Trade anatomy - IWM short strangle

Collecting carry despite the Labour Day stumble.

This new series will walk through the trades we present in Signal du Jour, dissecting them step by step. Every chart and forecast you see here comes straight from our platform.

If you want access to the same level of granularity, make sure to sign up. Joining in September locks in your price for good—no matter what new features we roll out down the line. See you on the inside.

Two weeks ago, we put out a piece on shorting volatility in U.S. equities. That one definitely raised a few eyebrows—after all, the VIX was sitting at 15.

But who sells VIX 15? Who??

The answer: traders who know that a price only matters in relation to the value it reflects. In this case, 15 was cheap insurance compared to the real risk it was covering.

So let’s dissect why things unfolded the way they did—and more importantly, whether there’s still enough edge on the table to press a similar trade today.

The trade

We were eyeing a short in the 230/250 strangle expiring September 30th on IWM. The structure carried a slight positive delta and, naturally, was short vega and theta. The trade-off? Gamma was not on your side—any sharp acceleration in either direction would hurt.

Before pulling the trigger, here’s what our forecasts were showing:

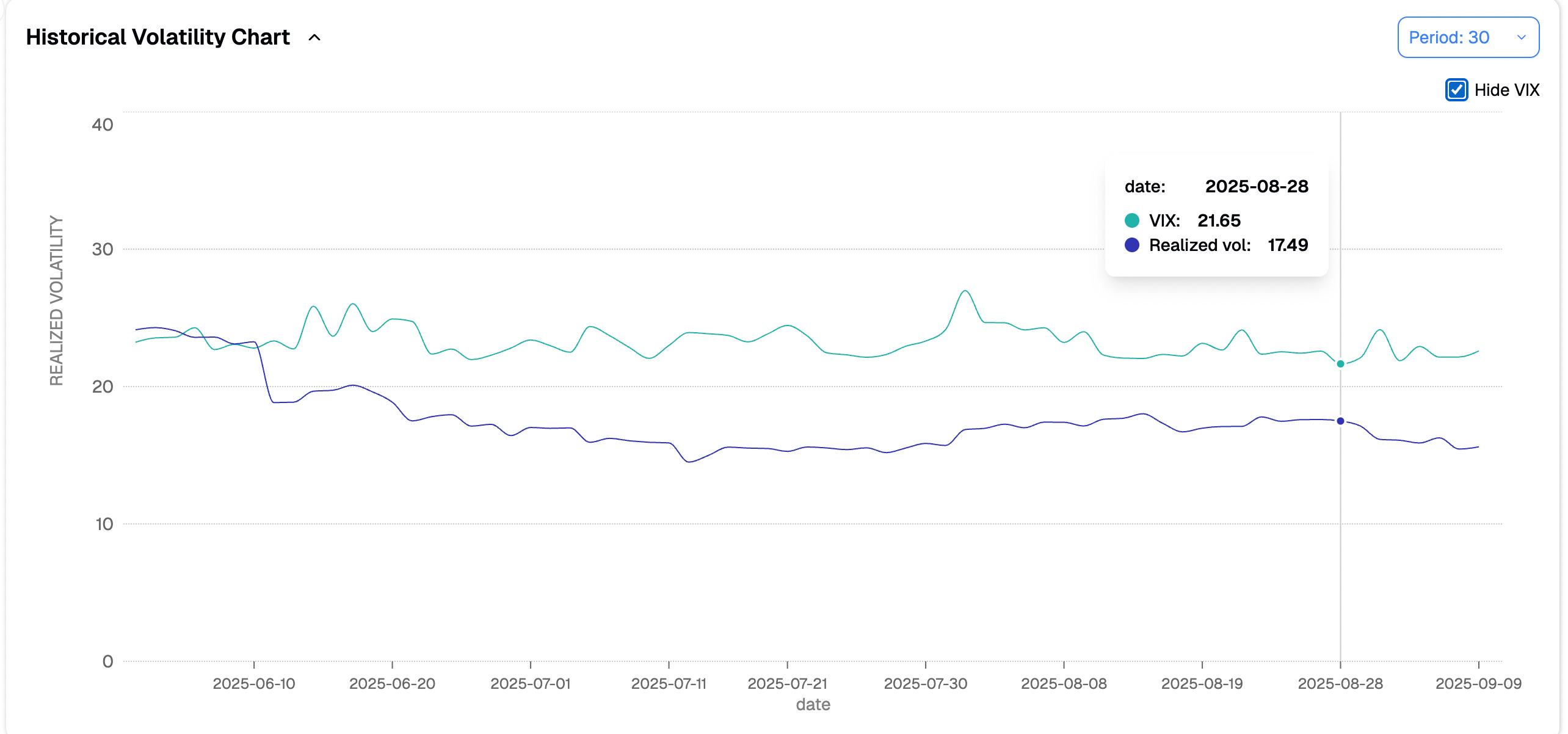

There was a 61% probability that realized volatility over the next 30 days (from Aug 28 onward) would stay below the prevailing implied level of 21.6. We also expected a non-trivial chance of IV ticking higher during that window, alongside some skew flattening—put demand was simply too light compared to calls.

In practice, that is roughly what played out. Implied vol nudged higher on Sep 2, with VIX briefly printing 19 intraday, but both realized and implied stayed contained. Implied finished a touch higher, realized a touch lower—right in line with the forecasts.

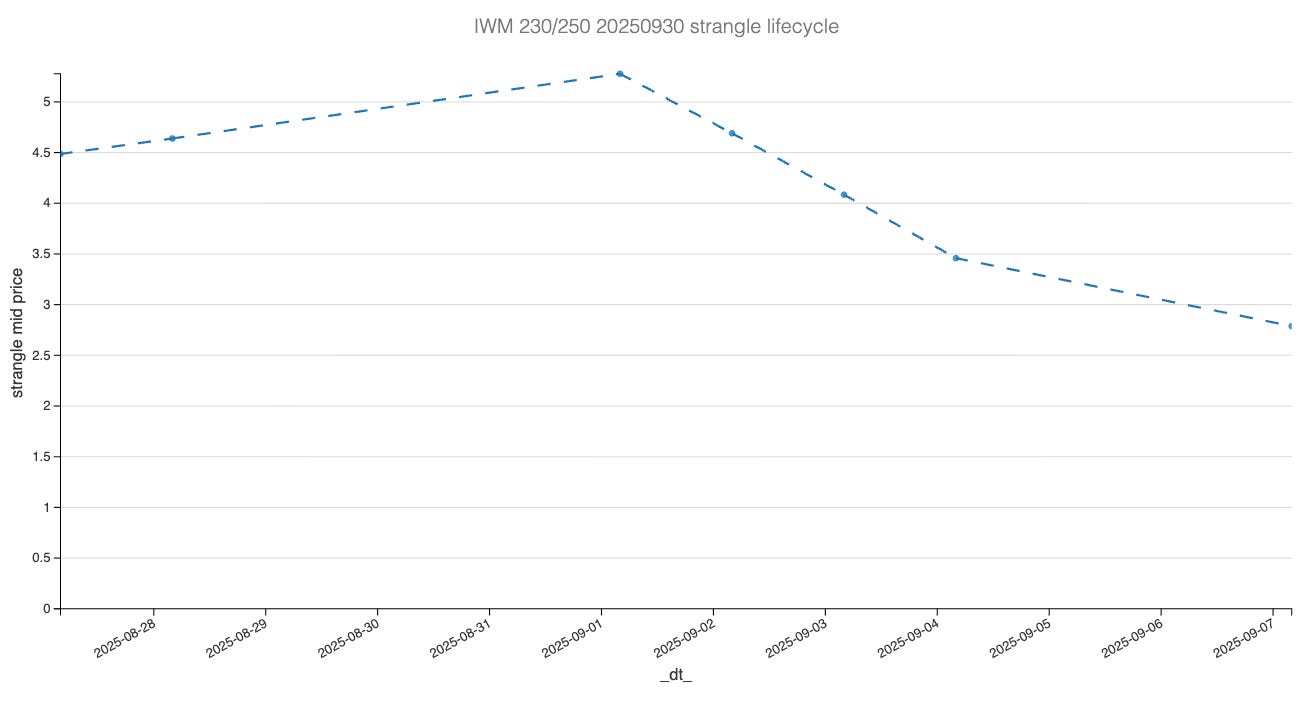

That stretch of relative calm worked perfectly in our favor. A quick look at the path of the underlying over those two weeks makes it clear: our strikes were never in serious danger.

So it is no surprise that what we sold for roughly $4.50 (assuming execution within the first half hour of Aug 28) was marking at just $2.78 by yesterday’s close. Not bad.

But if we want to think more like pros, we cannot stop at the P&L. We need to ask: was the position selection itself correct? Why this structure, why those strikes?

The answer lies in the P&L decomposition—breaking down exactly how each Greek shaped the outcome.

The greeks decomposition

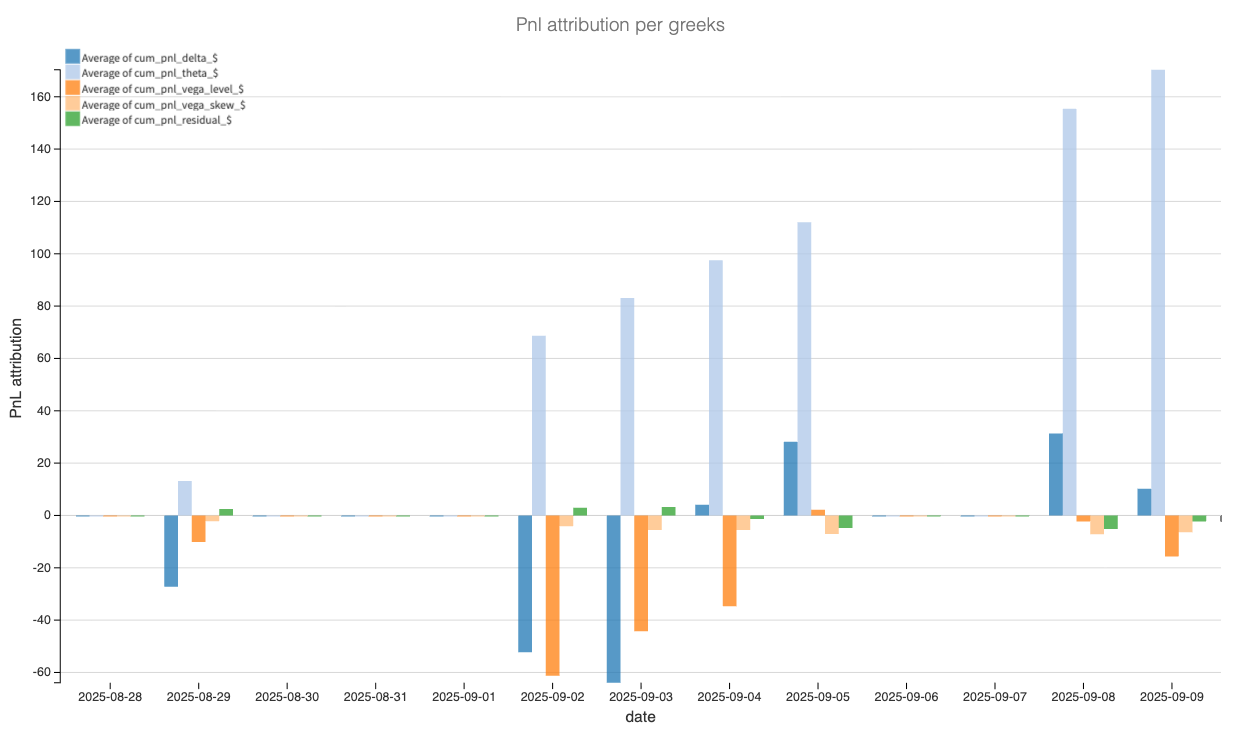

We decomposed the short 230P/250C IWM strangle day by day using end-of-day mids and dollar-Greeks. The buckets were: delta drift, theta carry, vega level (parallel IV moves), vega skew (shape shifts between calls and puts), and a small residual for higher-order or path effects. Since we did not delta-hedge, gamma shows up indirectly through delta and residual.

The story is obvious: theta did the heavy lifting. With DTE sliding from ~32 into the high teens while realized stayed pinned, carry compounded session after session. That was the core thesis—get paid by the clock, not by a heroic vol call.

As expected, implied volatility created some headwinds. Early September brought a pop in IV, and those days show up cleanly as negative vega-level bars. Once IV normalized, the drag disappeared. This was never meant to be a “vol collapse” trade; it was about harvesting carry while IV wiggled around.

Vega skew was a non-event. Call/put repricing relative to the level netted close to zero most days, and with no meaningful skew shock, the position barely felt it.

What about our expectation of the index drifting higher? Delta did its part. At entry, the strangle carried a small long-delta tilt (~+0.15). On the up days (9/5, 9/8–9), that bias added dollars; on the down days (8/29, 9/2–3), it gave some back. In the end, directional P&L was supportive but clearly second-order to the carry.

Residuals also stayed small, exactly as expected. That bucket covers vanna, vomma, gamma path effects, bid/ask noise, and model mismatch—no structural surprises hiding there.

All told, the trade delivered exactly as framed: mostly theta, a touch of delta drift, and manageable vega bumps. For a short-vol carry setup, those are the right fingerprints—steady positive theta, the occasional negative vega-level day that never overwhelms carry, and minimal skew impact.

So the big question: do we put this trade back on? Is there still enough edge to justify re-opening a similar setup, roughly at the 30-DTE mark?

Let’s take a look.