Signal du Jour - short vol EEM

A trade in emerging markets so close to the Fed?

It was quite the day yesterday! After a slightly hotter-than-expected CPI number, the market took a dive right after the opening. But was it really about inflation? Couldn’t it just have been someone with size making some waves in these last days of summer? What’s certain is that the SP500 looked ready for another -2% day but instead closed up 0.6%.

We can’t help but feel a bit sorry for the social media pundits urging people to go long on volatility because of factors like the economy, geopolitics, the election, the Fed, the fiscal deficit, and so on.

We feel even worse for those who follow them blindly. Going long on volatility is a tough game, and yesterday was a good reminder of why, when in doubt, you should short it. We get it: it can be scary at times and we’ve actually missed most of yesterday moves - who’s caught in the light like a baby rein deer now - yet if you don’t bet your house, it pays off over time.

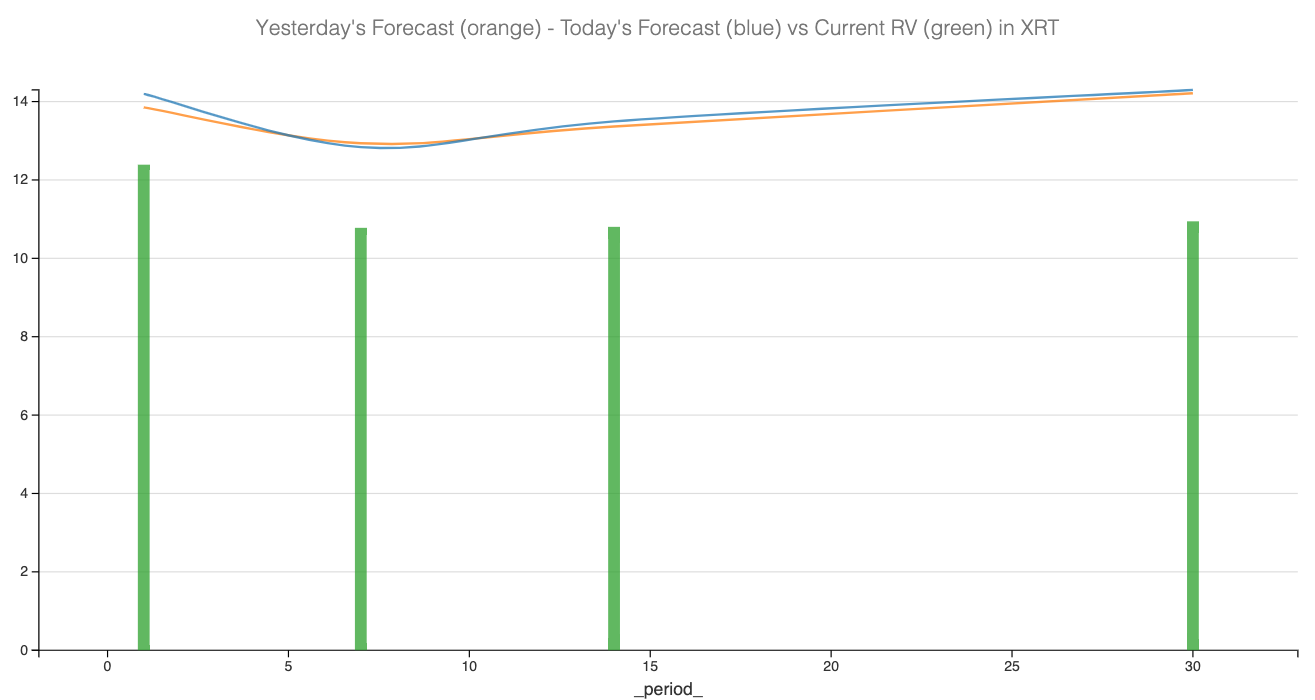

Meanwhile, we exited the short straddle in XRT we talked about last week right at the close. We're still holding on to the short vol in VXX from two weeks ago, but it might be time to cut it loose. Hopefully, we can manage a scratch between today and tomorrow.

Today, we're looking at an opportunity in EEM, the ETF that offers exposure to emerging markets. We’ve had quite a few signals in China and Brazil; all of these are available through our API and in our computations. Get in touch if you want access!

The context

We’ve written a few times about EEM, and every time, we get the same reaction from our (new) readers: "Stocks from emerging markets? I wouldn’t touch them with a ten-foot pole."

Well, "emerging" is just a label. A quick glance at its largest holdings reveals some well-established Korean and Indian conglomerates.

From a performance perspective, EEM is lagging behind SPY so far, but it’s still posting a solid return of +7%. Even with a 10% drop since the early July highs, the volatility over the summer didn't surge to unprecedented levels.

Currently sitting at 11%, volatility is expected to bounce back to a more typical range based on what we’ve observed over the past year. We’re looking at a forecast of around 13% within the next two weeks, and slightly over 14% over the next 30 days.

So, is this a reason to go long on volatility? Probably not. However, we can use our forecast to refine the insights we’ve gathered from the options market. Let’s take a closer look.

The data and the trade methodology

Let’s start by examining the variance risk premium (VRP) in EEM by comparing the implied volatility at 30 days to the realized volatility we just discussed.