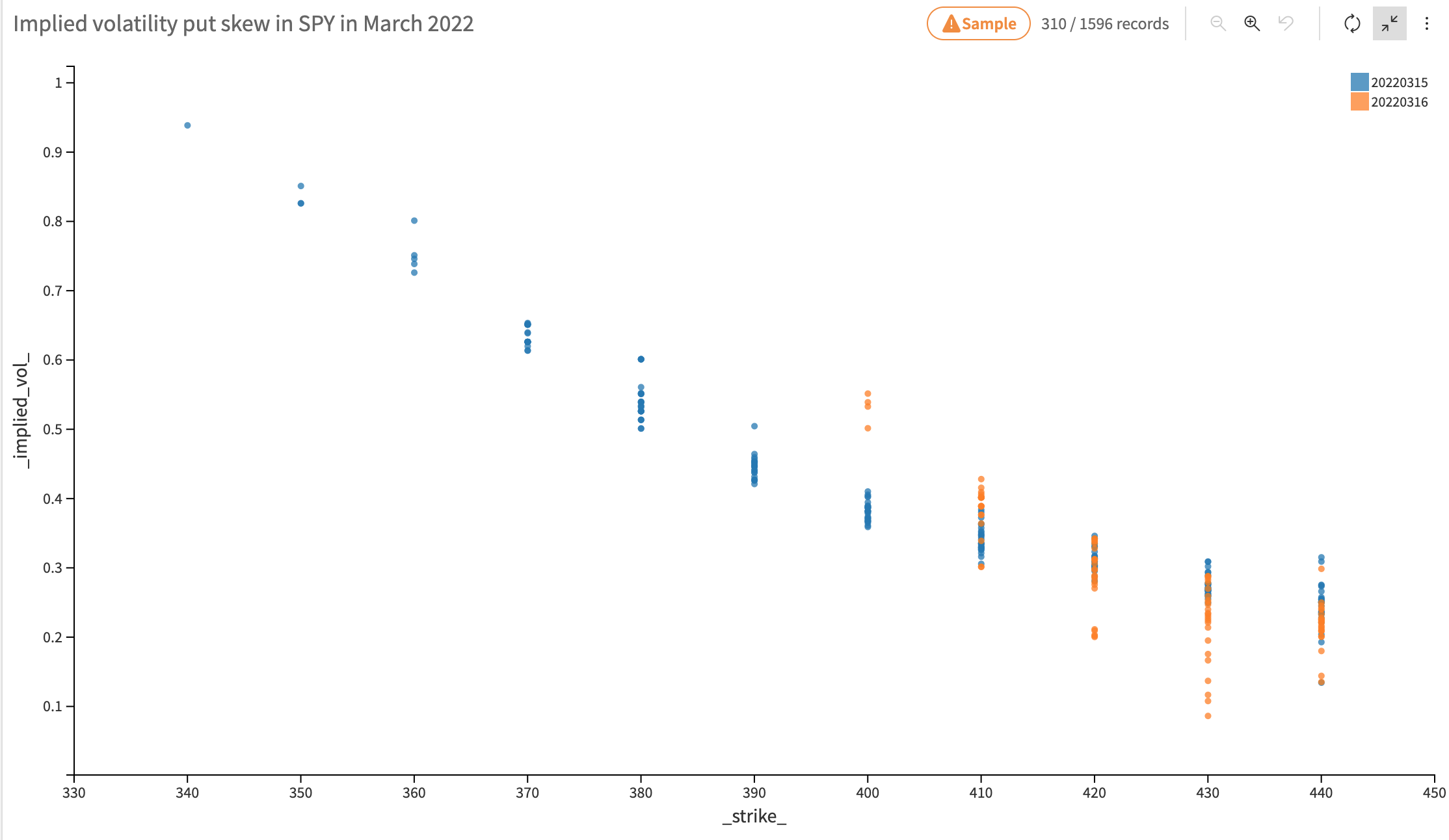

This is why we observed the skew in far out of the money puts: put sellers implicitly understand that under such circumstances, their model will break, necessitating a heftier premium to offset the risk. Conversely, buyers are willing to pay more for these options as insurance against catastrophic events, ensuring they're protected when "all hell breaks loose."

Who typically sells these "tail" options, and why might it not be wise for retail traders to follow suit? The sellers are usually market-makers, arguably the best risk managers in the marketplace. Their job is to provide constant liquidity, and they adhere to strict risk management protocols.

When they sell an option, such as a five-delta put, they immediately hedge the risk by engaging in another transaction: delta hedging, buying an option with a very similar risk profile in a correlated asset. Their arsenal is vast.

Retail traders, on the other hand, are not as disciplined: soon, they discover what a rise in implied volatility could do to their accounts while the market is not even challenging their strike.

“Hello? it’s me. Your margin.”

Let’s take a concrete example - it’s January 2021; Geoffrey has a 10k account and sold a $2 put on SPY expiring in 3 months (roughly delta 10), and he intends to repeat that all year to collect 8%. In his mind, it’s close enough to the average yearly performance of the SP500, and he doesn’t have to manage his account actively: his money works while he sleeps.

In December 2021, Geoffrey had a great year and started thinking, "Why not scale up? Selling five contracts instead of one could net me $1,000 every three months, equating to $4,000 annually on my $10,000 account." 40%? Now that’s appealing, and maybe that option game isn’t too difficult to master after all.

With an increased sense of confidence, he concludes: "What's the worst that could happen? My strike is so low that if disaster strikes, I'll have time to react."

However, the crux of trading implied volatility lies in its nature as a product of supply and demand. When panic sets in, everyone scrambles for protection.

In such circumstances, people say implied volatility goes up, but a more accurate description would be the demand for options skyrockets. Consequently, the price of Geoffrey’s put doubled overnight, despite his strike still far out of the money, leaving him exposed to significant losses.

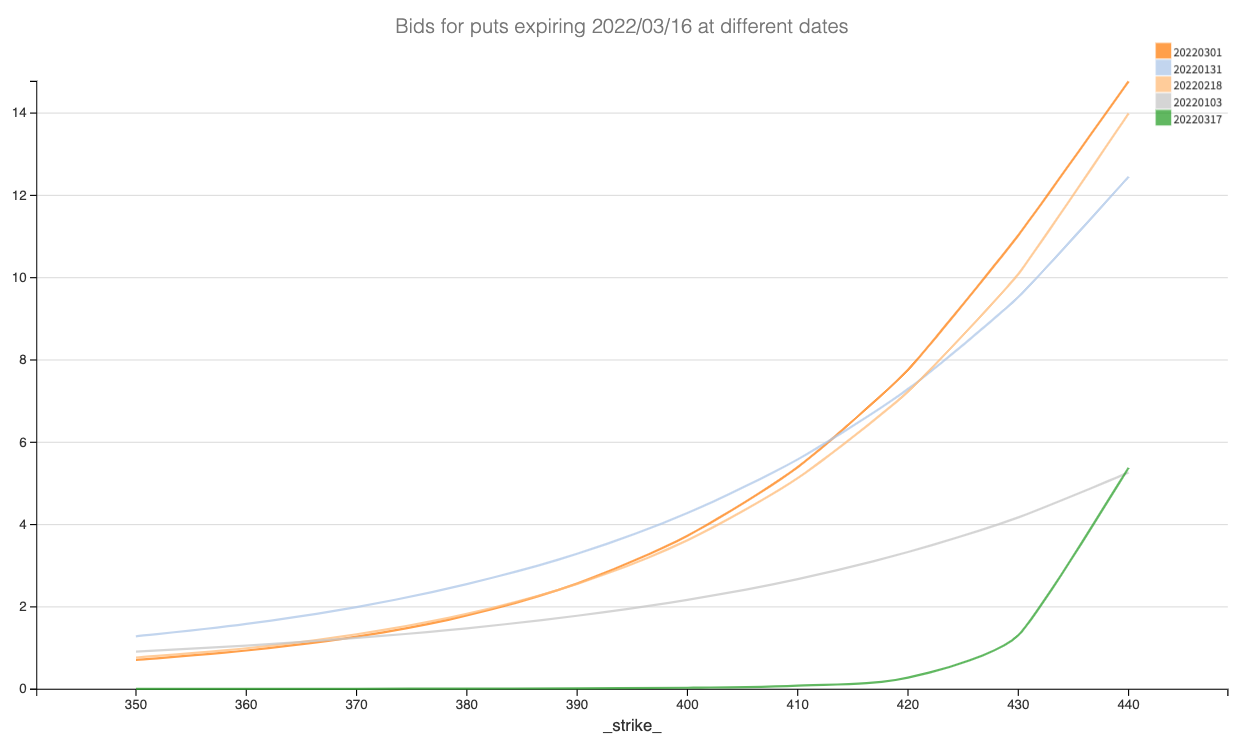

When you trade volatility, your margin requirements aren’t tied to the strikes you sold, and your pnl is a direct function of the current price of these contracts. Let’s focus on the put 420 expiring in March 2022 that Geoffrey sold in January for $3.3, not knowing that the war in Ukraine would explode.

His P&L now reflects a loss of (7.3 - 3.3 )* 100 * 5 = $2,000. That is 20% of his account, despite his strike still far from the money.

And as misfortune loves company, recall how he leveraged his account to the hilt, buoyed by overconfidence in an infallible strategy? Soon, he receives an unpleasant call from his broker, going along these lines (we tried to put some Adele’s lyrics to sweeten it a bit)

Ring tone

Hello, it’s me. Your margin.

I was wondering if after all those years you’d like to meet.

To go over, everything.

They say that time’s supposed to heal you

But your account will need more than healing.

It needs more money. Now.

Or else we liquidate everything.

Don’t be Taleb’s turkey.

Please don't misconstrue this discussion as a green light to sell the tail as long as you avoid leverage. This is a very poor usage of capital - 8% of the year vs. risk of ruin is a proposition you should not consider under any circumstances.

Instead, you should be focusing on the big options and trade volatility at the money when the implied volatility exceeds the realized movement in the underlying.

The only trading you should do in the tail? Buy them and leave the business of dealing with tail risk to professionals. They are like health insurance: you’ll be happy to have them when you need them.

Because you will: back in 2020, we would have never thought a single-day drop of 10 % was possible in modern markets. The situation is worse in stocks, where daily moves of 25% can occur more frequently than in indices. A quick tour of Wall Street Bet, and you will see stories of traders losing their accounts overnight.

We will conclude with a reference to Nassim Taleb. Regardless of your opinion about his character, his analogy of the turkey blissfully counting days until Thanksgiving provides a stark warning: everything may seem fine until, suddenly, it's not. And unfortunately, there is no in-between.

Don't let your account become someone else’s Turkey served up for Thanksgiving, and for which they will be very grateful.

Be sure to follow us on Twitter @Sharpe__Two for more of our insights. If our work resonates with you, don't hesitate to share it with others who might find it helpful.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.