Sunday Forward Note - 2024/04/07

Recalibration week

This week will bring a smile to most traders worldwide—finally, a bit of action after months of a lethargic drift to the upside.

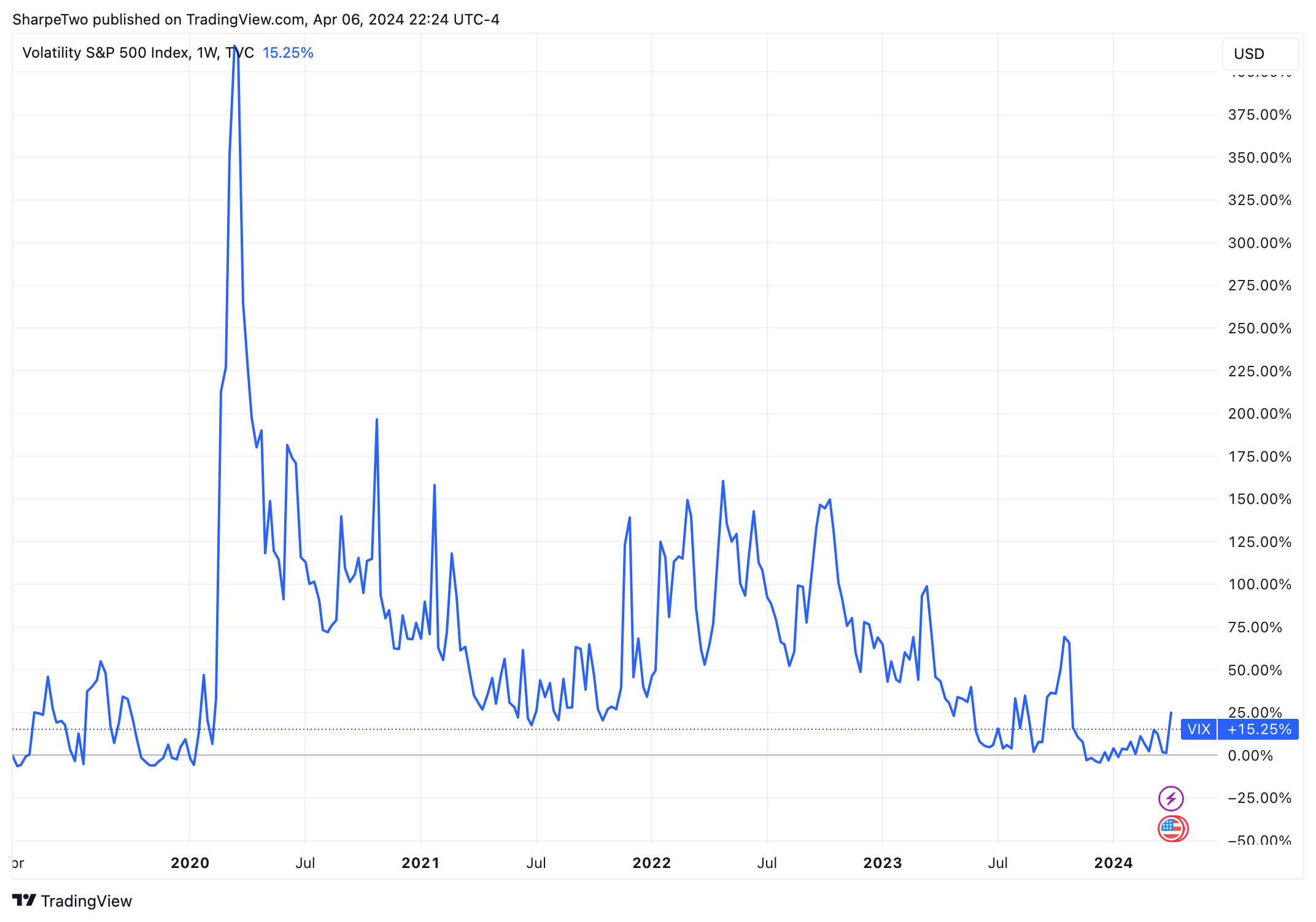

The SPX and the Nasdaq retreated about 0.9%. However, the VIX closed the week above 16 for the first time in 6 months. Is this the beginning of something significant?

The short answer is it’s too early to tell: there's no reason to panic at VIX 16, which is far below the historical average.

Yet, moving from 13 to 16 is no small feat, especially considering the three key characteristics of volatility:

It is neutral and drifts down.

It spikes pretty violently.

It reverts to its mean.

Could this be a spike or at least the beginning of one? Once again, we moved "only" from 13 to 16. We wouldn't necessarily classify that as a spike (yet) but more of a recalibration.

In fact, on Thursday, we witnessed a 10% increase in VVIX, which is substantial enough to grab our attention and provide insight into risk managers' new risk perceptions.

VVIX, or the volatility of volatility, is a good measure of the interest in calls on the VIX options chain. We started the week so low that we shared a slight discomfort with our Discord members in our Sunday pre-market call. We got what we asked for and are much closer to what translates to a "normal" activity level in the VIX options complex. A reading at 90 signals that the demand for calls on the VIX is more in line with what has been historically observed in the marketplace.

So yes, fund managers have recalibrated their books and bought some protection this week, but not to the point that signals panic. If anything, this indicates that the euphoric last six months, during which every event was given a pass, may be over.

Before jumping to conclusions, let's see if these levels hold. Remember mid-February, when we jumped to almost 100, only to fade back to a low of 80 a few days later? Nothing in the data suggests that this can't happen again.

However, fund managers don't suddenly buy costly insurance for no reason and certainly don't hold it over the weekend without a compelling reason. There must be a catalyst; needless to say, we've had quite a few this week.

First, Kashkari, a Fed member, opened the door to no rate cuts in 2024 if inflation is sticky. This is new, and even if it comes from nonvoting members, it's enough to push big players to reassess their overall market positioning.

Despite the Friday rally, fueled by yet another strong unemployment report, the devil is again in the details. Stocks rallied, but we didn't sell the hedges. We kept them going into the weekend, and this signal is a change from what we've observed throughout 2024.

At the same time, there are good reasons to keep the hedges, considering the second catalyst. Tensions in the Middle East escalated again, with Iran threatening Israel with retaliation after the attacks that killed some high-ranking officials. This was enough to propel oil above the $90 mark and accelerate the downward stock move on Thursday.

So, what's next?

Some new inflation data will be released this Wednesday, just a few hours before the latest FOMC minutes. Unless inflation becomes stickier and lends some credibility to the no-rate-cut rhetoric we've heard this week, this may be another non-event. After that, we'll closely monitor how volatility and VVIX behave.

The real risk, however, lies on the geopolitical side. Israel and Iran have been on heightened alert for months now, and despite the US trying to tighten its grip on the situation, anything could happen at any moment. This is unsettling, to say the least, and will force the market to navigate in more cautious waters.

We'll conclude by addressing a question we've received a few times on social media this week: Is it enough for us to endure volatility or stop selling it? Long-term, absolutely not. Short-term? We closed up shop on Friday to assess things a bit better. If nothing happens after the CPI release, there would be no reason to keep the shop closed.

In other news

The first quarter has ended, and some funds are already posting impressive performances. Rokos, for instance, is up a staggering 12.5%, partly thanks to its bond market bets. What was the main position? A contrarian macro view was that the seven rate cuts anticipated in January had little chance of materializing and that bond prices were too high.

This strategy paid off handsomely, as bond prices slid while rate expectations continued to shrink into the new year. Could they fall even further? It's not unlikely that the Fed will open the door to no rate cuts at all. Even more interestingly, even if a rate cut were to happen in June, wouldn't that already be priced?

We tend to avoid macro positioning, but we wouldn't be surprised to learn that Rokos maintained its bet throughout Q2 and most of 2024.

Thanks for sticking with us until the end. As always, here are a few interesting reads from last week:

This week, Capital Flows has a thought-provoking piece that reminds us that accumulating knowledge doesn't necessarily translate into the ability to make good decisions. It's a must-read if you feel like you're at the top of your game.

Why does your breakfast cost ten percent more than last year? AlphaPicks provides detailed analyses of the key commodities you consume every morning: orange juice, coffee, and cocoa. Yep, they're all on the rise.

At Sharpe Two this week, we looked at the top performers in short volatility during Q1. QQQ made the list, but SPY didn't. Read the article to find out why.

That's it for us this week. We wish you a fantastic week ahead and happy trading!

Ksander