Finally, volatility has spiked - the biggest intraday move since November 2021.

Long volatility traders are dusting off their "I told you so" mantles, while some who bet heavily on the short side might be licking their wounds.

In the realm of short volatility trading, days like yesterday are part of the game. Your goal is to manage risks as best as possible to avoid getting burnt: control your gamma exposure and try not to stay there too long, particularly ahead of potential market catalysts.

At the end of the day, it always comes down to a fundamental question: what is your role in the marketplace?

At its heart, short volatility trading is akin to the insurance business. You're essentially offering short-term protection to fund managers wary of their long-term performance. You are dealing with the risk they don’t want, and in exchange, they pay for the service.

Once in a while, there comes an incident, and you have to cover the bill.

It’s called business.

To be honest, we are quite excited about that spike; it means fund managers may wake up after four months of euphoria. Yes, the market can move 2% in a day, and when it does, you’d better be covered. Hopefully, this will serve as a reminder and prompt their swift return to the options pit. And if you know how to assess risks, you can take advantage of their price urgency and price insensitivity.

Ultimately, the essence lies in evaluating situations for what they truly represent.

For instance - why would you buy the volatility in us equities right now, right after the spike?

It may be tempting but not opportune. Volatility does mean revert. And we don’t know - nor is it that important - if it is on its way to 19.

Therefore, avoid buying puts with no other plan than “VIX was up 25% at some point yesterday and then closed under 16. Therefore, it’s a good point of entry, and it should go back to a reasonable level, real fast, real soon.”

What’s a reasonable level? Something you guessed through lines and resistance on a chart? Or a piece of insight you read about dealers’ gamma exposure? No one knows what a reasonable level is, and the most reasonable thing to do is to stay calm and patient.

Let the VIX rise, and when it is ripped for being short, you’ll get the memo soon enough. It is an easier trade than timing spikes like yesterday.

So, what's the move in the meantime?

We stick to our proven strategy: seek out areas where the market's compensation exceeds the risk. The financial world extends far beyond U.S. borders, and while global markets often move in tandem, each has its unique risk perceptions and motivations for purchasing insurance.

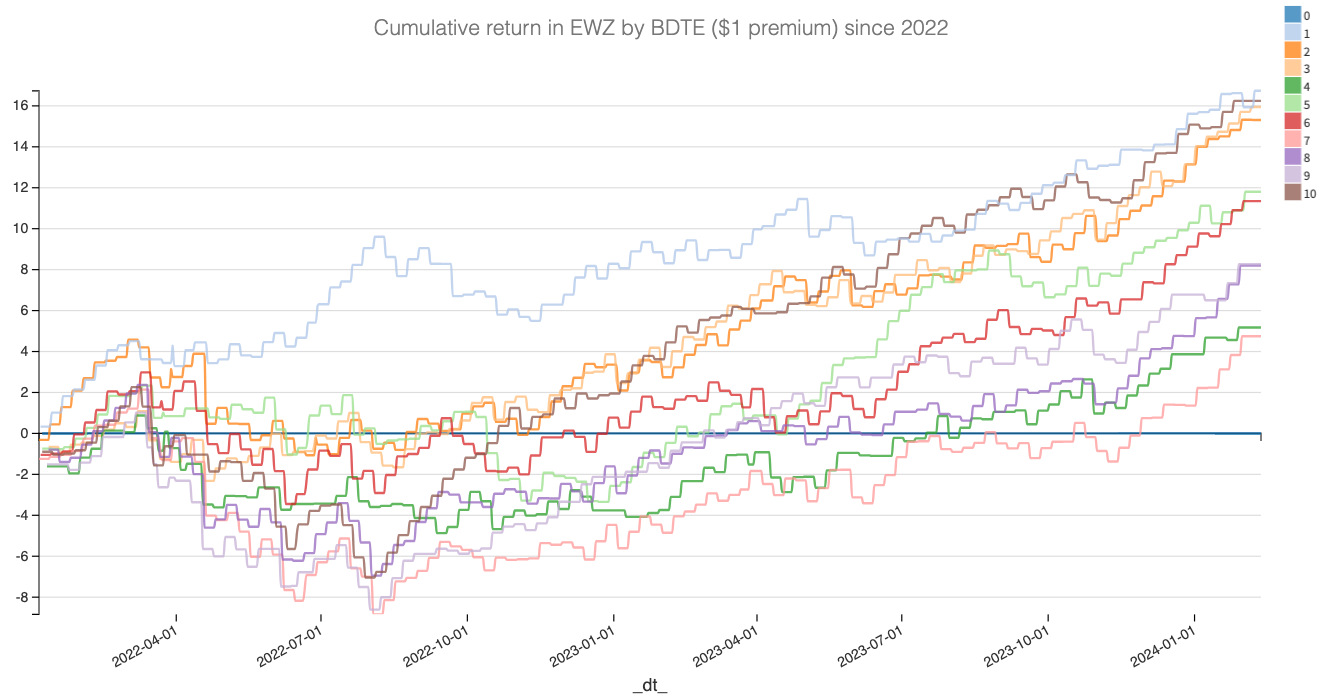

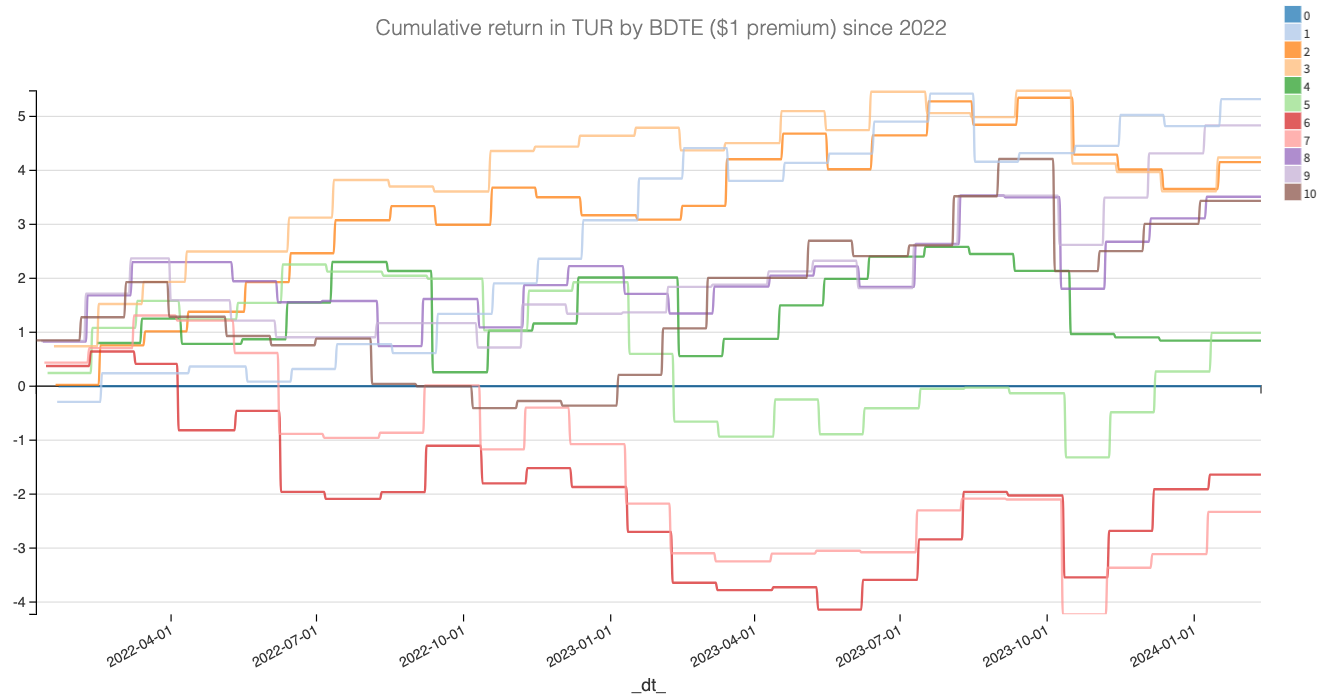

Given the positive feedback on our recent VXX trade, we're diving into 0/1DTE for two emerging market ETFs: EWZ is tracking the Brazilian equities, while TUR is doing the same for Turkey.

These ETFs represent vibrant yet fluctuating economies, each with its unique set of challenges and opportunities for short volatility traders.

The last three days until expiration allow you to capture most of the premium without hedging.

The findings for the Brazilian ETF (EWZ) are quite revealing. Interestingly, selling a straddle ten business days to expiration yields, on average, the same return as selling it just three days before expiration. This pattern underscores fund managers' habit of seeking last-minute hedges—opting for what they perceive as cost-effective protection against unforeseen market turmoils. The mantra "better safe than sorry" seems to prevail.

For TUR, the Turkish ETF, the impact is even more substantial. Yet, it's important to note that TUR's market is significantly less liquid than EWZ's, with only monthly contracts available, not weekly. This discrepancy in liquidity might explain some of the observed differences in trading behavior and outcomes.

Thank you for reading Sharpe Two. This post is public so feel free to share it.

Setting aside the liquidity differences, the pronounced outperformance on days 10, 9, and 8 compared to days 6 and 7 underscores the predictability of fund managers' behavior. Imagine you're a fund manager with compliance policies mandating hedging. This often translates into a pattern of securing protection right before the weekend (10 bdte translating to 14 dte) or early in the week preceding expiration (9 bdte or eight bdte). Otherwise, you will focus on the last few days before expiration, where the premium is the lowest … but not the cheapest.

While averages provide insights, the true story unfolds in the cumulative P&L returns.

It's noteworthy that positions opened 0 and 1 business day to expiration (bdte) yield comparable results to those initiated two weeks prior. This observation reaffirms the strategic timing of fund managers seeking to hedge.

The Brazilian ETF, EWZ, remains a favored asset for us, consistently offering clear advantages, especially in short tenures. TUR, the Turkish ETF, presents a different scenario. Although it offers potential in the very short term, concerns over liquidity and geopolitical proximity to conflict areas prompt us to exercise caution across other parts of the expiration cycle.

It's important to acknowledge the inherent risks in these markets. They often come with a set of challenges, including the potential for sudden political or economic shifts, which explains why the premium. It also means that once in a while, things can turn bitter.

The Brazilian ETF's performance dip from April to September 2022 wasn't just a reaction to the Fed's interest rate hikes; it also reflected investor nerves around the turbulent management of the COVID crisis and the buildup to the presidential election. In such times, the trading edge becomes murky, with one notable exception: trades placed one business day before expiration (1 bdte).

The trade methodology

So, what's the trading strategy?

Consider shorting the ATM straddle in EWZ and TUR one day before their expiration. For those feeling a bit more daring, you might start shorting EWZ two weeks in advance. However, we advise caution with TUR due to its unique set of risks.

The appeal of this strategy lies in its simplicity. For once, you can temporarily set aside the Variance Risk Premium (VRP) and focus on a more tangible indicator: media attention. Are these countries currently making headlines? If yes, it might be wise to steer clear of selling those insurance contracts. But in quieter times, like now, it could be an opportune moment.

What we also like is the rapid return on capital. You can put the trade on one day before the expiration and have your margin available at the close the next day.

However, always keep your position sizes within reasonable bounds. Every so often, unexpected events will trigger market volatility, and as the insurer, you'll be on the hook for the costs.

Be sure to follow us on Twitter @Sharpe__Two for more of our insights. If our work resonates with you, don't hesitate to share it with others who might find it helpful.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

Data, charts, and analysis are powered by Thetadata, Dataiku DSS.

Have access to our indicators using our API.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.