Signal du Jour - Skew trade in GS

Is the world really on fire?

We didn’t quite hit VIX 30, but we got close enough. On Monday, as rumors spread about a hedge fund liquidating positions, the market accelerated its decline from the previous week. Realized volatility remained firmly above 30 since last Friday, only cooling off slightly yesterday—conveniently in sync with inflation data showing signs of easing.

The real question now: is this slowdown enough to put stagflation concerns to rest and potentially push the Fed toward a first rate cut before the end of Q2? Maybe. We’ll get some answers next week at the FOMC press conference.

In the meantime, on days like this, we like to ask ourselves, Is the world really on fire? Sure, uncertainty is significantly higher than it was a year ago when all we cared about was the timing of rate cuts or the outcome of the election. But this mood swing feels a bit too extreme—especially in certain corners of the market that, until proven otherwise, are still holding up just fine.

Today, we’re turning our focus to financials (again) to see how we can take advantage of the recent surge in demand for options.

Let’s dig in.

The context

Last week, we focused on the financial sector, specifically regional banks. As the market started moving lower, these banks came under scrutiny—echoing concerns from the crisis two years ago.

Over the past week, as selling pressure intensified, things only got worse for the financial sector as a whole.

JPM and GS are now down a solid 17% over the past month, while BAC has lost 14%. What’s striking is that they’re currently underperforming the regional banks index—despite being (supposedly) larger, more resilient, and structurally positioned to absorb shocks. And above all… too big to fail.

Before we go any further, let’s make one thing clear: we are not advocating a long position in financials. That’s not what we do. We’re simply laying the groundwork for our thesis on the volatility side.

Speaking of volatility—if we take a look at realized vol over the past few months, the data paints a similar picture.

GS is particularly interesting—without any major negative headlines, it has taken the lead in realized volatility among its peers, which wasn’t necessarily the case over the past year. Again, we’re not making a judgment on the stock’s quality versus its competitors—just an observation.

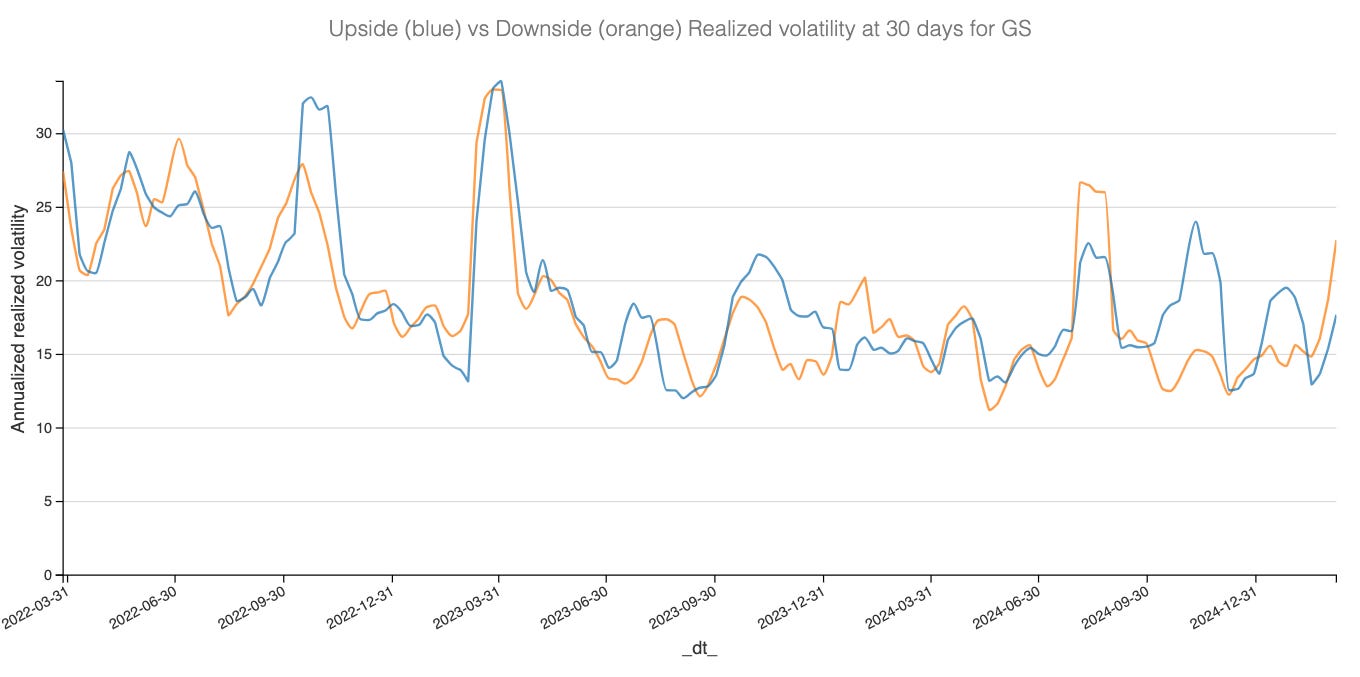

One metric we often look at (but don’t communicate much about) is the decomposition of realized volatility. By isolating positive and negative returns, we can gauge how much of the volatility comes from upside versus downside moves. Like realized vol itself, these metrics tend to mean revert and cluster. Here’s what it looks like for GS:

This perspective is useful because it helps put the degree of panic into context. While realized volatility suggests heightened activity in the stock, it would be easy to assume that sentiment is overwhelmingly driven by downside moves. But looking at downside realized volatility alone; it’s still well below what we saw during the regional bank crisis.

Another interesting takeaway: the spread between upside and downside volatility tends to be quite mean-reverting. Something for momentum and sentiment chasers to consider—but outside the scope of today’s article.

If we take a simpler view of realized volatility as a whole and project it over the next month, we get the following:

This is, of course, quite dramatic and should be taken with a grain of salt—models have a limited ability to discern when things are truly awry versus when they’re simply overdone. Right now, the forecast is heavily influenced by the extreme price action of the past week. Could the next four weeks mirror what we just experienced? Possibly, but unlikely. It would take something truly extraordinary. And despite all the Trump shenanigans, nothing on the newswire suggests we’re about to enter an even wilder regime.

Let’s see what the options market thinks and see how we could structure a trade according to our vix/skew matrix.