Does selling 45 DTEs really work?

Looking for whales in 2024

It is “easier” to make money selling volatility in low-volatility regimes. Stock tends to drift up, but the realized volatility is much lower than what was implied by the market participants.

These periods of high win rate open the door on the development of systemic approaches to harvest as much profit as possible. There is nothing wrong with that. The problems arise when we stick to these principles while the market entered a different regime. Or worst, when we build rules on the wrong cause - like theta, for instance - instead of the real pnl driver: price distortion.

You are making money in the market only because you manage to buy something cheap and sell it expensively. It may sound obvious, but someone completely new to options trading and with social media as sole reference could think that he is making money because time is passing.

As such, our readers often mention that the optimal timing for selling options is 45 days to expiration (DTE). This advice stems from a popular options trading network that has significantly contributed to democratizing options trading over the past decade. While their influence is undeniable, and they've done much good to the development of retail option trading, we felt compelled to investigate this claim ourselves.

Ultimately, this article tries to identify which segment of the expiration curve offered the most success in 2023 for volatility sellers. It doesn’t mean it will necessarily be the best place to sell options throughout 2024, but at least it will give some things to think about.

The assumptions made for the backtest

Let's outline the conditions of our backtest.

Regular readers of Sharpe Two may know now that we focus on a broad spectrum of ETFs spanning various asset classes and geographies. That represents 66 tickers; the full list is available through our API. For this backtest, we've operated under the assumption that we could sell straddles at the mid-price at 3:50 pm. We then held the position for two weeks before exiting at mid-price at 3:50 pm.

Additionally, we've standardized the test to $1 of credit per trade. This means that in real trading, you would need to adjust the quantity of straddles sold to maintain consistent credit across trades. This approach also guarantees a fair comparison of performance throughout the expiration cycle.

While all these conditions - especially the timing of the execution at mid-price - might be challenging to replicate in real trading scenarios, they offer valuable insights into the potential outcomes of a simple strategy relying only on the number of days to expiration to find opportunities.

What are we looking for?

Let's take a step back and explore the rationale behind this approach.

The options market primarily serves as a haven for fund managers aiming to hedge their portfolios against unforeseen risks. When they do so, they tend to be relatively indifferent to pricing. As a matter of fact, their primary concern is not the cost but the necessity of protection, dictated by their obligations to clients and internal risk management policies. Consequently, their purchases characterized by large amount in dollar term - something hard to comprehend for retail traders - often result in elevated option prices, as they are willing to pay what's required to safeguard their holdings. In other words, they follow a “Better safe than sorry approach” for risk mitigation rather than bargain hunting.

Considering the busy schedule of fund managers, who balance reading financial reports, interviewing CFOs, and meeting with analysts, buying insurance for their portfolios isn't an everyday task. It's typically done at set intervals—weekly or monthly. Hence, finding an advantage in the options market often involves anticipating when price-insensitive buyers — whales — will make moves creating opportunities or "waves" that can be capitalized upon.

How did selling 45 DTEs straddles perform in 2023?

This brings us to the original hypothesis of this article: whether selling options at 45-day-to-expiration (DTE) is an optimal strategy, and if it is not, what is the part of the expiration cycle where we observe the waves made by fund managers, buying options in bulk.

Our analysis begins by charting the average returns from selling straddles and the frequency of trades executed for each Day to Expiration (DTE) segment. Our evaluation focuses only on weekly DTEs — multiples of seven for clarity and simplicity.

The chart reveals a higher volume of trades within the 7 to 14 DTE range, attributed to the availability of weekly contracts in numerous ETFs within our study. Following the same observation, you see a higher number of trades between 21 and 42 DTEs as a result of monthly contracts being more frequent than quarterly contracts.

Upon examining the average returns, several intriguing patterns emerge. Selling options in the back months (63 and 56 DTE) appear to yield favorable outcomes, contrary to the 42 to 49 DTE range, which, on average, does not exhibit the same level of profitability. Remember, this was only for 2023, but already an important conclusion.

Conversely, options in the front month are typically overpriced, and it is no surprise to see this part of the curve leaning on the positive side on average.

To translate these observations into tangible insights, we next explore the profit and loss (PnL) outcomes, providing a clearer picture of the financial implications of these trading strategies.

The pattern observed mirrors our previous findings, reinforcing the idea that selling options between 49 and 42 DTE typically does not bode well for traders. At least in 2023, entering the market earlier was often more advantageous, or a few weeks later, to capture the moment where the Variance Risk Premium tends to increase as we get closer to expiration.

This makes sense to a certain extent - as a fund manager, you would buy one month, two months, or 3 months before expiration and not randomly between months 1 and 2.

Therefore, if you really want to capitalize on price distortion, you could sell options with 30 Days to Expiration (DTE) while concurrently buying protection for options with 80 DTE. Similarly, engaging in transactions with 63 DTEs, securing them with options at 100 DTE, and then reassessing and adjusting the position after two weeks to align with the most beneficial DTEs could yield positive outcomes.

Essentially, selling the front months and hedging with the back month is a sensible approach to developing an options portfolio, especially when you observe some contango in the volatility term structure - which was the case for most of 2023.

The further away you are, the smoother the results.

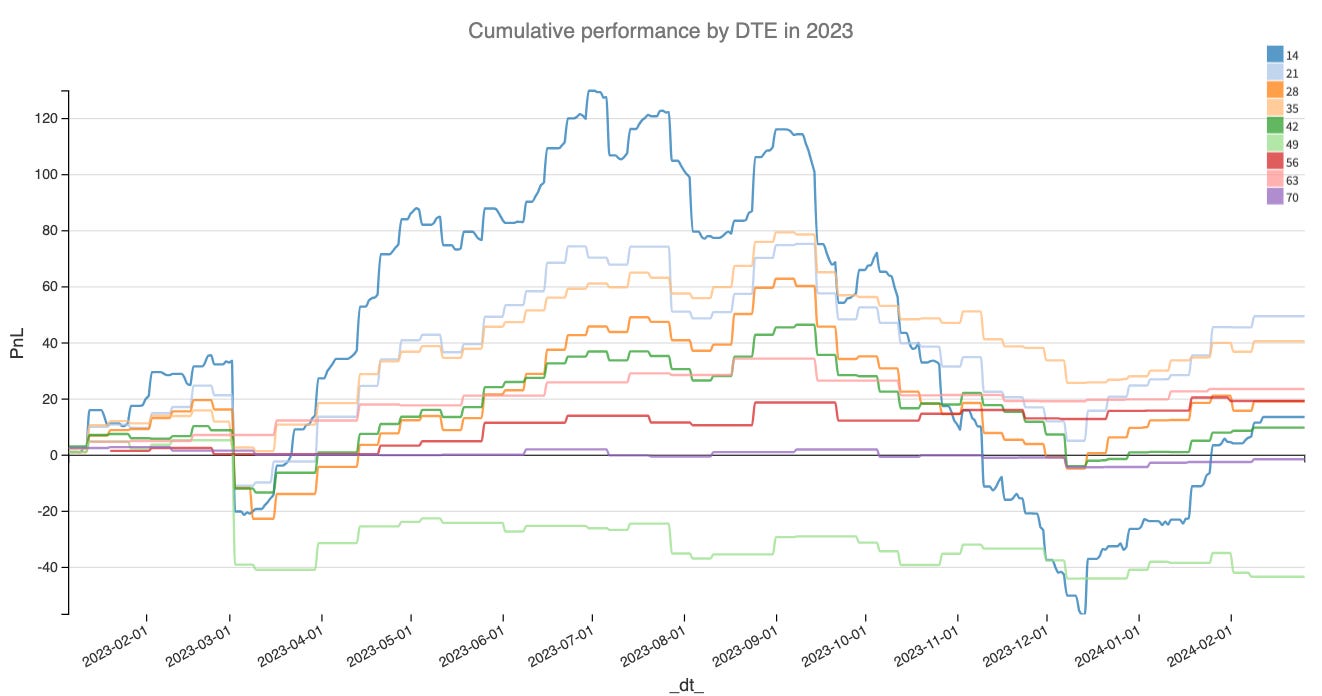

Next, we dive into the PnL curve by DTEs for 2023 to assess not just the profitability but also the stability of returns. A consistently positive PnL is desirable, but the ultimate goal is to achieve this with minimal variance, ensuring that gains are made in a steady and predictable manner.

As anticipated, the highest level of variance, by a significant margin, is seen at 14 Days to Expiration (DTE). This phenomenon aligns with our discussions in previous articles about the implications of high gamma exposure. High gamma exposure at this stage indicates a heightened sensitivity to rapid and pronounced movements in the underlying asset's price, susceptible to testing the boundaries of straddles.

As you extend the timeframe away from the expiration date, the observed variance tends to decrease.

This trend suggests that selling overpriced volatility far away alongside the expiration requires less need for constant monitoring and adjustment for a similar level of profitability.

However, it's crucial to understand that this observation does not constitute a standalone strategy. Returning to the average profitability per trade, which stands at 3 cents for every dollar of premium sold at 63 DTE, it becomes evident that focusing exclusively on selling straddles at this particular DTE is not a sustainable or effective strategy on its own.

Exploring additional strategies to enhance profitability is essential, and a good place to start is identifying the specific underlying more susceptible to attracting price-insensitive buyers.

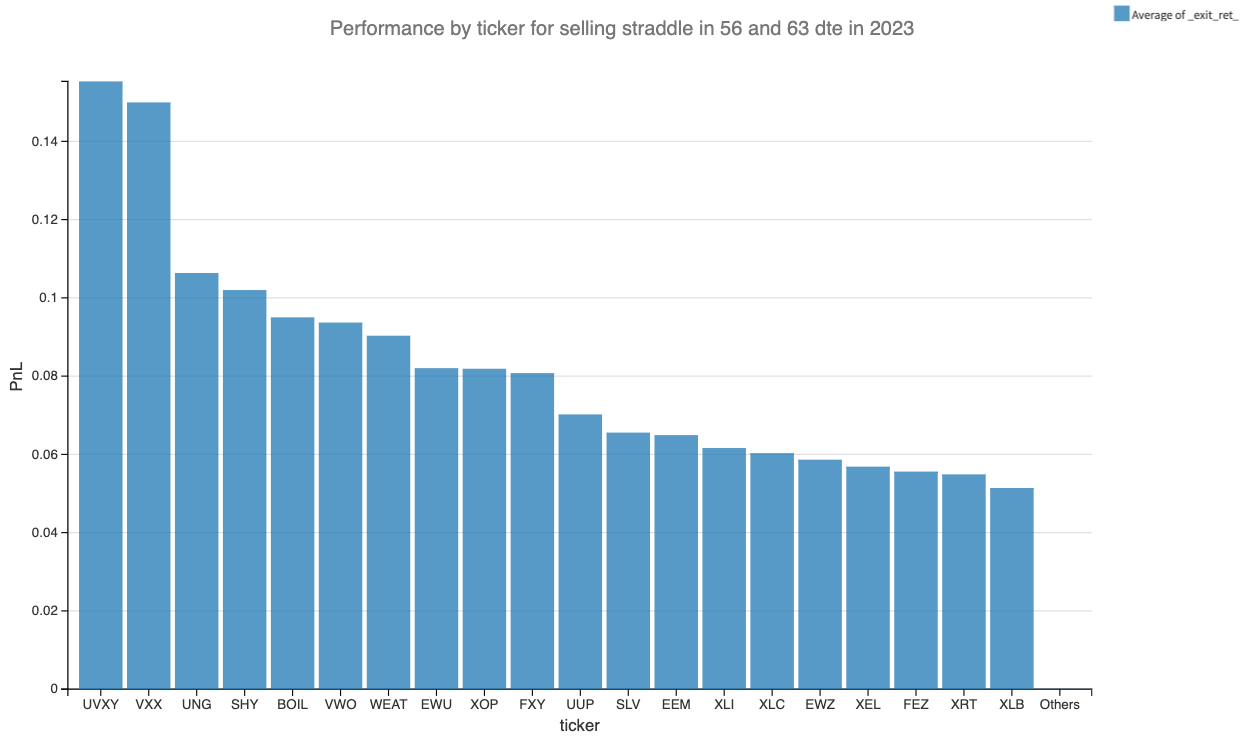

Let’s review the best-performing ETFs at 56/63 DTE in 2023.

This chart reveals familiar names like VXX and UVXY and should not come as a surprise: given the VIX's potential for abrupt spikes, premiums for these products naturally tend to be elevated, reflecting buyers’ and sellers ’ agreement on potential significant movements.

BOIL and UNG, ETFs mirroring the performance of natural gas, stand out in 2023, given the current geopolitical tensions. It's hardly surprising that premiums yielded an average of 10% when held for around two weeks. Once again, it reflects the market uncertainty around the fact that any new development could significantly impact the price of natural gas.

SHY, which tracks short-term US Treasury securities (1 to 3 years), also merits attention. Amidst discussions on the Federal Reserve's policies, selling straddles in SHY was particularly profitable in 2023. Why? Fund managers don’t want to be caught off guard by another violent market reaction and are willing to pay a high price for protection.

Conclusion

Let’s now look at the cumulative performance of selling 63 and 56 straddles in the tickers listed above.

The results are quite appealing. But while it's tempting to look to the past for clues about the future, it's crucial to remember that historical performance is not always a reliable predictor. Or maybe a little bit. The real question to answer is, are we now in a market regime similar to what we observed in 2023?

At a global market level, the answer is no.

But you may answer positively for individual names — the market is probably still tense about the federal rate policy. It is also eyeing the tension in the Middle East to assess the fair price of natural gas. And while the VIX is at 14, it is unlikely that market participants think it cannot spike to 18 in a matter of days and requires protection against such an event.

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.