Forward Note - 2025/01/26

Data-dependent and cautiously optimistic.

Equity markets rose steadily this week as President Trump took office on Monday, riding the wave of relief generated by last week’s CPI numbers. The US economy might not be running as hot as some feared, which was enough to sustain positive momentum and push the SP500 to an all-time high by Thursday. Despite a slight dip on Friday afternoon, the SP500 closed the week up 2.7%, while the Nasdaq posted gains of over 3%. The VIX, meanwhile, dipped comfortably below the 15 handle, settling at 14.85.

The pressing question now is whether all the tension that built up at the end of 2024 has truly dissipated—or if this is merely the calm before the next storm. Some clues may surface next week during the year’s first FOMC meeting. While it’s widely expected that the Fed will hold rates steady, Wall Street will be laser-focused on Powell’s press conference. The reasons? Plenty—and they matter.

First, Powell will likely face questions about his remarks from the last presser, which sparked the latest bout of market volatility. While we don’t expect him to say anything groundbreaking—likely reiterating the standard lines about being data-dependent, two rate cuts in 2025 if conditions allow, and fewer if they don’t—it will still be worth noting whether recent economic data has nudged him toward a more dovish stance for the year or if the committee remains fixated on the threat of inflation re-emerging.

That brings us to the second key point: with the new President now in office and wasting no time signing a flurry of executive orders and some remarks on how he will demand the Fed to cut rates, it’s almost certain Powell will be asked if these policies could influence the Fed’s decision-making process.

The likely answer? A polite yet unequivocal no. But, as always with the market, it’s the little details that matter. What subtle phrase or inflection will traders latch onto this time, and could it be enough to set off yet another spiral? Only time will tell.

At a VIX of 15, it seems clear that inflation concerns have taken a backseat, with the market now waiting for proof to come from actual data rather than the committee’s rhetoric. Yes, rates remain high, and sure, a 30-40% market drop is always within the realm of possibility. But isn’t that true at any time, for any number of reasons?

For now, we cautiously align with the camp of “VIX 15 tells you everything you need to know.”

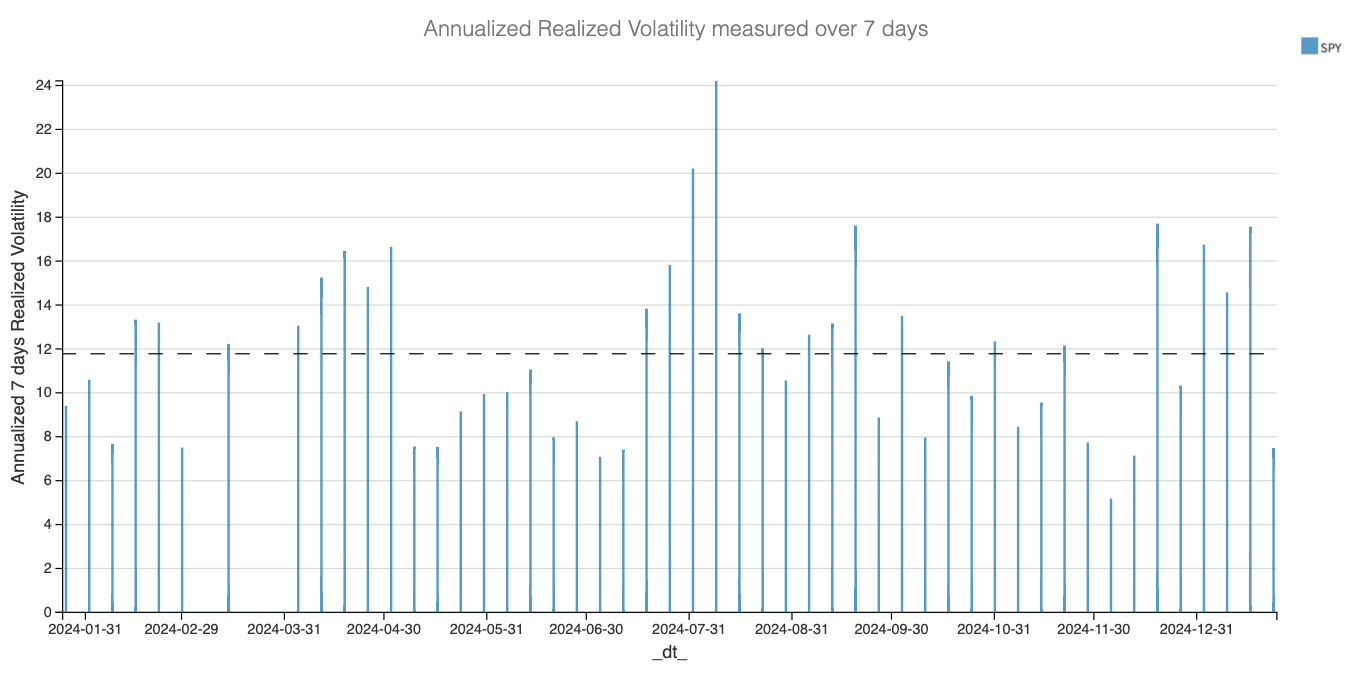

That said, we can’t deny that this has been a rather unusual month. Realized volatility has remained elevated for most of it, only taking a meaningful dip this week.

With two remarkably calm trading days on Thursday and Friday, we’ve finally dipped below the 8% weekly threshold—bringing us back in line with the median level observed over the past year.

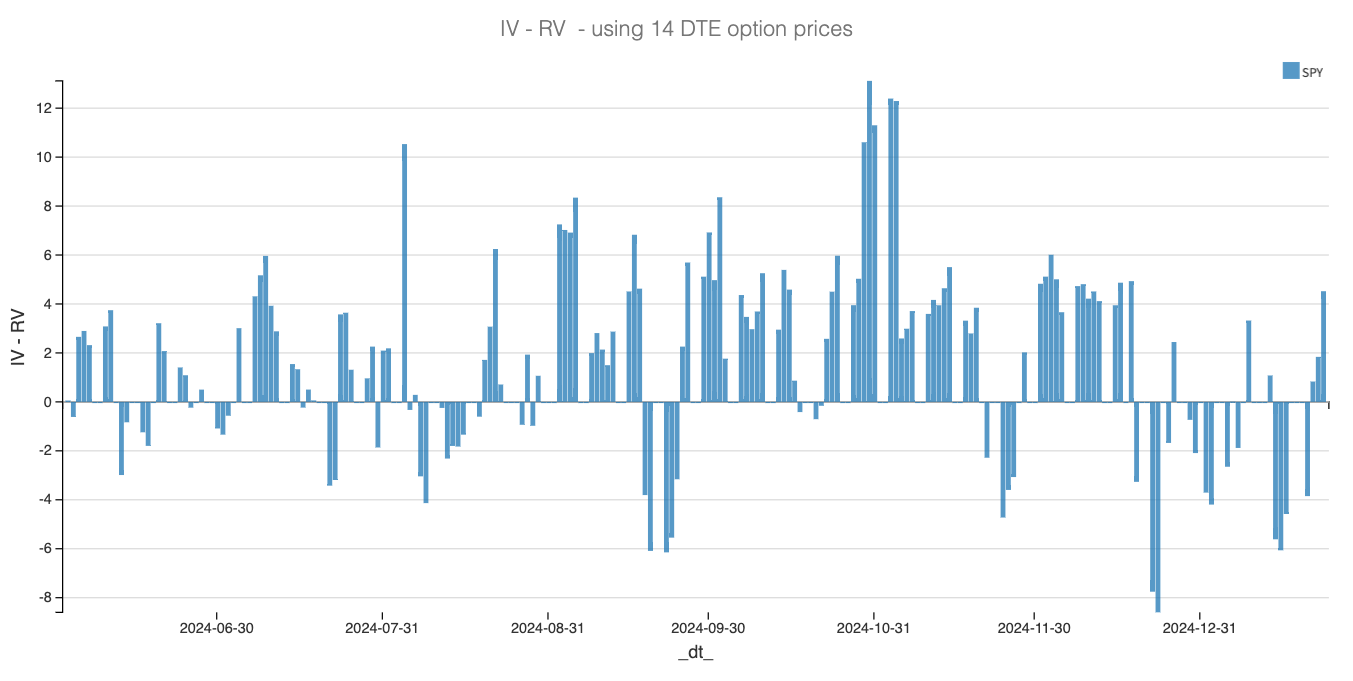

Despite the larger-than-usual intraday swings in January, implied volatility never truly took off to provide adequate compensation for the risk taken in the SP500. In fact, as we noted on Thursday, some of our indicators were signaling potential long volatility opportunities due to the significant compression of the Variance Risk Premium.

However, with the recent dip in realized volatility, the premium may be starting to re-expand—particularly in shorter maturities.

Under normal circumstances, that would be enough for us to jump back into the trade. But with a packed calendar next week and our realized volatility forecasts still pointing higher than where implied currently trades, we’ll wait for a better setup.

We can’t deny that this marks a significant improvement from last week, when monthly realized volatility flirted with the 16 handle, and the forecast remained at 18. With this week’s forecast down to 14, and assuming nothing substantial emerges from the Fed press conference or the earnings reports from major tech players, we could see a return to more favorable market conditions for volatility sellers.

That said, our stance remains unchanged from recent weeks: 2025 is already shaping up to be markedly different from 2024. Buying protection should be a routine part of any strategy to guard against sudden downside surprises. As one of our Discord members astutely noted this week, while the VIX hovered near 14, the VVIX held steady in the 100s—an important signal that the market’s demand for protection hasn’t entirely faded.

This is purely a hypothesis on our part, with nothing concrete to back it up: it’s entirely possible that the market, learning from the two major spikes in H2 2024, has adapted. While it might not be aggressively buying tails in the index, it seems to have shifted that activity to the VIX options complex. This would make sense—after all, we witnessed significant volatility blow-ups last year without corresponding major pullbacks in the broader market.

The effectiveness of this hedging method is, of course, up for debate. (We lean toward skepticism—how many stories have you heard of someone properly hedging their book with VIX options? Not many. But, what do we know?) The more important takeaway for the rest of us mere mortals lies elsewhere: the market is clearly more hedged now than it was last year. And if the professionals are gearing up, you should be too.

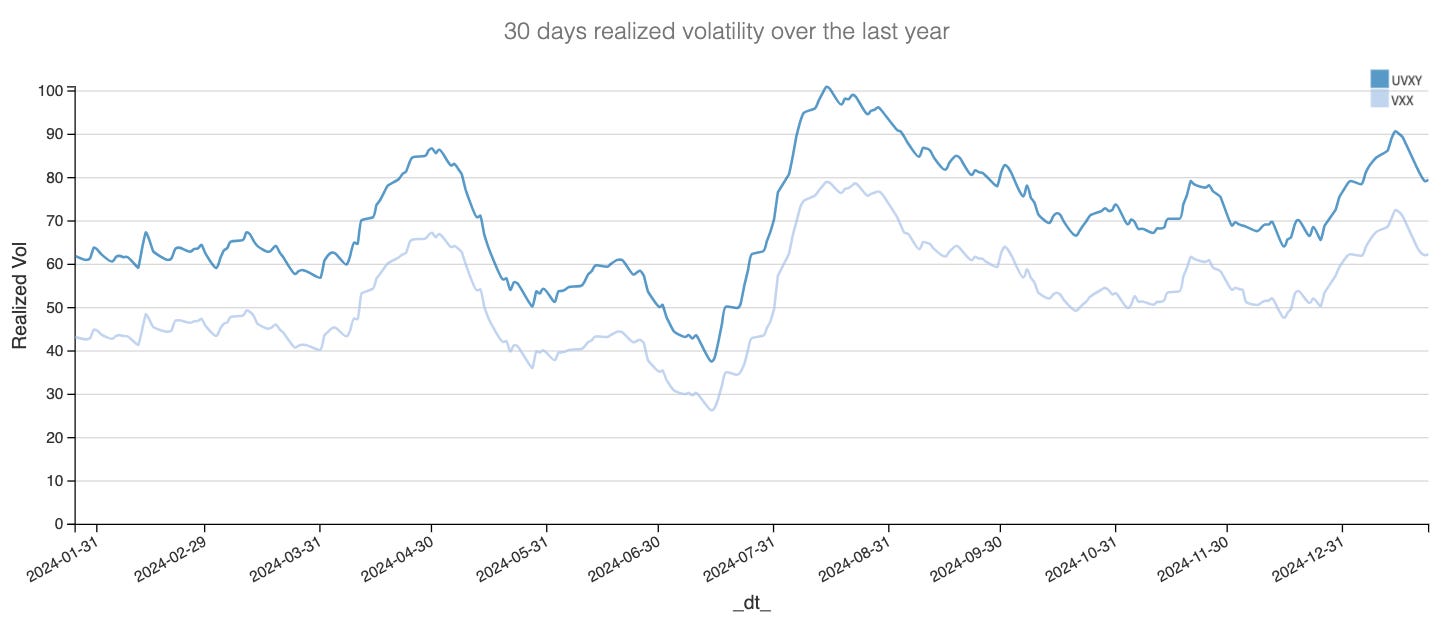

Another key takeaway is that one of our favorite trades may be making a comeback. With VVIX elevated, the VRP in VIX-related products should be materially larger than in 2024. Right now, however, that’s not entirely the case: realized volatility in VXX options at 30 days, for example, is gradually declining, and as a result, the VRP is turning positive again.

Even with a VRP hovering near zero in vol-of-vol trades, the market still demands more compensation than what will likely be realized. This is no surprise—the market is rarely generous without reason.

That said, 2025 is not 2024. While this trade was a staple for us last year, we’re approaching it with more caution this year. Humility is essential when interpreting the collective views embedded in prices. An elevated VVIX may simply reflect a higher probability assigned by the market to another VIX spike. This is not the time to go all in on short vol-of-vol trades. Adaptation and restraint will be the name of the game in 2025.

In other news

Hedge fund manager Liang Wenfen has achieved a breakthrough by releasing DeepSeek R1, the first Chinese LLM to rival OpenAI and Anthropic. Up until now, you might think: who cares? But here’s where it gets interesting—not only did they publish the exact methodology of how they built it (wasn’t OpenAI supposed to be the champion of building models for humanity?), but they also accomplished it with significantly fewer resources.

It’s another reminder that there’s no true moat in being an LLM architecture provider. The race to develop the best models is ultimately a race to the bottom, capped by the asymptotic limits of what is technologically possible, in particular with chips and realistic human-generated data. Yes, AI will undoubtedly transform the world. But increasingly, it’s less about architecture and more about business execution. With quality data from specific industries, we’ll soon see the emergence of tailored applications leveraging APIs from these architecture providers.

Oracle was revolutionary for a time, but in the end, it was just a database seller and a (powerful) business enabler. After the dot-com bubble burst, it took over a decade for its stock to hit new all-time highs. OpenAI and Anthropic are not so different. This week’s news is a timely reminder that, while their valuations are ballooning, they represent the beginning of the AI story—not the end.

Thank you for staying with us until the end. As usual, here are a few interesting reads from last week:

Trump took office this week—and reportedly got about the equivalent of 57,250 BTC (or 6 billion USD) richer—by capitalizing on his popularity and issuing a coin to monetize it. You already know what we think of these shenanigans, but why not read kyla scanlon take on it?

We began our trading career in 2011 dabbling in Short-Term Interest Rate futures, and seeing an article that breaks down how they work and the strategies that accompany them filled us with nostalgia. If you're curious, here's a fantastic read from Paper Alfa .

That’s it for us this week. We wish you a great (and hopefully calmer) FOMC week ahead. Happy trading!

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.

The content of the note recommends being cautious of short vol trades given VRP compression. However, with the VVIX > 95, are you still executing the overnight SPX trade as recommended on previous posts.

So happy to see a recommended link from Kyla! Her content and explainers are fantastic, and so is her book.