Another Friday, another round of fireworks. Despite the SP500 closing the week down by a solid percentage point and the Nasdaq shedding 3.5%, we witnessed one of those end-of-month rallies for the ages—adding 2% in the final two hours of trading.

According to , this was the fourth most powerful end-of-month rally on record, with the SP500 gaining a full percentage point in the last 30 minutes and a staggering 40 handles in the final 15.

There’s always a lot of hype (and some fantasy) around options expiration flows. From a retail standpoint, the end-of-months are much easier to grasp and, while undeniably strong at times in 2024, we’ll need to keep a close eye on them in 2025.

Especially since the mood has shifted throughout February. At the start of the month, the market was still trying to make sense of all the new variables—DeepSeek, the tariff war—but by the end of the month, the sentiment felt more like “cover your back first, ask questions later.”

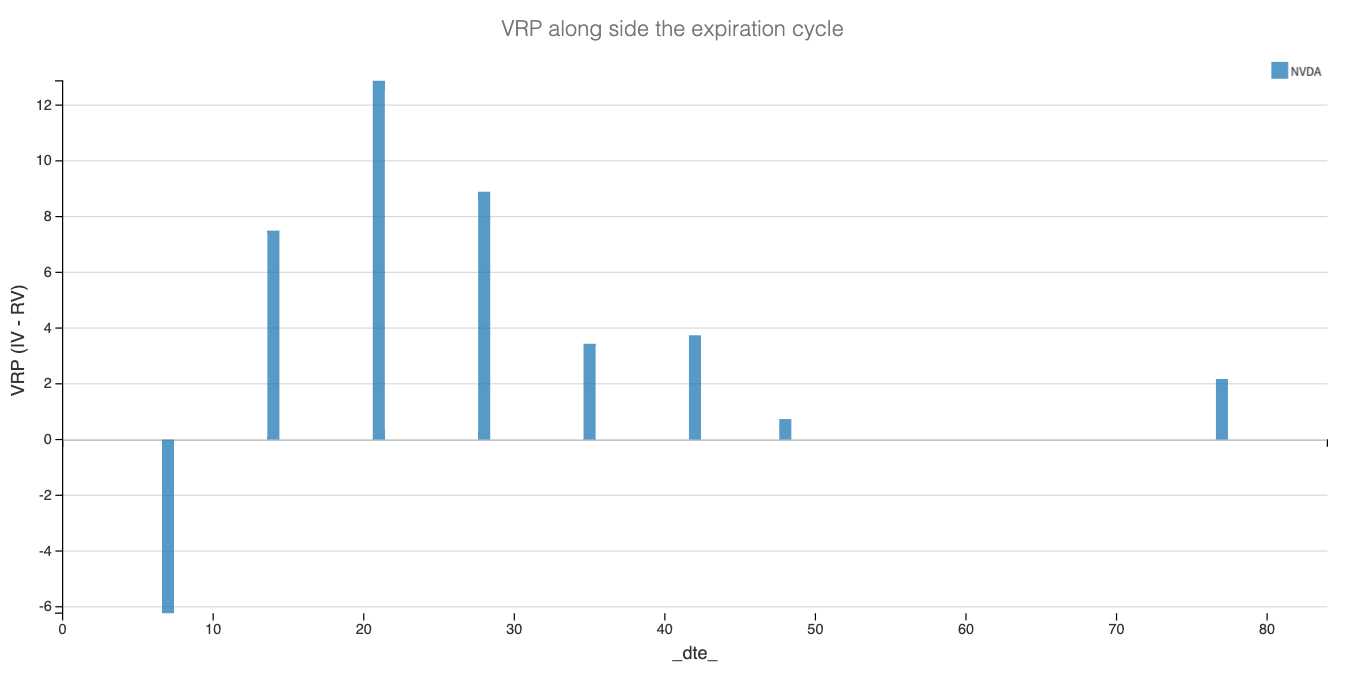

Take NVDA, for example. Despite delivering another stellar report with 80% year-over-year growth, the stock barely reacted on earnings day and sold off the next. By Friday’s open, it was down a solid 10%, only to claw back half of those losses by the close, thanks in part to end-of-month flows. Given NVDA’s realized volatility, nothing catastrophic—but another subtle sign that the market isn’t entirely oblivious. 80% growth is great, but it’s still too early to gauge the true impact of DeepSeek on hardware investments.

While implied volatility continues to absorb most of these price swings, be cautious with short-dated options, where gamma risk is highest.

Another under-the-radar signal this week—BABA. After an incredible run since the start of the year, fueled like many other Chinese tech stocks by the DeepSeek hype, the stock dropped nearly 10% on Monday after announcing… well, a hefty investment in hardware and infrastructure. Could this become the new norm in 2025? Investors scrutinizing large capital expenditures more closely, demanding more before signing blank checks? It’s possible.

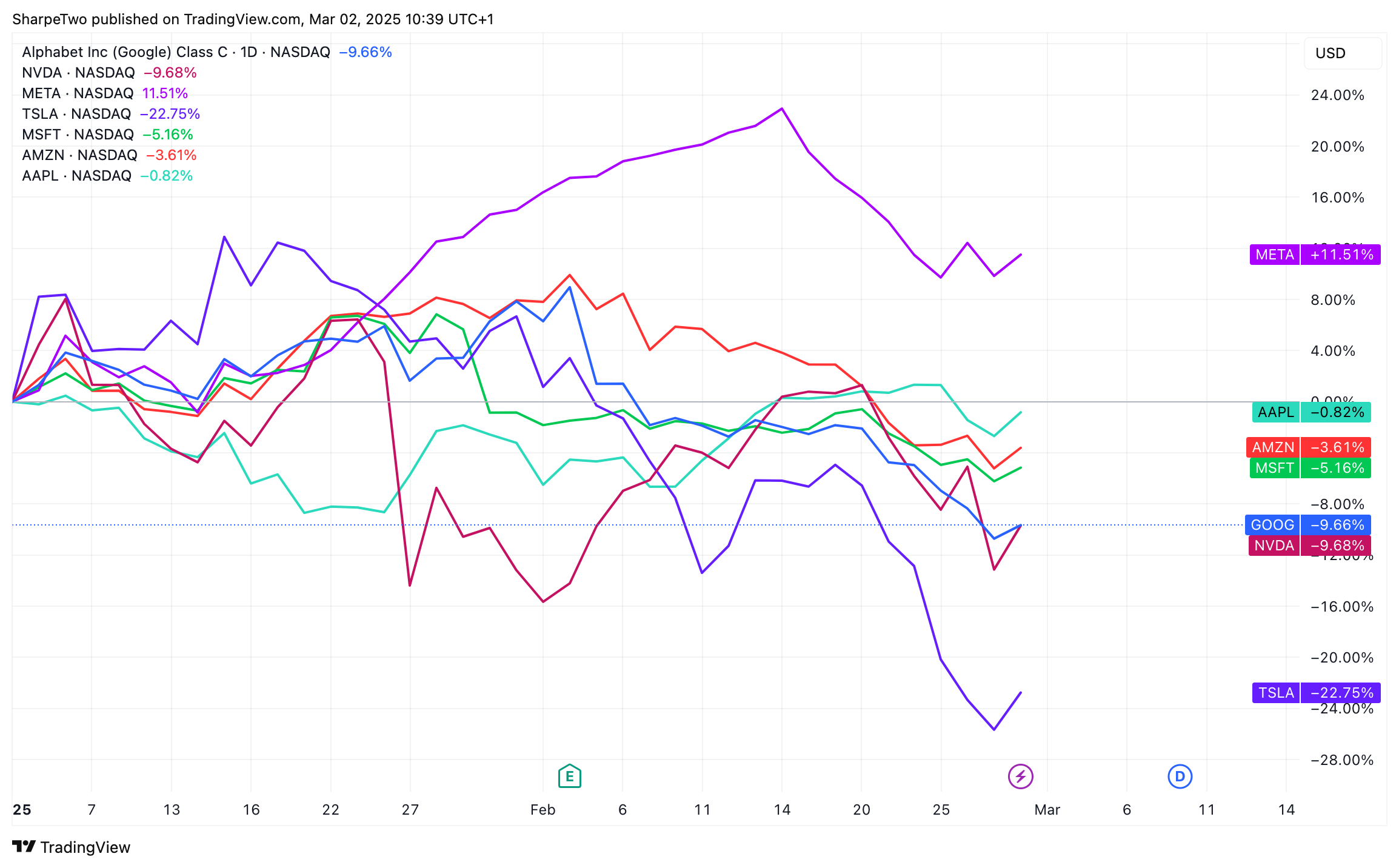

Another example—TSLA. The stock is down 25% since earnings (and it could have been closer to 30% if not for Friday’s rally), with even JPM losing patience over the company’s lack of substance.

Meanwhile, AMZN, MSFT, and GOOG are all moderately down (-5% to -10%), but still down nonetheless. And if not for META—which, despite being **up 12% YTD, has shed 12% in the last two weeks—the “Magnificent Seven” wouldn’t be looking so magnificent in 2025.

From a volatility perspective, this matters— a lot and not only because we pointed this week that puts in the tech sector may be expensive. These seven stocks make up such a massive share of the main U.S. indices that a shift in sentiment around them could be the real reason why the VRP is back.

Are we buying puts again because we’re genuinely worried about the economy? Or is it because we’re finally looking at some of these multiples and remembering that—even the most magnificent trees, when they grow too close to the sun, eventually burn?

We don’t necessarily have a clear answer to that. Based on the latest economic data, many in the market are already pricing in a much larger recession. We've even come across wilder theories suggesting that the U.S. President and his administration might intentionally orchestrate a recession to trigger a round of rate cuts and potential QE.

The problem with these theories? We’ve been hearing variations of them for the past three years. Decrypting what’s true or false is far above our pay grade. But what’s interesting for us, once again, is the shift in market sentiment.

A year ago, the focus was "when will the rate cuts start?" Six months ago, it was about how business-friendly the election winner would be. Now, those concerns pale in comparison to the genuine uncertainty driving the market today.

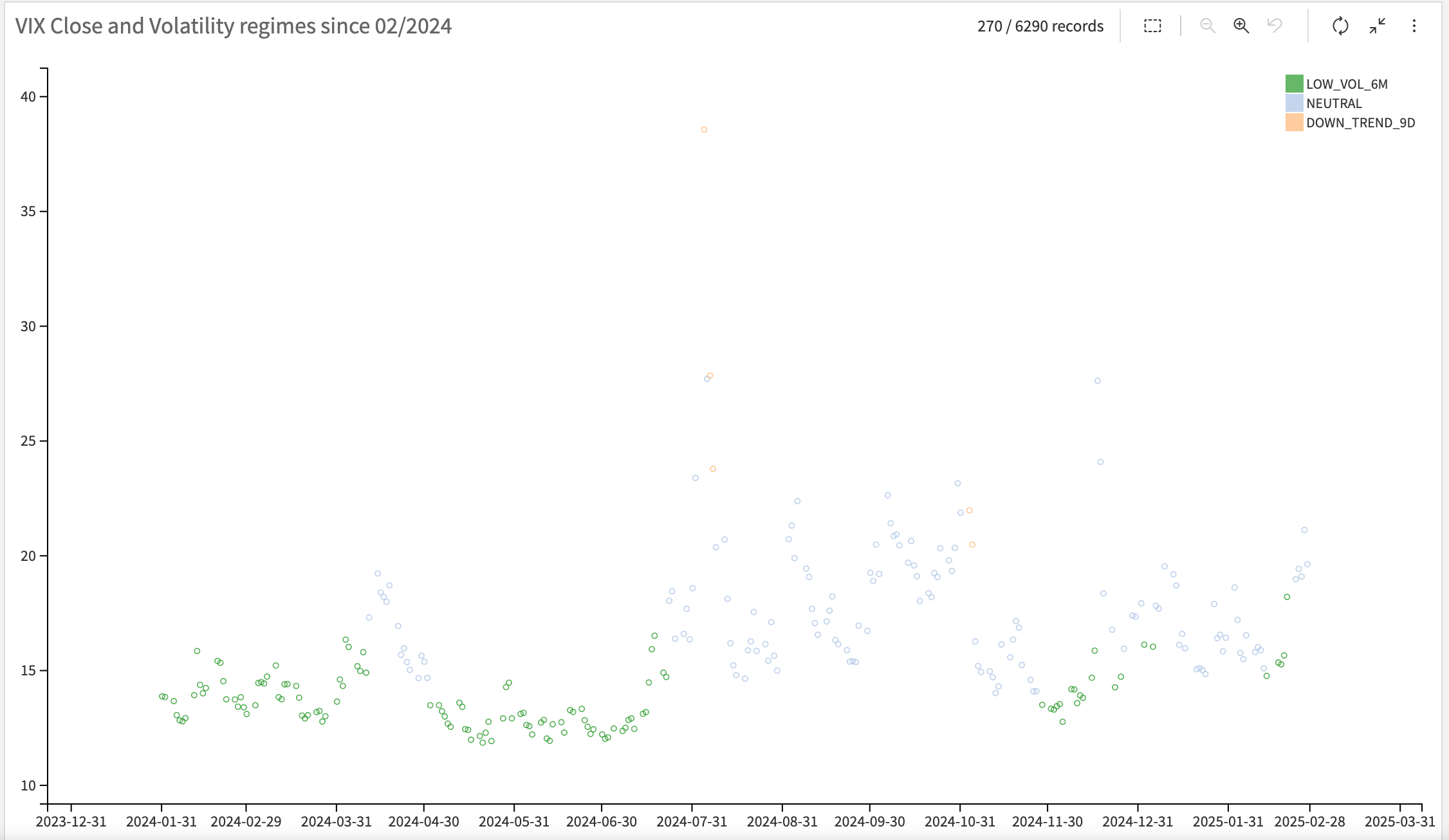

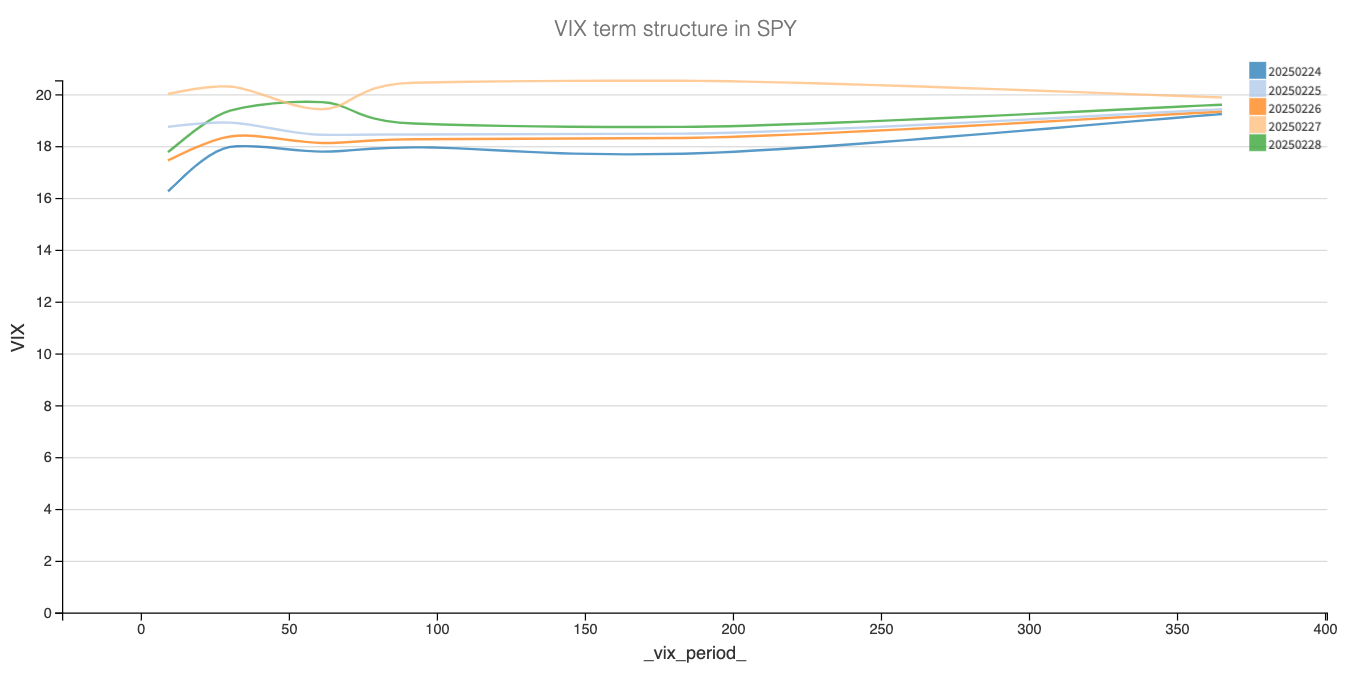

One of our favorite indicators for gauging market uncertainty is the shape of the VIX term structure—and right now, it’s as flat as North Dakota. But notably, it’s also much more elevated compared to current realized volatility.

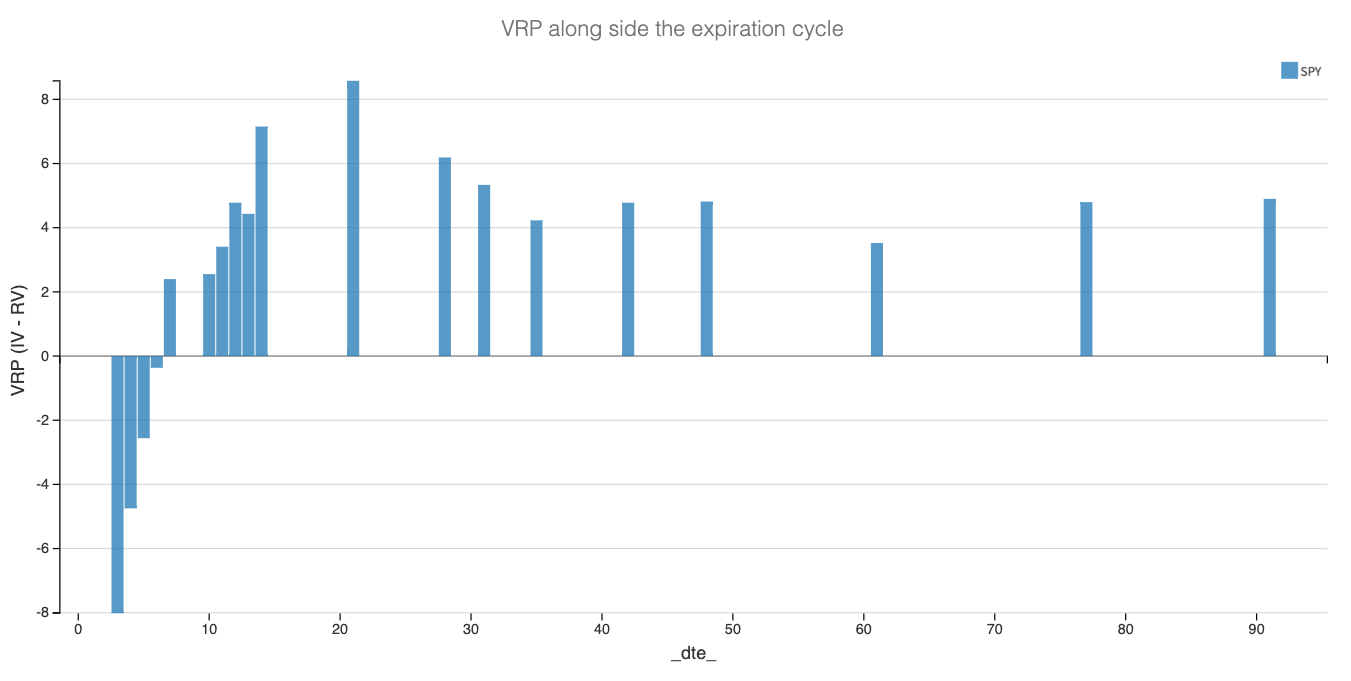

As option sellers, we’re happy to see the VRP making a comeback. But let’s not forget: people don’t buy options because they’re stupid. They buy options collectively because they see risks worth hedging ahead.

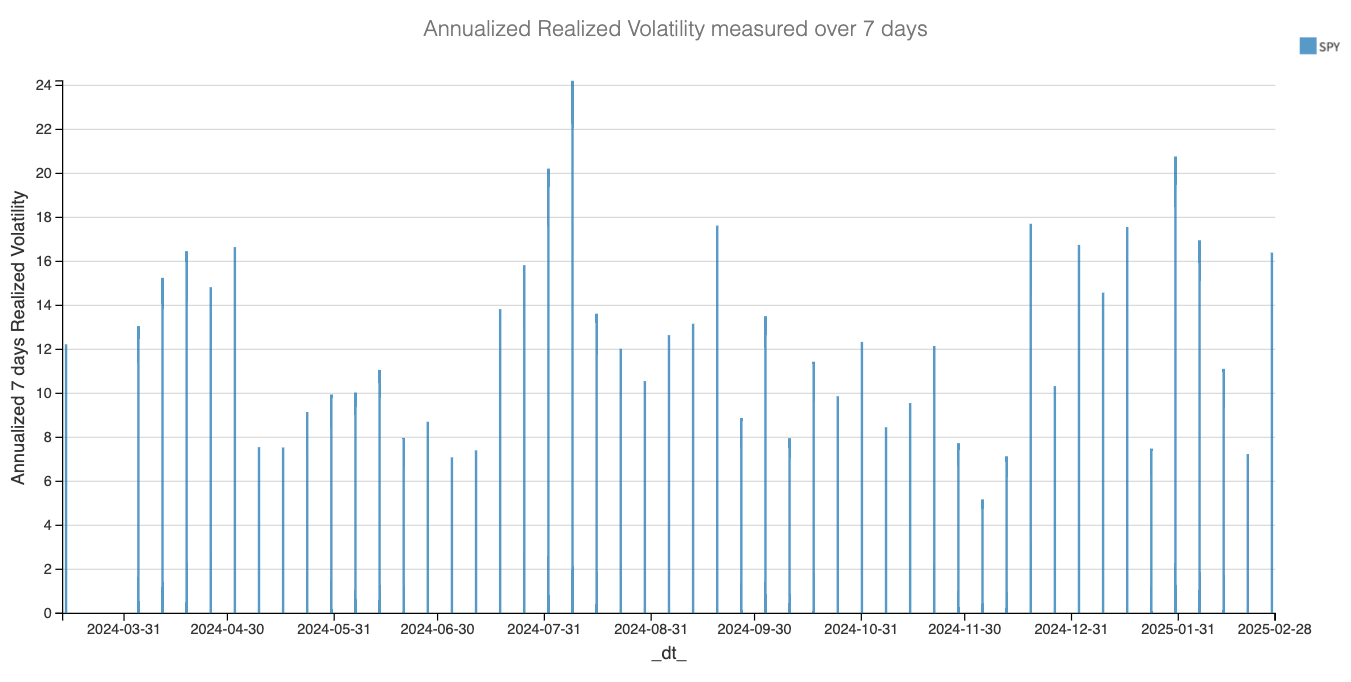

Our job? Assessing whether those risks are worth taking. And for that, we need to look at realized volatility. While it had been drifting lower over the past few weeks, it has ticked back up over the past few days.

Especially as we head into another round of macro data-driven trading. Next week, we get the monthly jobs report, which will be dissected for any confirmation of a significant economic slowdown. The following week? Inflation numbers. Then comes the March FOMC meeting. And on top of that, we have March OPEX—which, if you care about options expiration flows, focus on the quarterly ones and ignore the rest.

Bottom line: we don’t expect things to calm down anytime soon. Get used to it. It may look chaotic, but these back-and-forth swings between VIX 16 and 22 are totally normal—and, more importantly, tend to be quite profitable for those who trade them well.

Sharpe Two is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

In other news

We were quietly waiting for the end-of-month trade when the schooling of Zelenskyy by Trump and JD Vance took over every single thread on social media. This might just be the most humiliating moment in diplomacy we’ve seen in the past 15 years—closely followed by Hu Jintao’s removal during the last Chinese Congress.

There are a few key takeaways. The most obvious? Relying on someone else for your security is an enormous risk. The black swan that no one saw coming (or were too busy debating shades of grey and black to notice) was the U.S. abruptly shifting from global policeman to full-on America First. Europe was effectively short vol—and suddenly, vol spiked to levels no one expected.

This is a stark reminder that we need to be extremely cautious about our assumptions of the world order—what should be and what actually is. Anything can happen, at any time.

One example we love? Bitcoin—the global currency of the new world order, for sure. Now that Trump is backing it, Wall Street is trading it, and white-collar criminals entrepreneurs are embracing it, we’ve reached a new phase, right? So nothing to worry about the -20% over the last weeks … right??

Thank you for staying with us until the end. As usual, a couple of interesting reads from last week:

- We’ll be honest—we still haven’t finished that very dense three-part series on what the adoption of very short-term futures could look like. Why is this one different and worth your time? Because it’s not just good—it’s detailed and precise, skipping the usual prediction fluff to lay out, in realistic detail, what the economics, business models, and research around AI might actually look like.

- A year ago, we were writing to you from Mexico, and we loved every moment of that trip. Here’s an old Tumblr post by Anthony Bourdain that captures, in much better words than we ever could, the rich and complex emotions we felt while we were there.

That’s it for us this week. Wishing you a great week ahead—and happy trading.

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.