Forward Note - 2024/03/10

The seatbelt sign is on, go back to your seat.

The equity market took a breather this week, failing to reach new all-time highs, while the VIX closed above 14 for the second time in a month. Friday's job report came in much stronger than expected, underscoring the economy's resilience again. However, the positive news wasn't enough to lift the market's overall performance: the Nasdaq closed 1.5% lower, while the S&P 500 limited its losses to 0.25%.

This week's other big event was Jay Powell's semi-annual testimony. On Wednesday, he reaffirmed the Fed's dual commitment to Congress—aggressively tackling inflation while ensuring that Americans have access to stable, long-term employment.

Although he didn't provide a specific timeline, Powell reiterated that it will be appropriate to adjust the monetary policy at some point this year. Except for one of the most awkward moments we've had to witness since following the financial news, the same message was delivered to the Senate the next day and was well-received by the market.

So, why the sudden reversal on Friday? Once again, it was NVDA.

The stock plummeted nearly 10% within hours, going from flirting with the $1,000 per share mark to well below $900. Despite some late-hour buying that lifted it from its lows, things didn't look so hot for the Wall Street darling, and the resemblance of a black Friday was quick to resurface. Given the size of its market cap, NVDA dragged the major indices, SPY and QQQ, down with it.

No major news triggered this decline, and it's plausible that some funds were simply selling to cash out on their substantial profits—it is a market, after all. Undoubtedly, many investors have been riding this wave for quite some time and may have decided that they are content with their gains. The stock still ended the week up 4%, and despite the flurry of articles suggesting the bubble had burst, we wouldn't recommend looking further into this matter until something significant surfaces about the company itself or the overall semiconductor sector. However, it is a sign of caution.

What really caught our attention, though, was VVIX. As a reminder, VVIX is the equivalent of the VIX for the VIX. It provides insight into the supply and demand dynamics within the VIX options complex, looking 30 days ahead. After weeks of nothingness, we witnessed a significant upward move throughout Friday’s session. What does this mean? It is the first concrete indication that fund managers were buying VIX options en masse.

A side note: yes, you can always monitor more advanced and complex metrics, such as the steepness of the skew, to track fund managers' activity. However, if you need to dive this deeply to stay on their trail, it likely suggests there was little substantial activity to begin with. As we say in France—trading signals are like jam: the less you have, the more you need to spread them around.

Does this mean we are entering a new regime? It's a start—VVIX actually had two moves of more than 5% this week. Such 5% moves are rare enough to be noteworthy, immediately placing them in the 90th percentile.

However, let's temper our excitement. With VIX at 14.74 and VVIX at 86.5, we are still far from the long-term averages observed in this product, and our regimes remain firmly anchored in the low volatility environment we've experienced for months.

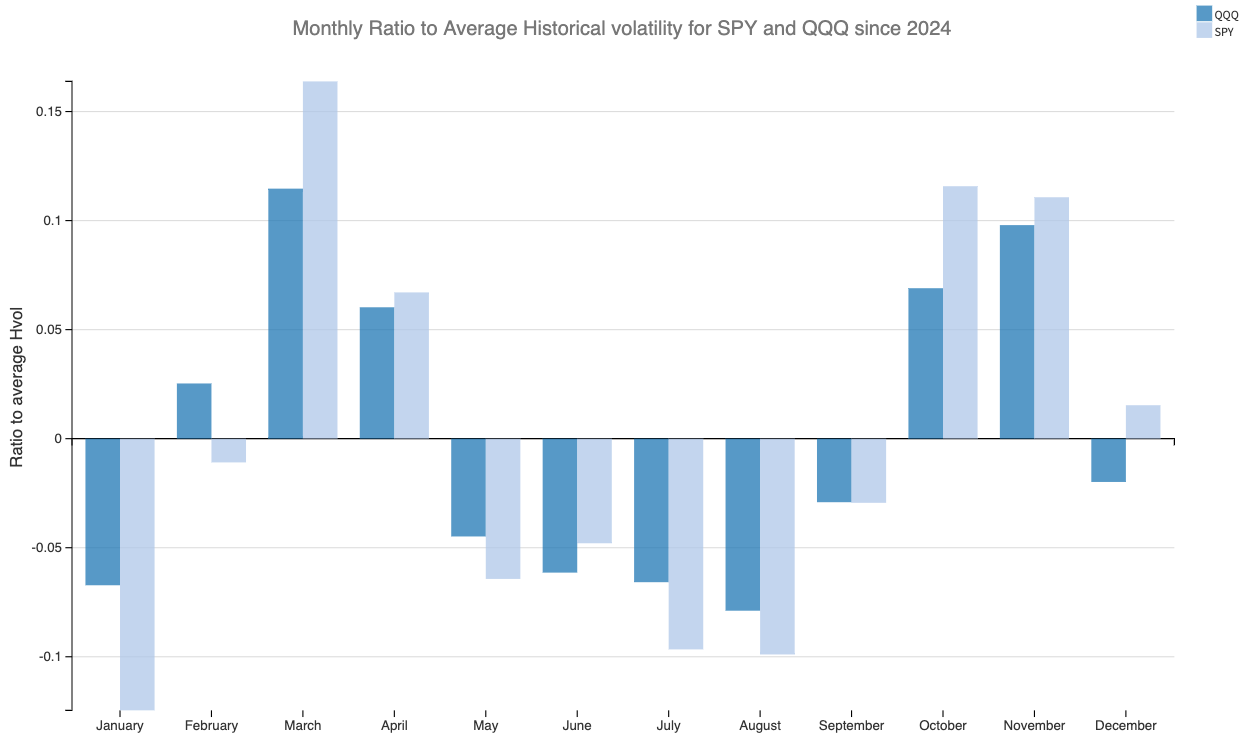

Nevertheless, we will closely monitor the situation next week as the market prepares for three FOMC meetings in the next 90 days. This period also coincides with the highest average historical volatility of the year.

In light of this, it's reasonable to suggest that the serious action is just beginning, and it's no surprise that some big players might want to trim their portfolios or at least purchase some hedges ahead of the coming weeks.

Next Tuesday's CPI reading has the potential to be quite disruptive. The consensus is a decrease from 3.9% to 3.7%, but a reading above 4% would signal that inflation may, at the very least, be much stickier than anticipated a few months ago. In the worst-case scenario, it could suggest that inflation is reaccelerating, which might lead to increased hedging activities until we have better clarity on the overall inflation trajectory and subsequent monetary policy.

While it is already priced in that there will be no rate cut in the March meeting, market participants will be paying close attention to the wording used by the Chairman and the likelihood of a June rate cut. Currently, the consensus in the marketplace is for three rate cuts throughout the year, occurring in June, September, and December.

To conclude: have you ever been on a very smooth flight when, without apparent reason, the seatbelt signs illuminate and the pilot's voice comes over the speaker saying, "We are entering a zone of turbulence. Please return to your seat and fasten your seatbelts"? That's exactly how it feels right now—we haven't changed regimes yet, but mind the bumps ahead.

In other news

It's no secret that Sharpe Two is a strong believer in AI technology. Churning out content, editing it, managing an option book, fixing bugs in a data pipeline, answering questions in the Discord channel, reading, and many other tasks wouldn't be possible without the help of multiple AI agents assisting along the way.

This week, we switched from ChatGPT to Claude, the Ai assistant from Anthropic. What prompted this change? We were initially intrigued by a recent article in which researchers claimed they had been "Clauded." While testing the tech, the model understood it was being tested and explicitly questioned the researchers about it. We wanted to see if the difference was truly this impressive, and indeed it was, particularly in verbal and communication tasks.

As we like to get to the bottom of things, we couldn't help but wonder how Claude achieves such a significant performance increase when no significant improvement to AI architecture has been made lately and the algorithm itself hasn't changed much. The answer likely lies in the training data. Recall that a year ago, Anthropic announced a strategic partnership with Zoom? It may very well turn out that human conversations from Zoom's data provide a much better training set than written HTML pages from the web. We wouldn't be surprised to see more AI companies exploring similar partnerships in the future to enhance their models' performance.

Thank you for staying with us until the end. As usual, here are a few interesting reads from last week:

We've tried to convey this message for weeks, but Amrita Roy did it much better than we could have dreamt of in this fantastic piece: "Yes, AI is in a bubble, but it won't pop just yet."

This long and extensive article from Citrini provides different frameworks for thinking about the incoming US elections. Take an hour of your time to read it; it's worth it.

This week at Sharpe Two, we discussed one of our favorite topics: market regimes. We explored how combining high implied volatility and expansion in historical volatility could lead to—well, you guessed it—Sharpe Two.

That's it for us this week. We wish you a fantastic week ahead.

Happy trading!

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.