Forward Note - 2025/05/25

The vigilantes bark and volatility yawns.

When thinking about what lies ahead in the coming weeks and months, two camps are taking shape.

There are those convinced we are on the verge of a generational backdrop—arguing that every proper bear market has its share of face-ripping rallies. And then there are those who are either convinced (or busy convincing themselves) that everything is just fine.

We’re watching both camps with curiosity. Because if spring 2025 taught us anything—anything—it’s this: nobody knows. Not even the ones with a lot of nose. This week offered a gentle reminder.

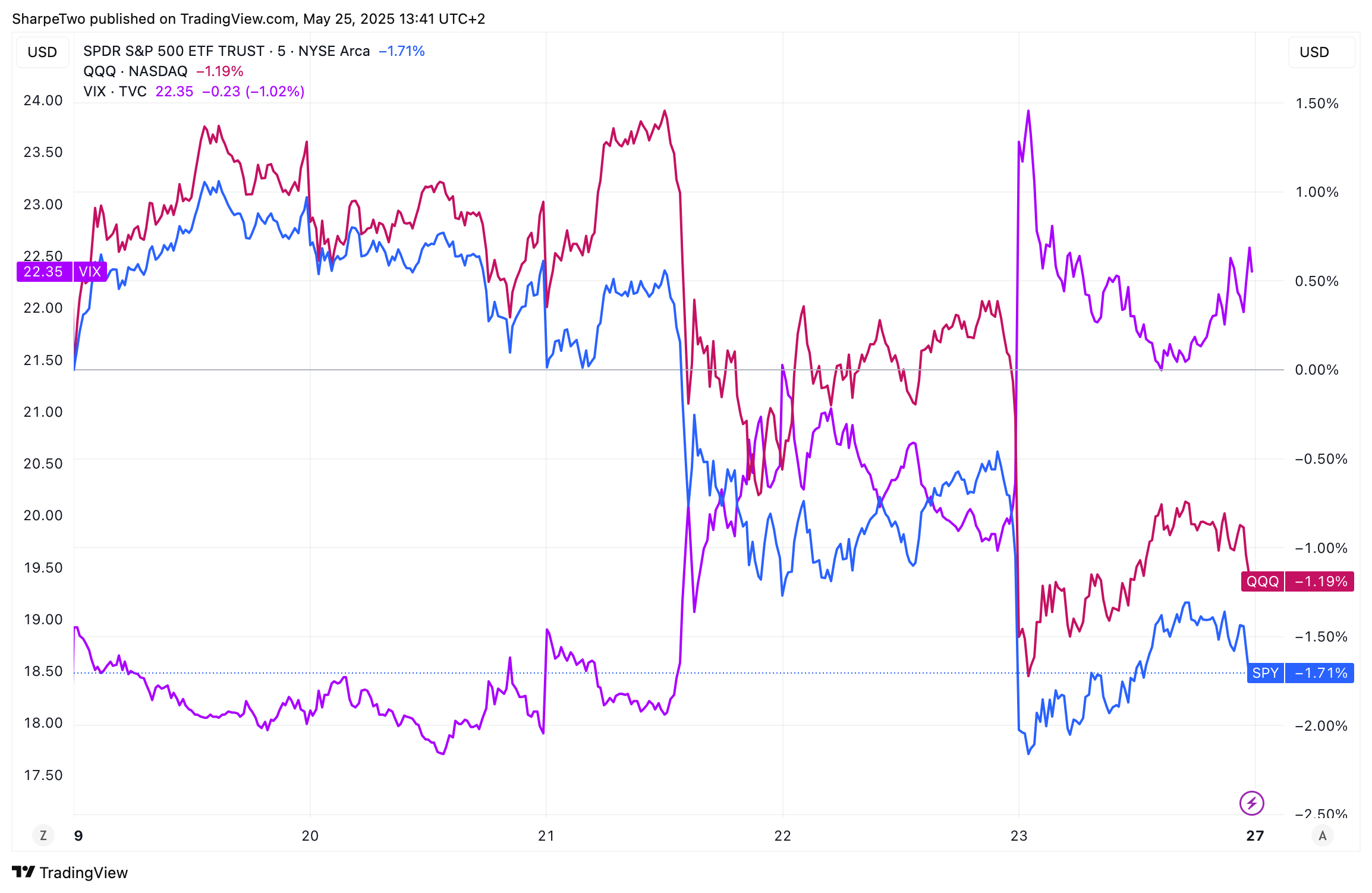

Some numbers: the S&P 500 dropped just over 1.5%, and the Nasdaq gave back about 1%. But it could have been worse. Much worse.

Friday, before the open, we learned President Trump had floated the idea—on brand, via tweet—of 50% tariffs on Europe. No follow-up, no details, just enough to send VIX spiking back above 25 in pre-market and throw a chill through anyone hoping for a quiet Memorial Day weekend.

The end of the story? Oh come on—you really did not see it coming?

Of course you did. When faced with a choice between sacrificing their long weekend to price in a new presidential threat or just chilling, the market did what it does best: shrugged. VIX melted all the way back down to 21. And while we did close the week above the 22 handle, the reaction was nothing compared to the kind of spasms we saw after each new headline in March or April.

Some will be quick to point out we’re still three points higher in vol on the week. If you ask us, that’s just the pendulum swinging back from the burst of early-May optimism—when markets cheered the China truce and started imagining trade deals blooming left, right, and center.

But we are inching closer to the 90-day pause deadline. Europe has been warned. Japan and India, meanwhile, have dared to sing some slightly dissonant tunes about how close they are to striking deals with the U.S.

Nothing burgers for now—but for how long? We certainly do not know.

The other “major” market mover this week? The BBB budget—narrowly passed, giving the President the green light to push his agenda forward. This time, the market raised not one eyebrow, but two. It is not every day you see 30-year U.S. bonds trading above 5%.

Yet here we are. And with that, a fresh wave of warnings from the bond vigilantes that this is it—the big one. Maybe it is because we started our careers barely two months before America’s first credit downgrade, or maybe because we were trading European debt during the sovereign crisis—but honestly? We are having trouble getting worked up about it.

Let us put it this way: the market kept lending money to Argentina for years, and through more than a few haircuts. Are we really supposed to believe it will stop lending to a country still (arguably) at the forefront of global innovation, with an economy that makes up nearly a quarter of global GDP?

We have our doubts. Especially when the “credible alternatives” are… what exactly? France? Germany? Italy, maybe? All of that to say: while we acknowledge the risks looming, it is hard to sink into another round of negativity.

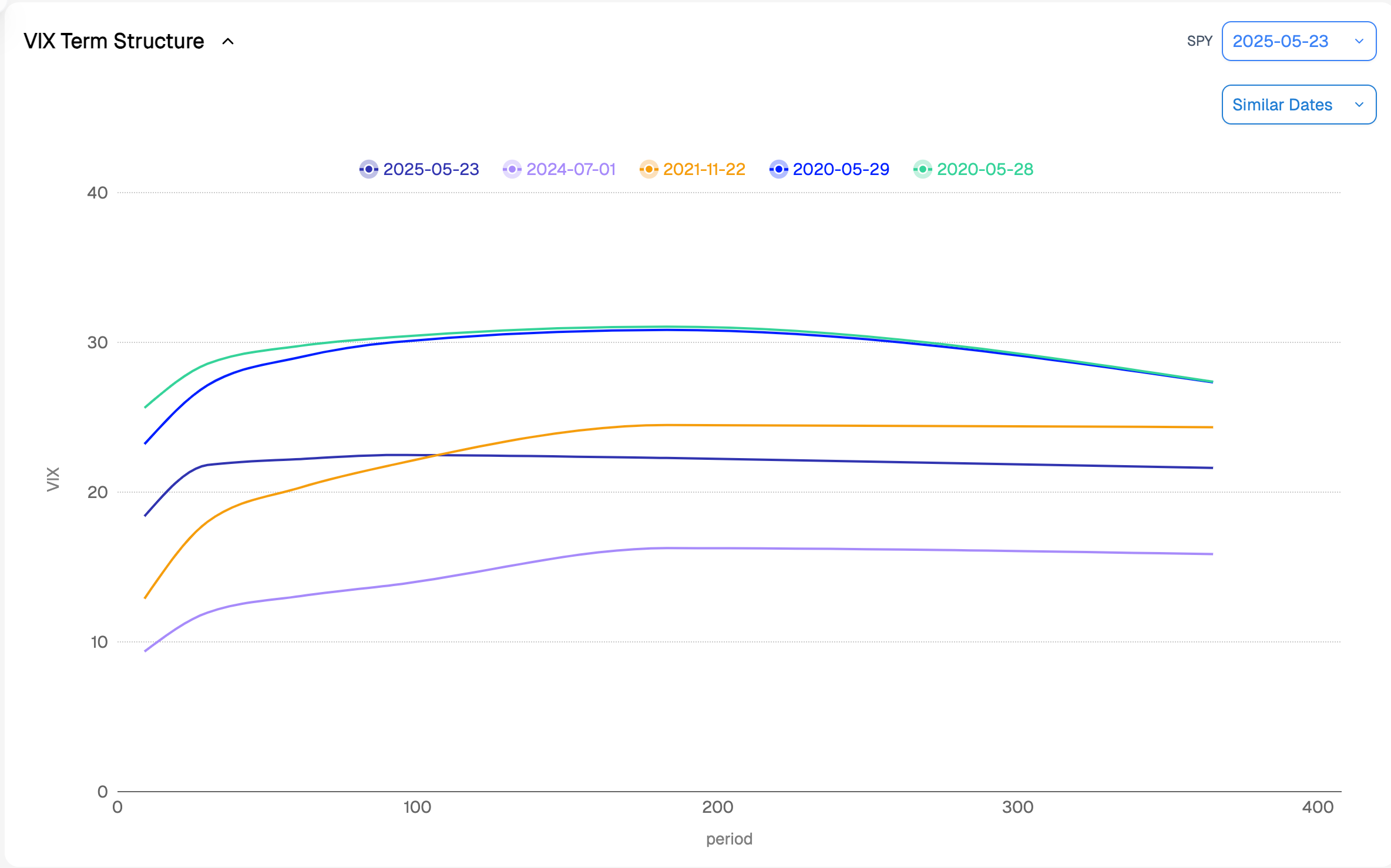

Let us bring in some hard data—and, as usual, start with the good old term structure. Despite all the gloom mushrooming across the newswires this week, last week’s contango held up.

We agree—it is not the most convincing shape. But if you squint, the current volatility setup looks eerily similar to the calm of May 2020, post-COVID. Back then, volatility had not vanished—but the worst was probably behind us. (Until the next crisis, of course—whether months or years later, depending on your lens.) That is roughly how we are seeing things now.

Another look at the term structure:

Yes, the contango last week was likely too steep. But even after some digestion, the curve closed in a similar shape to late April—and still a far cry from the flat, exhausted structure we saw through March and parts of February. This, despite a laundry list of reasons for traders to load up on short-dated protection.

Let us be precise—VIX at 22 is not high. It can go much higher, as we have seen recently. But for that to happen, we would likely need to revisit the flatness we saw earlier this year, where the spread between VIX and VIX3M was barely a point—for weeks. Think of that setup as the antechamber of real risk.

Sure, we could always get another spike to 30. But judging by how quickly Friday’s move was digested, it gives you a sense of just how disruptive the next headline will need to be to take us from slight contango to full-blown backwardation.

One more tactical sign: SPY puts were not cheap into Friday’s close.

The right time to load up on those was about ten days ago. Now? We are much closer to neutral. Vol is not screamingly cheap, and puts are priced slightly above calls—but nothing extreme.

So what do you do with all this?

As we mentioned last week, we are slowly but surely dipping back into risk reversals. The risk is obvious—especially if you do not delta hedge: one bad headline and the put side can bury you fast. But with a term structure still in mild contango, vol levels that do not beg to be bought, and puts no longer a bargain, the environment is gradually becoming more supportive for those kinds of trades.

If you want a one-line narrative: you are betting on the resilience of a market that—annoying as it was—remarkably absorbed the April shock. And short-term ripples are unlikely to truly test that resilience. If you want an even simpler one: equities go up. That has been the story for decades. And if April reminded us of anything, it is exactly that.

In other news

And it is another all-time high for Bitcoin.

Quietly but surely, the digital currency rallied from the low 80s to tack on a stunning 40% in just a few weeks. The rationale? Hard to say. Maximalists were quick to point out that its performance closely tracked gold—and that it is increasingly behaving like a serious diversifier against the U.S. dollar and Treasuries (sic).

More measured analysts noted it has simply moved alongside equities, as investors pile back into risk now that a world of day-to-day tariff pivots is just part of the playbook. It also helps that ETFs now allow fund managers to allocate capital into crypto with far less operational headache.

We smiled this week when someone remarked that Bitcoin is now “more valuable” than MSFT. That sentence alone says plenty: just how small this asset class still is, and how far it has to go before becoming more than a shiny digital playground.

It also raises the real question—if you think 110k is expensive, ask yourself: three years from now, what is more “valuable”—the entire Mag7 or Bitcoin?

Thank you for staying with us until the end, as usual, here are two good read from last week

An exhaustive, sharp breakdown of how Google’s AI blitz can’t save its decaying search monopoly. Despite flashy demos and Gemini 2.5’s capabilities, the business model that made Alphabet a $2T juggernaut is in structural decline. A must-read for anyone betting on BigTech resilience—or shorting it.

A packed breakdown of why semiconductor stocks ripped in May—despite headwinds. From Computex 2025 to NVLink Fusion, Nvidia is widening its moat and locking in Middle East demand with AI megadeals. The piece lays out why sovereign AI, not just U.S. hyperscalers, might drive the next leg higher—and why AMD is not out of the race just yet.

That is it for us this week, we wish you a happy long weekend and a good (NVDA earnings) week ahead.

Happy trading.

Ksander

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.