Another rollercoaster week, and here we are, just shy of new all-time highs.

How is that possible? Weren’t we on the brink of a freefall last week after yet another mixed employment report? Panic is a favorite word on the market, but it doesn't always show up.

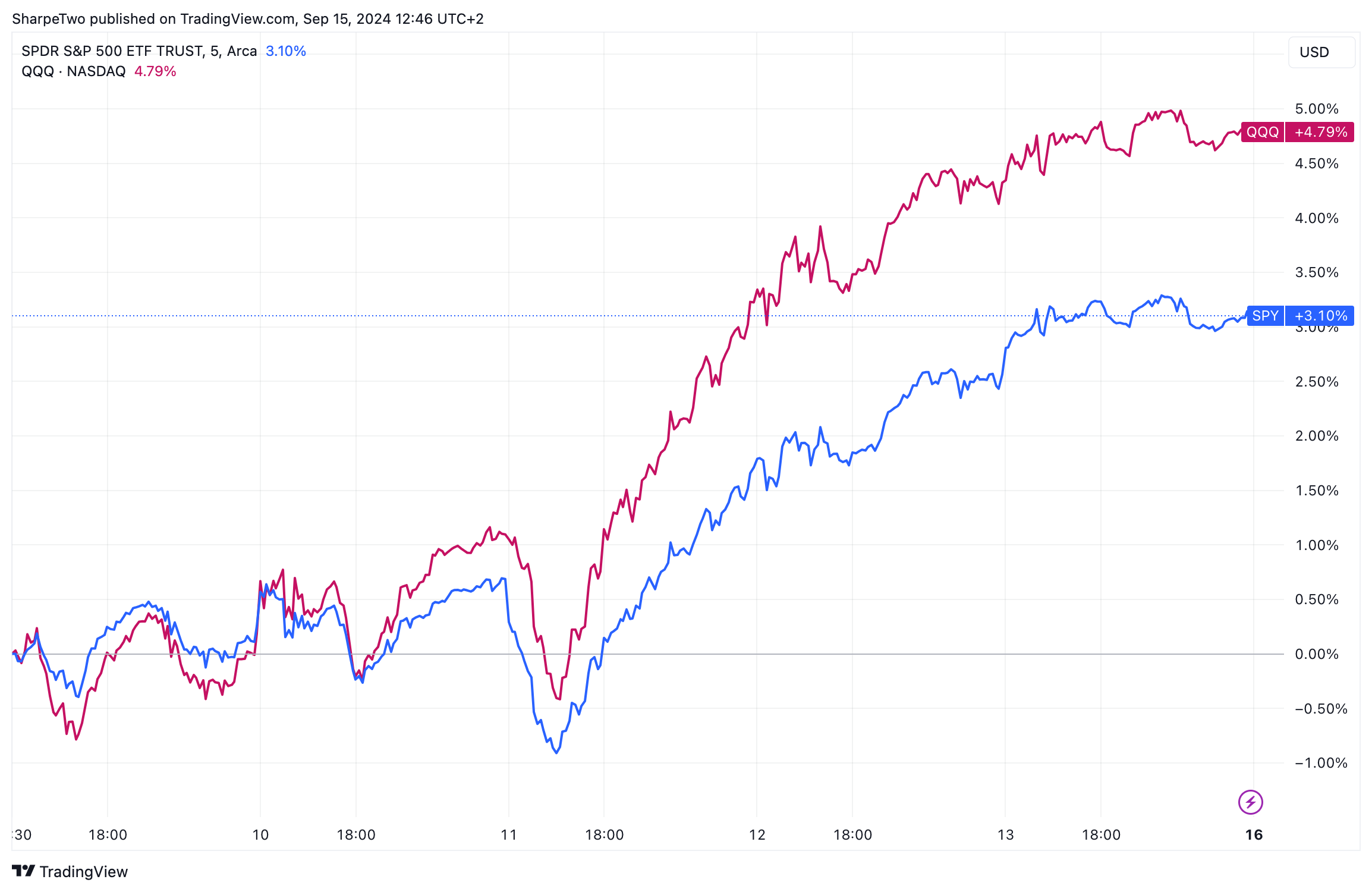

Instead, the major indices reversed most of the losses from the week prior, with the S&P 500 adding 3.93% and the Nasdaq up 5.77%—one of the best weeks on record this year. The VIX closed below 17 for the first time in September.

It wasn’t all that straightforward, though. After some unexpectedly “hot” CPI data, coming in at 0.3% instead of the expected 0.2% (can we please stop talking about inflation?), the market hit an air pocket, dropping nearly 100 points in the S&P 500 in less than an hour.

At that moment, things were looking rough, and the stakes for a bumpier September than August seemed to be rising. Yet, there was barely time to take a break, and … it was all gone. The market closed the day well in the green, and it was smooth sailing until Friday.

What drives the marketplace crazier than an unexpected crash? An expected crash that never happens.

If you’ve been a reader of Sharpe Two, you know that directional bets aren’t really our style. Still, it’s hard to ignore such strong reversals despite all the macro, gamma, and social commentary circulating online. It could be just a relief rally after a tough two months, and the volatility could start up again next week with the Fed’s rate cut announcement and the accelerating U.S. election cycle.

Yet.

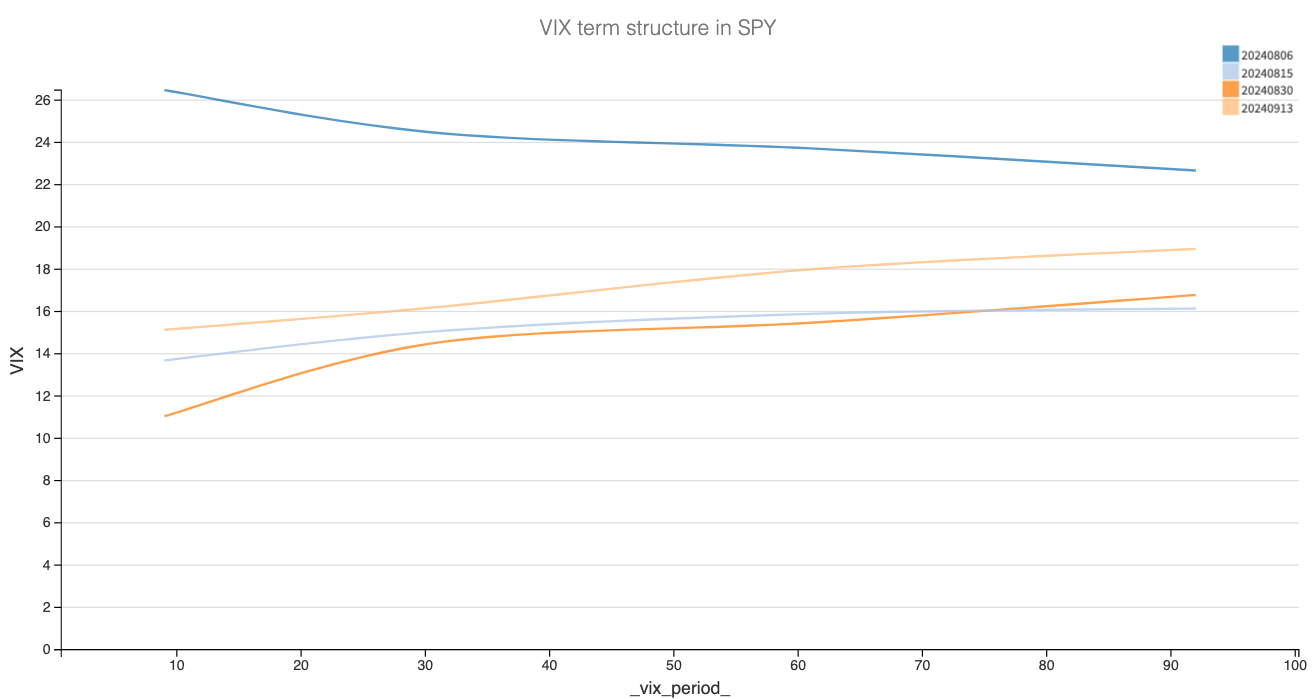

VIX at 16.56 tells a different story. And while the VIX alone can be a misleading indicator, the VIX term structure isn’t showing much tension right now.

Sure, we’re still slightly elevated and a bit flat, but this doesn’t compare to the high-stress period we experienced in August. While emotions are still running high and the memory of VIX 65 is fresh in everyone’s mind, the market has… somewhat moved on.

Bear with us—we’re not saying there’s no risk in the market. But anyone betting on long volatility here, expecting an imminent crash, is going against the most widely accepted outcome currently priced in: some moderate agitation but nothing too serious on the horizon.

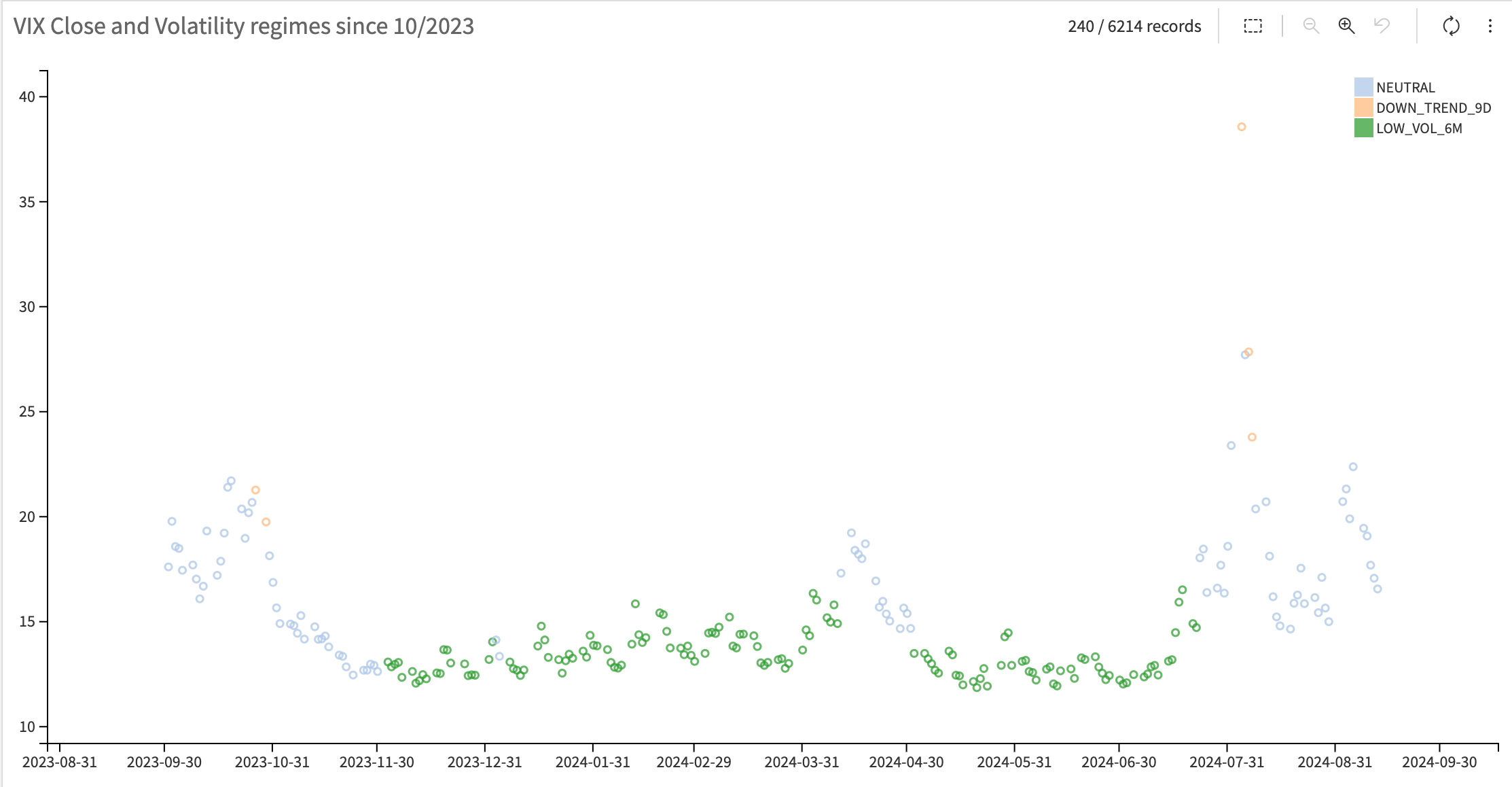

Could we see VIX back at 22? Absolutely—last week proved it could happen in just half an hour. However, it also confirmed that we’re solidly in a neutral volatility regime: the burden of proof is on the risk side and realized volatility, and the market isn’t willing to pay a high premium for long.

Market participants love streaks and stats, so here’s one for you: Since last Friday, despite all the post-NFP jitters and concerns over the size of the upcoming rate cut—considering a recession might be around the corner—the VIX hasn't closed above its previous close. That's hardly a market shouting about tensions, nightmares, and fears.

So, as written in our Note from the beginning of the month, this is the harvest season for volatility sellers. Unless something drastic changes, swings in implied volatility should be carefully assessed and likely shorted to capture the premium over realized volatility.

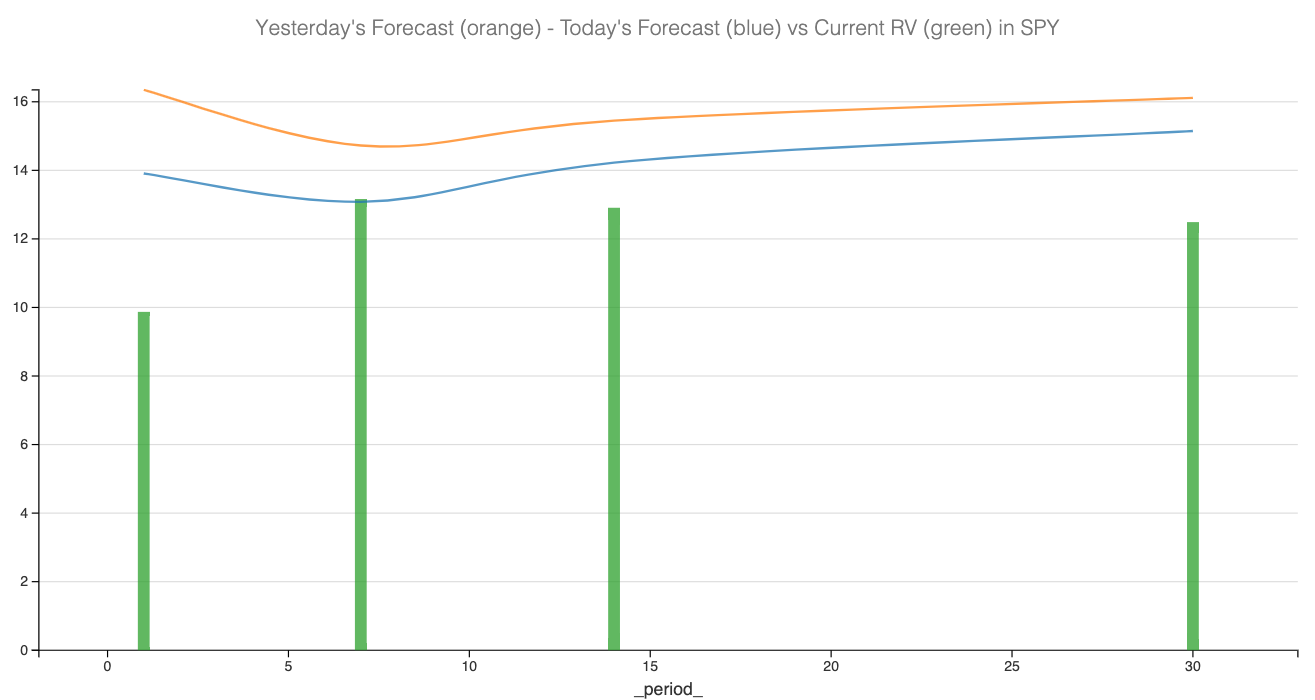

Carefully, because selling too low will obviously hurt—remember, we’re in a neutral regime. For example, VIX at 16.56 might not be the best sell right now, given our forecast for realized volatility over the next 30 days is somewhere between 15 and 16.

It may be best to wait for the next phase of agitation to find great prices, and we are in luck considering that the FOMC is on the same week as the quarterly expiration.

In conclusion - don’t rush to sell volatility early in the week it’s not expensive yet. Don’t buy it either: it’s definitely not cheap.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In other news

Gary Stevenson—does that name ring a bell? We came across him in a YouTube documentary where he claimed to be the most profitable trader at Citi during 2011. We watched it with a mix of amusement and nostalgia. Thirteen years ago, the author of this newsletter was also active in STIRs, though not with the same grandiose success Gary claims. However, it turns out that success might not be as glorious as he suggests. FTAV recently interviewed former colleagues and people mentioned in his best-selling book, The Card Game. While some stories are accurate—like how he got recruited by the bank despite the recruitment team stacking the deck against him—he was certainly not the best of the best.

This reminds us of a quote from an old (and very successful) boss: "Success is like jam; the less you have, the more you need to spread it around."

Thank you for staying with us until the end. Here are a few interesting reads from last week:

- If Gary's misadventures put a smile on our faces, the ones involving Raphael Bostic didn’t. While no apparent conflict of interest has been flagged (yet), the fact that a Fed member can still talk to the marketplace, vote at the FOMC, and trade is beyond us.

- This week, Donald Trump and Kamala Harris debated, and while the mood in the Republican camp has certainly darkened after Trump's performance, we’ll leave you with some music and (hopefully) a lighter mood to start the week.

That is it for us - we wish you a great week ahead, and happy trading.

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.