Another week under the chopping machine.

Equity markets shed about 2% last week despite a shortened trading schedule due to Thursday’s state funeral for President Carter. Most of the losses came on Friday, following yet another blockbuster employment report. Yes, you read that correctly—despite the US economy adding 256k jobs in December, the market tumbled 1.6%. While the VIX didn’t quite manage to close above 20, is the “good news is bad news” mantra making a comeback?

Let’s try to bring some nuance to this. The strength of the US economy is precisely why these sell-offs feel so orderly. If we stick to the data, it’s clear that the market is currently unwilling to overpay for hedges, recognizing that the likelihood of a rapid acceleration in the downturn remains relatively low. This makes life tougher for insurance sellers, but if you’ve been struggling on the short side of volatility lately, consider the plight of California’s insurers and homeowners. They’re exposed to max gamma, grappling with margin calls, and dealing with the human cost of natural disasters.

A sobering perspective, to say the least.

So why are things heading south? It’s not a case of "good news is bad news" but rather the inflation narrative making a comeback. On Friday, the market dipped about 1% following the jobs report, but the decline felt “manageable”—stay away when volatility is climbing, and you’d likely be fine.

The real acceleration came later, after the University of Michigan, better known for its consumer confidence index, dropped below the 74 threshold expected by the economists. However, their lesser-known inflation indicator, the consumer inflation expectation, stole the show, coming in at 3.3% instead of 2.8%.

We usually refrain from overanalyzing such numbers … but not this time. If I bombard you with messages insisting it’s going to be freezing tomorrow, what will your expectation of the temperature be? Unless you’re a troll, a super-smart scientist, or lucky enough to have escaped the northern hemisphere’s chill for something warmer, your expectation will probably lean toward "cold." But does your opinion truly have predictive power? And by truly, we mean really?

Yes, 3.3% is higher than 2.8%, but let’s not get carried away. The actual inflation pain threshold for households is well above 4.2%. In simpler terms: households expect prices to rise (duh …), but they’re not forecasting anything close to the chaos of 2022.

We rest our case.

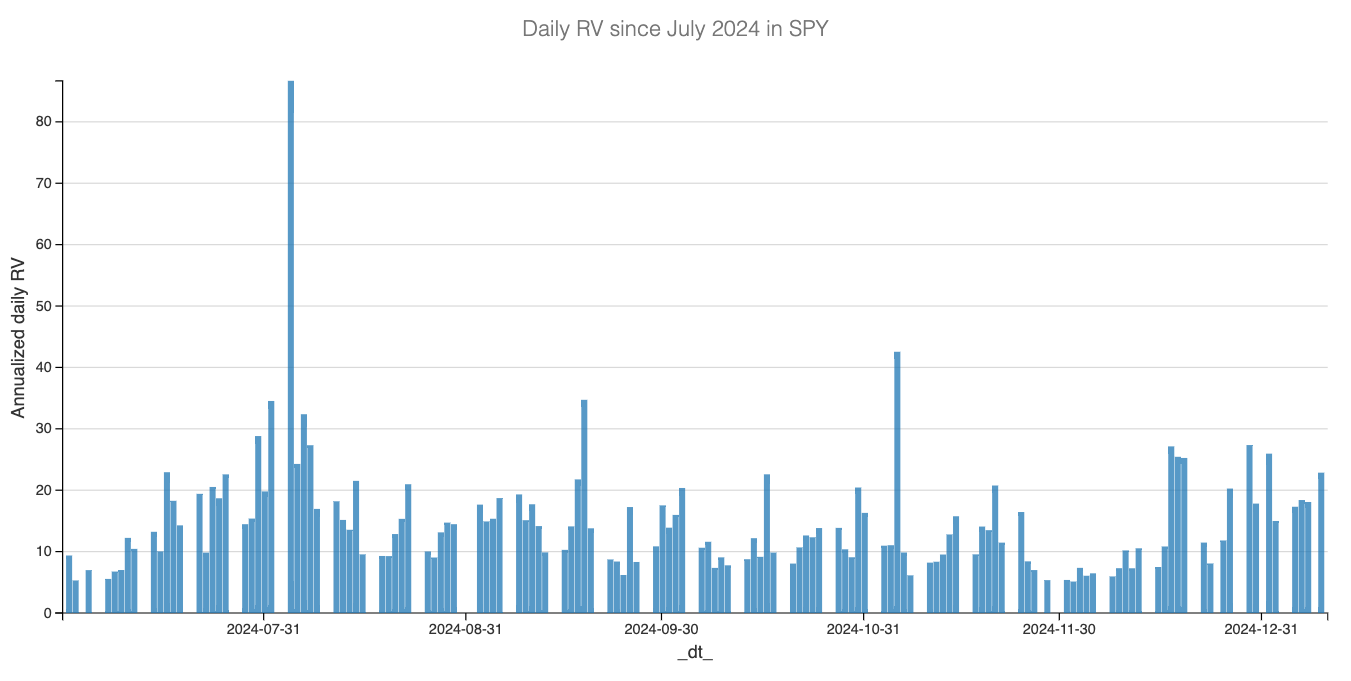

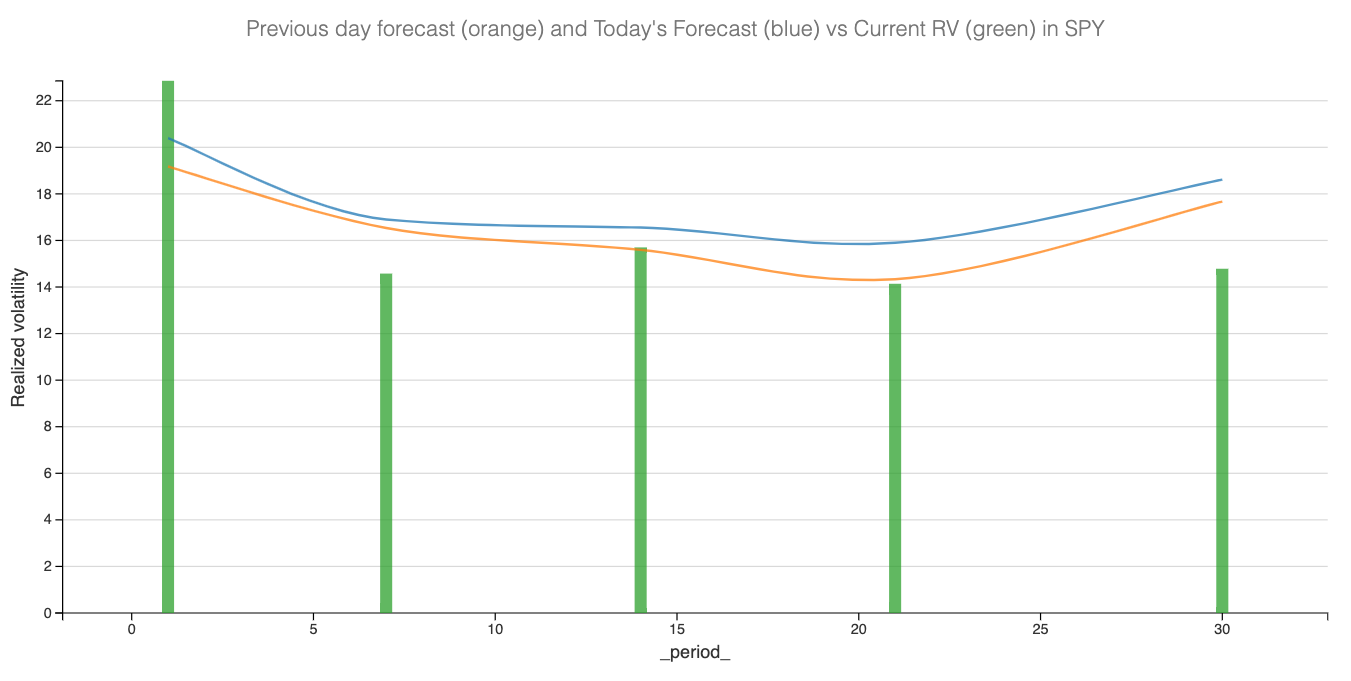

Great—so what do you do with all of this? Last week, we mentioned that at VIX 16, the variance risk premium in US equities wasn’t worth the trade. But at VIX 20, things start to look more compelling. We still anticipate realized volatility to hover around 18 over the next 30 days, but we’re now sitting at the higher end of the range observed over the past six months.

And let’s set aside the math for a moment: VIX 20 to 22 offers a pretty attractive entry point for selling volatility—provided we remain in that neutral volatility regime. Of course, keeping an eye on the news is essential to ensure nothing is spiraling out of control: Trump isn’t even back in office yet and is already threatening Denmark if they don’t sell Greenland.

But we’re traders. Our job is to assess risk and, when conditions allow, take a nibble at it. At these levels, dipping a toe into the water starts to feel interesting.

We also mentioned that after the December FOMC spike, it was time to acknowledge a shift in the market. The volatility of volatility has entered a new regime—it’s elevated, and seems comfortable staying there. This calls for a different approach.

We’ve received many messages about the calendar spreads and diagonals discussed in last week's Forward Note. We appreciate the feedback and questions, so please keep them coming. However, let’s clarify something important: a structure alone rarely provides an edge. Consistent profitability comes from selling something expensive and offsetting it with something cheap—or at least cheaper than what you sold, and ideally a very different risk profile.

Let’s break down what we plan to do over the next few months. Suppose you sell an ATM straddle with 21 days to expiration because it is overpriced. Traditional volatility trading suggests holding that straddle until expiration to maximize the profit from vega and the subsequent theta decay. We propose a shift: exit that front straddle much earlier—sacrificing some of the vega and theta exposure—to limit your short gamma exposure drastically. If volatility of volatility is high, that may be a sensible risk management rule to enforce anyway.

Then, use the proceeds to purchase a 5-delta structure, ideally underpriced but more likely fairly priced, with over 45 dte. These longer-dated options often attract ill-informed traders looking to "collect premium on stuff they would like to own".

Then rinse and repeat.

You won’t generate consistent profits like you would by systematically selling volatility—although, if you manage your book like an insurance seller, you can reinvest only a portion of the proceeds. After all, you are the manager of your trading, and how you allocate is up to you. That said, a sudden big move—whether up or down—can yield a nice payday.

To be clear, we are not suggesting a complete overhaul of your book or trading style, nor are we advocating joining the dark long side of the force. However, a bit of diversification in your strategies can provide a useful hedge and offer flexibility when conditions change.

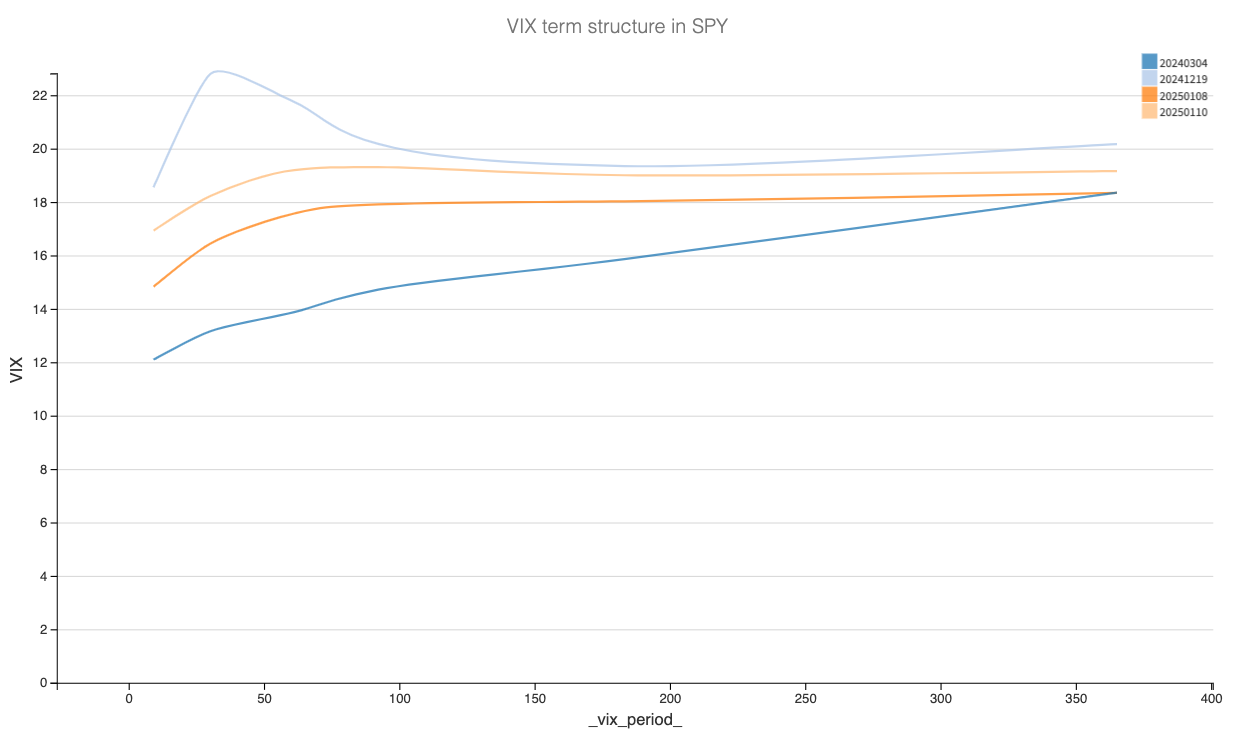

The truth is, nobody knows what 2025 holds. We reviewed the VIX term structure over the past four months, and while there was a brief improvement after the US election, it has remained stubbornly flat, oscillating between very slight contango or very slight backwardation. This signals something important: the market is anticipating a catalyst and is poised to react when it arrives.

Notice your own cognitive bias here—our analysis didn’t imply something terrible, yet that might have been your first thought. It’s natural to focus on risk, but remember: the burden of proof lies on the sellers. And do you really want to bet against an economy that added 256k jobs in December, especially with a president widely expected to support American business over the next four years?

We understand that fund managers might consider taking profits and parking capital for a comfy 5% yield after two exceptional years. However, it’s hard to imagine the buying flow evaporating entirely.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In other news

What’s happening in China? Nobody truly knows, but the bond market is experiencing a bit of a rout alongside the currency. The market appears to expect more stimulus for the economy. And if it weren’t China—with its mighty government—we might even dare to say that the markets are demanding it.

Will it get that stimulus? Once again, predicting the actions of Chinese policymakers is an exercise in futility. What’s more striking is that despite two attempts to stimulate the economy, in September and December, they’ve failed to deliver meaningful results. This raises an even bigger question: Can they do more, or are they grappling with the sheer complexity of administering an economy this vast?

As powerful as the government might be, it seems they can’t even compel billions of people to spend—or prevent a foreign leader with a penchant for disruption from rekindling a trade war.

Thank you for staying with us until the end. As usual, here are two highly engaging reads from last week:

- has published a detailed and thought-provoking piece about buying tails in MSTR. We’ve previously described this company as white-collar crime in plain sight. Now, we might actually put our money where our mouth is and follow him on that trade.

- We discussed a trade on ARGT earlier this week, and while a reader pointed out some poorly explained figures (fair enough), the broader narrative remains unchanged—Milei is proving many of his critics wrong. For some, that truth is difficult to accept.

That’s it from us this week. Wishing you a calm (not too hot) CPI week and, as always, happy trading.

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.