Trade Anatomy - Short Vol in IBIT

Post Mortem - Signal Du Jour 2025/10/16

Two weeks ago, we presented an opportunity to short volatility in IBIT — and across the bitcoin complex more broadly. It already feels like a lifetime ago, but back then, uncertainty had just crept back into markets, and we were drafting our piece while the VIX flirted with 25.

The day after publication, bitcoin dropped sharply — enough that a few readers wondered if we had mispriced the strangle. In the end, the market came back to its senses and the trade paid off faster than expected. We were out after seven days instead of the usual 14-day time stop. We will see whether it would have been worth keeping the position a little longer — and whether it still makes sense to put it back on at the end of this article.

With this one, our Signal du Jour series now stands at eight out of eight. The best part is that each trade was documented and later dissected here in these post-mortems. You can call it luck but when your edge comes from rigorous predictive modeling, and you simply let probabilities do their job, these are the kinds of results you should expect.

So what are you waiting for to subscribe to our platform? You can build a quant desk, or you can simply rent ours.

The trade

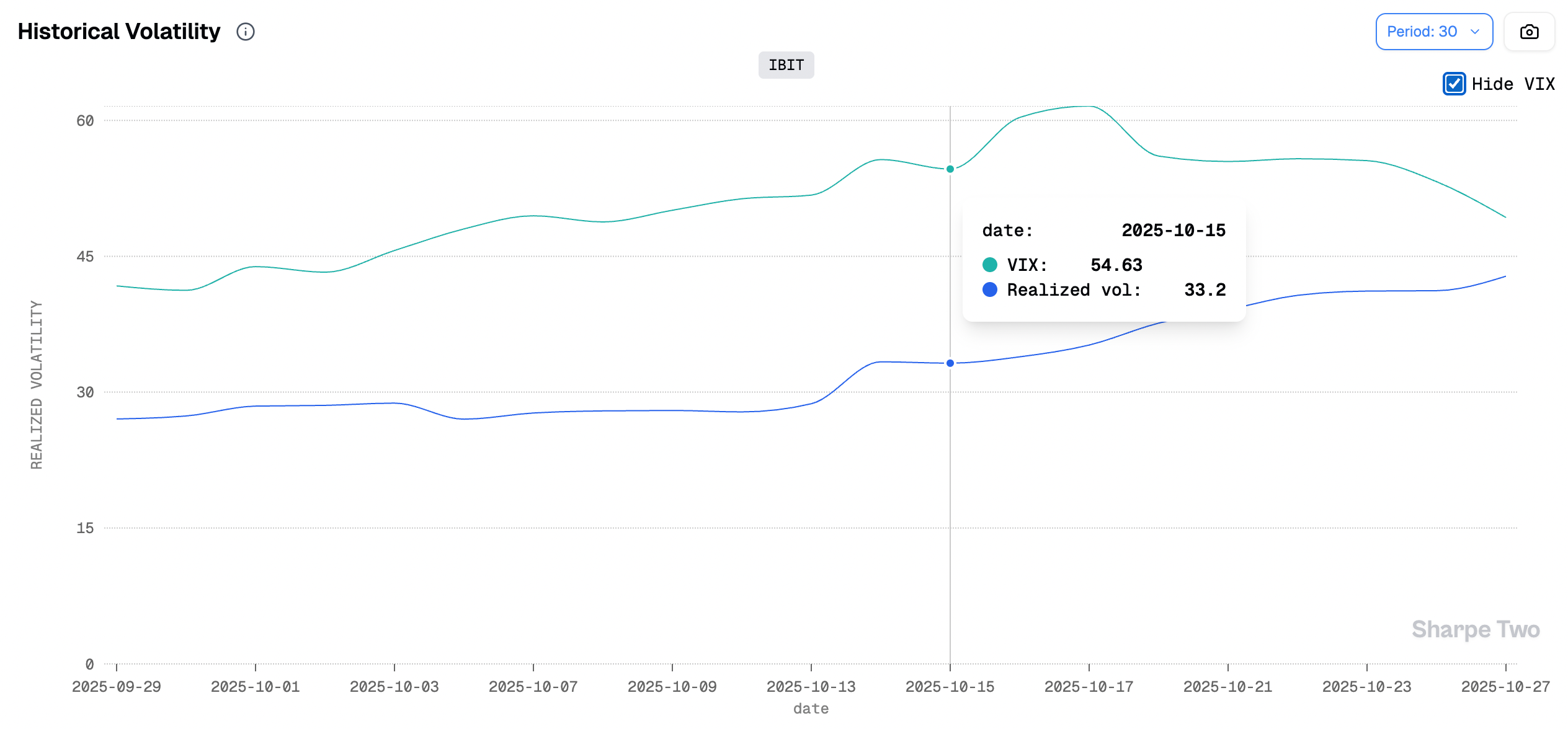

In our Signal du Jour from two weeks ago, we highlighted an opportunity to short overpriced implied volatility in the IBIT ETF, which provides exposure to spot BTC. At the time, bitcoin had just gone through one of its sharpest volatility bursts since April, and the market was growing anxious about a potential shift heading into year-end. Our systems showed the following:

The implied volatility you would have sold then — sitting around 54.6% — had a 75% probability of exceeding the subsequent realized volatility over the next 30 days. We also estimated a 70% chance that implied volatility would decline, making it a key expected driver of the PnL.

That said, realized volatility was almost certain to rise from there (33.2%), which needed to be factored into trade construction. We do not delta hedge, but with such a high probability of realized vol increasing, the choice was clear: either go with a very wide strangle, or — in rare cases — make an exception and ensure you are not caught in a directional trend where the volatility thesis proves correct, yet the PnL ends up in the red due to directional risk.

In the end, both implied and realized volatility behaved almost exactly as expected:

While realized volatility kept grinding higher as bitcoin pared back some of its losses, it rose from 33.2 to 42.8 — not enough to seriously challenge the 54.6% level we sold at when entering the trade. And although implied volatility initially moved slightly against us, it now sits around 49.3%, validating our thesis that implied vol would be the main PnL driver.

Another interesting detail: the VRP was quite stretched at the time of entry — roughly 21 points — but the market has since stabilized, and that premium has narrowed to “only” 6.5. A useful datapoint for anyone deciding whether to keep the trade on.

Now, about the delta risk we mentioned earlier. The underlying dropped sharply right after entry, getting uncomfortably close to the put strike:

When IBIT traded below 60 and implied vol spiked on Friday, a few readers reached out asking what to do. The answer, as always, was in the data: add more, restrike if necessary, or simply let things play out if your sizing allows the underlying to trend. At no point did we think it was time to exit the trade.

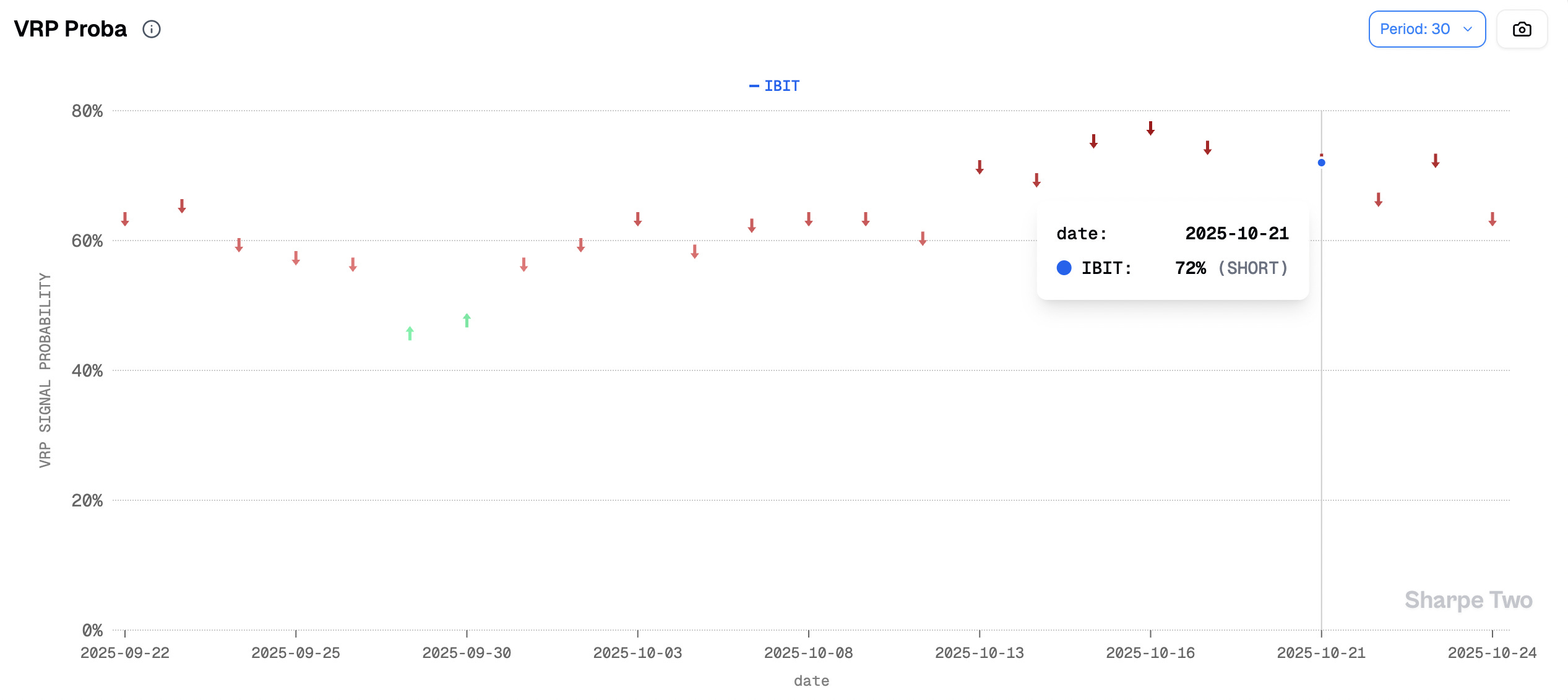

The following day, the probability of profiting from selling implied volatility versus realized volatility had risen to 77% — a perfectly valid cue to lean into mean reversion and sell more to an overly reactive market. In the end, once things calmed down, the edge played out as expected. We exited just a week after entering, helped by three factors: the absence of a sustained directional trend, realized volatility not climbing to dangerous levels, and implied volatility cooling off.

Still, while taking profits at +25% was already more than enough, could you have held for +50% or even +60%? That depends on risk tolerance. But the edge in IBIT remained intact all of last week — a perfect illustration that hitting a profit target is not always a reason to close. Sometimes, the right move is to stay put and let probabilities continue working in your favor.

Let’s now break down the PnL in detail and see how each Greek contributed to the final tally.

The Greek Decomposition

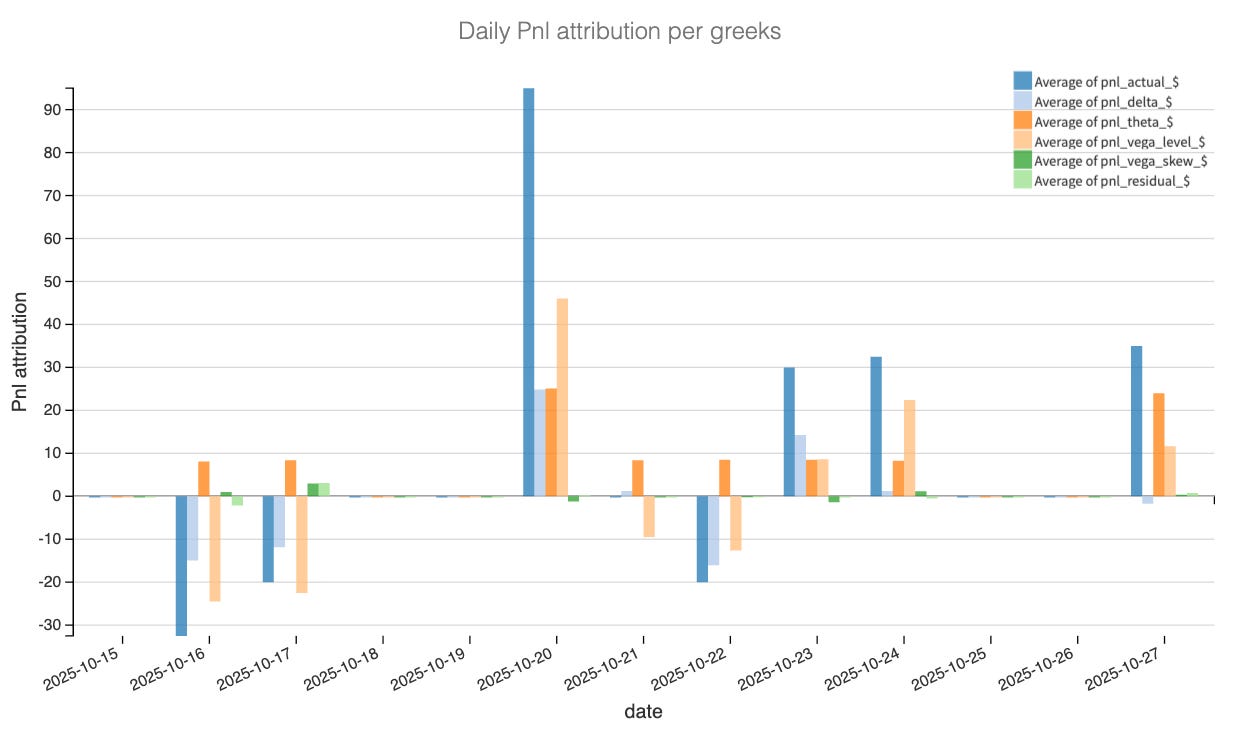

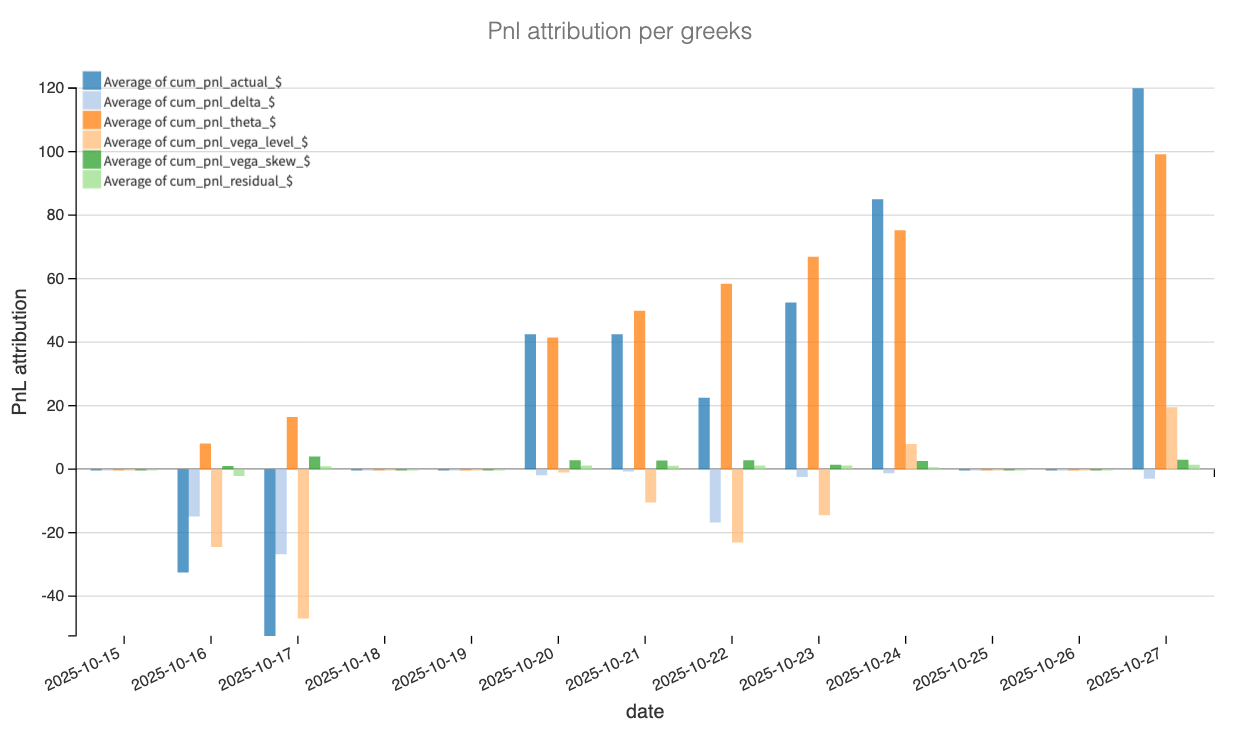

The attribution tells the story we expected.

Carry paid us almost every day and volatility compression did the heavy lifting when it arrived. In the daily chart you can see the early sequence where spot moved against the short strangle first. Around 16–17 Oct, delta was the main drag while theta was positive but not enough to offset the slide. Vega-skew barely mattered. That is typical IBIT when the market suddenly leans into downside hedges: puts fatten a touch but the whole surface is still ruled by level rather than shape.

The picture flips on 20 Oct. Implied came in from the high-60s toward the mid 50s and the vega-level bar towers over everything else. Theta also prints solidly positive on that day. From there, the grind higher in spot plus cooling IV produced a clean two-engine rally in PnL: steady carry and bursts of vega-level wins on 23–24 Oct and again near the exit window. The delta line turns from red to slightly positive late in the sample, which is what you want after the scare: no persistent trend stressing a wing, just oscillation around the middle of the strangle.

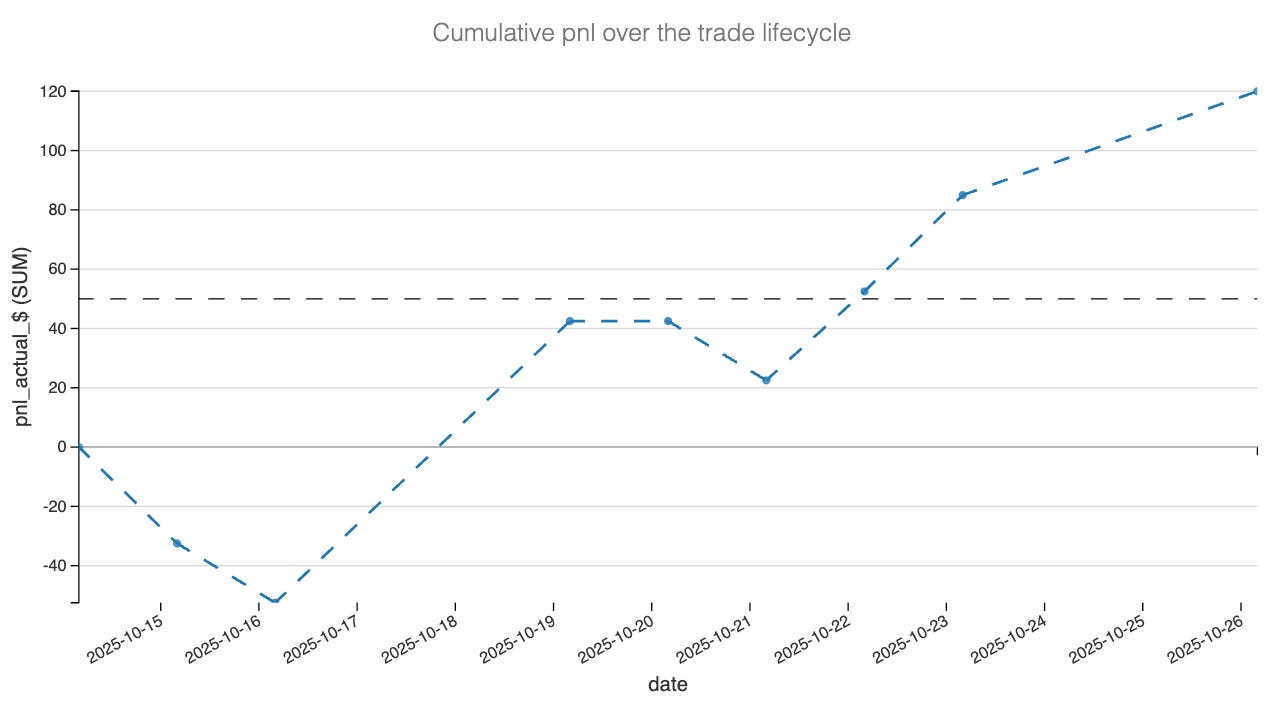

The cumulative chart crystallizes it.

Theta is a smooth staircase up, the metronome of the trade. Vega-level is lumpy but decisive, accounting for the bulk of the gain after 20 Oct. Delta nets out small negative to flat, which validates the choice to stay close to delta-neutral rather than chase a view. Vega-skew remains a rounding error throughout, consistent with a balanced structure where we were not trying to monetize one side of the book. Residual is close to zero, so the attribution behaves.

The thesis played out almost textbook. Get paid to wait, then let IV cool. Carry plus vega-level won the week, and the lack of a sustained directional push kept the position out of trouble.

Now, the real question? Should we put this trade back on. Let’s have a look.