What to Make of This Summer?

As September rolls in after Labor Day, that’s likely the question on the minds of many traders—whether they’re professionals or retail investors.

On one hand, the macroeconomic picture hasn’t shifted dramatically. A rate cut at the next FOMC meeting on September 18th seems almost certain. GDP growth year-over-year is at 3%, slightly above the 2.8% economists predicted, and the previous quarter’s numbers have been revised upward. The unemployment rate has ticked up to 4.3%, but it still sits near historical lows.

On the other hand, equity performance over the summer has been a mixed bag. The SP500 added another 3%, but the Nasdaq slipped by about 1%. Meanwhile, the Russell 2000 saw a nearly 10% jump.

What a contrast to H1, when the Nasdaq was up 19%, closely followed by the SP500 at 15%, while the Russell lagged behind with just a 0.5% gain. We touched on this back in July, noting the start of a potential rotation: it’s getting harder to ignore now.

Here’s the market thesis: small and mid-caps are hit first by restrictive financial conditions. They simply don’t have the cash reserves or access to credit lines that blue chips do, and a 5.25% rate is prohibitive in the long run.

So, if we’re entering a new rate cut cycle, their financial outlook should improve, and they should rise. Yet, we find ourselves puzzling over this question:

Isn’t a rate cut supposed to be good for all stocks, prompting investors to buy across the board? After all, if it's beneficial for the weaker players, shouldn’t it also boost the stronger ones? But the past few days have painted a different picture: the SP500 has struggled to hit new all-time highs despite multiple attempts and plenty of reasons to do so (a 3% GDP figure on Thursday is no small achievement). Even with end-of-month flows on Friday just before the close, no one dared to venture into uncharted territory.

This might be more macro commentary than we usually dive into, but it’s a necessary foundation for what we really care about—what's the current volatility regime?

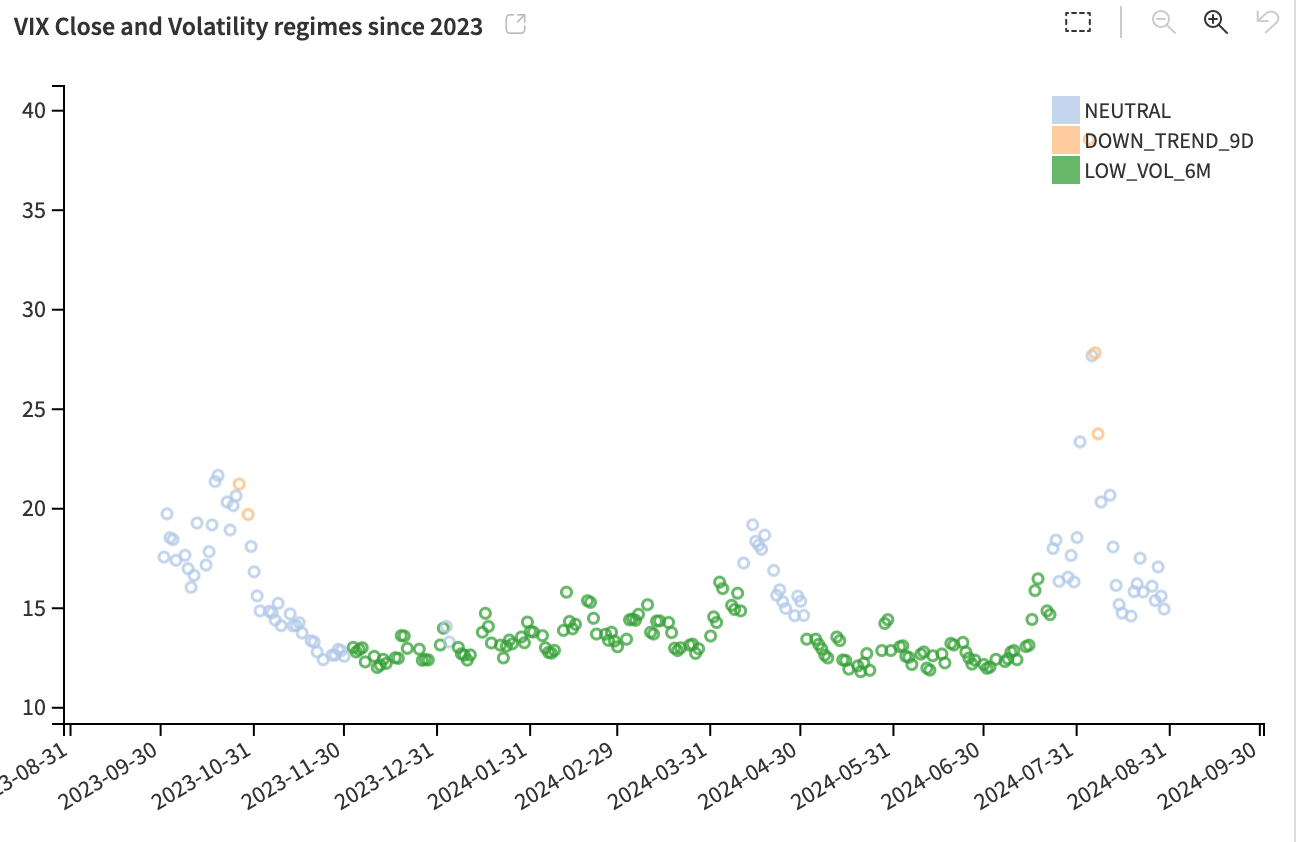

If you were just glancing at the VIX on Friday, you might think, “15.00? Nothing to worry about. Call us back when we’re above 16.” And a part of us does feel that way.

But from a data standpoint, the market regime is still neutral.

What's clear from this chart is that things feel a bit different now compared to Q4 2023 and H1 2024. Back then, we’d easily crush 15 and settle comfortably around 12 without a second thought. Not anymore. This could be nothing more than a byproduct of the huge spike earlier this month—many traders might just be rattled, thinking twice before selling at 15.

But we can’t shake the feeling: isn’t this precisely a feature of a new regime that we’ve entered this summer? A regime where rates may be going down, where the market's focus has shifted from inflation to recession? A regime where blue chips and tech stocks don’t soar as easily (like NVDA dropping despite its monster earnings)? A regime where VIX at 15 is the new 12, and the breaths of implied volatility are deeper than before?

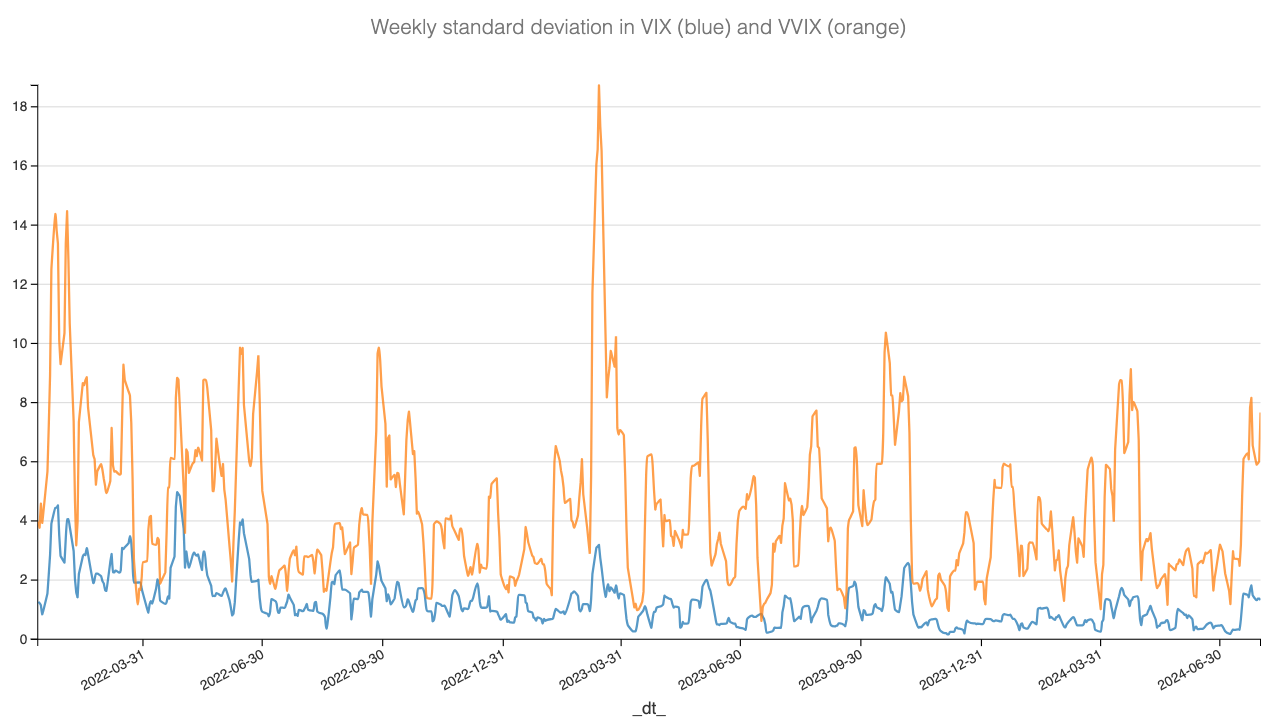

Let’s break it down—look at the standard deviation of the VIX and VVIX over the past nine months.

Notice how we went from virtually zero to almost 2 in the VIX, and now we're consistently above 6 in the VVIX? All it took was raising the threshold from 12 to 15.

To survive in the market, you have to repeat the same process over and over, yet adapt—changing slightly each day. That’s how you end up doing something very different from just six months ago. Those who don’t adjust to the fact that the VIX can now swing 1 or 2 points in a couple of sessions before giving them back over the next 2 or 3 days, just because it wasn't like this before, will miss out on many opportunities—or take unnecessary hits.

Let’s wrap up with this: a regime where volatility breathes but invariably returns to its mean is exactly what we want as volatility sellers. There's risk, sure, but nothing too extreme. It may feel unsettling at times, but generally, carrying that risk pays off quite well.

Enjoy it while it lasts.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In other news

NVDA did it again. Its revenue is now approaching $100 billion a year, out of which it pockets a staggering $53 billion as pure profit. Frankly, there are hardly any words left to describe how extraordinary these numbers are. Yet, the stock was down this week, dropping nearly 10% immediately after their earnings on Thursday before clawing back some of those losses. A quick scroll through social media reveals a range of wild theories, with some even suggesting fraud in their accounts.

Maybe. Who knows? But why would Nancy keep buying calls?

A more reasonable explanation is that while their revenue doubled, it's still lower than the 2.6x growth it posted last time. This might signal that the incredible acceleration is beginning to slow down. Time for new investors to hop on board while others take their profits and exit the rocket ship.

Just the normal life of a publicly traded company, if you ask us.

Thanks for sticking with us until the end! As always, here are a few smart reads from last week:

- The Efficient Market Hypothesis — One of the most debated concepts in finance. Some strongly disagree with it and have made fortunes by betting against it (yes, Charlie, George, and Ken, we’re looking at you). Meanwhile, others have also made fortunes embracing it (hello, BlackRock and all the ETF sellers out there). So, when we came across an interview with Eugene Fama in the Financial Times, we couldn’t help but devour every word.

- Not an article, but a research paper that caught our eye: Retail Market Makers Can Post Up to a Sharpe Ratio of 17 Thanks to Uninformed Retail Flows—and they’re not even paying for it! If retail money is this clueless about the market, is the market really efficient? Sorry, we couldn't resist. We'll see ourselves out.

Thank you for your support it isn’t lost on us. We wish you a great week ahead and happy trading.

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.