With just two weeks left until year's end, we're entering what's traditionally the least volatile period. It's important to distinguish between volatility and movement in the underlying asset. An asset can exhibit minimal volatility yet undergo significant drift, dragging the unwary volatility traders into deep water.

This is because most asset classes are not mean-reverting and can experience drift. In such scenarios, delta hedging or reassessing your strategy becomes essential to avoid substantial losses—our recent short vol position on $TLT is a prime example.

At Sharpe Two, we are all about making our lives easier. We zero in on mispriced implied volatility so significant that we're willing to take on the risk of underlying drift for the comfort of not defending a position.

But the best way to make our life easier?

Look for assets that don’t drift and tend to hover around their mean.

Which asset fits this bill? Volatility itself. Selling volatility on volatility? Phew, this is getting … $META.

Nope, $VXX is all we need.

Oh and if you haven’t subscribed yet, we have a Christmas present. You don't want to miss 50% off for all of 2024!

The context

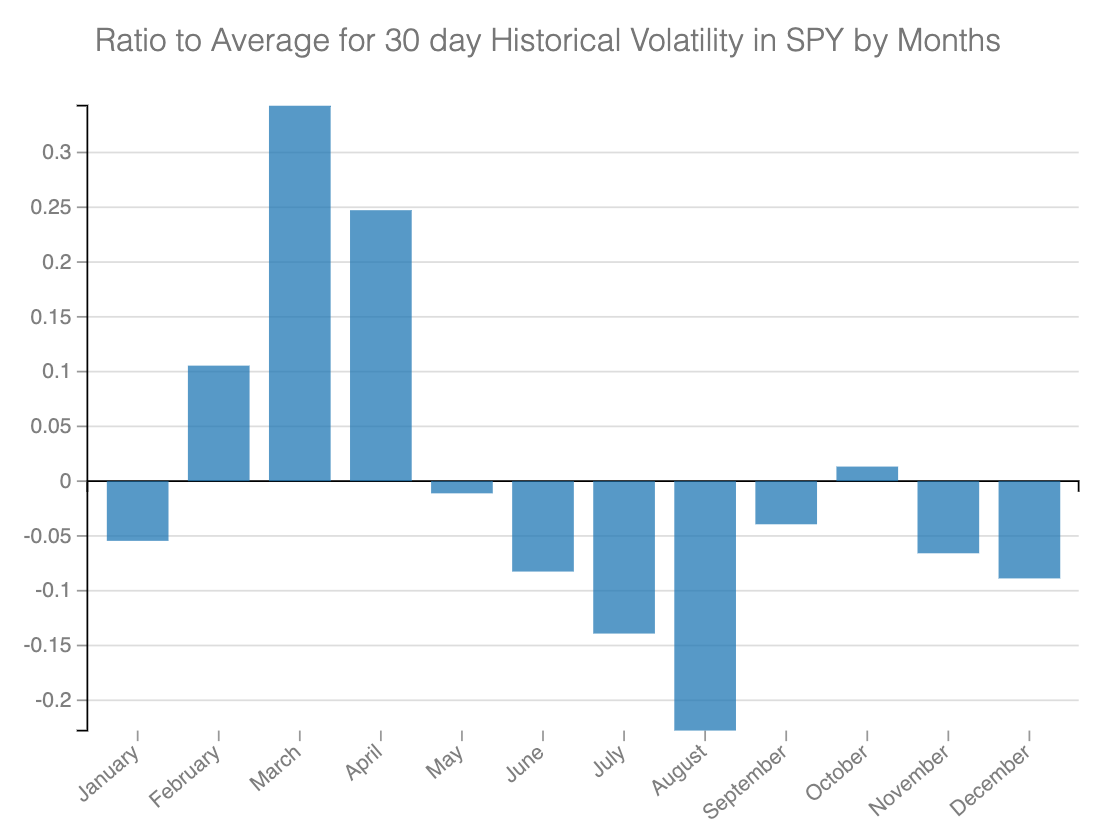

It's no secret that traditionally, December sees a slowdown in market activity as participants take time off to be with their loved ones. As illustrated in the chart below, aside from the summer months, the realized volatility in SPY over the past ten years tends to hit its lowest point in December.

During this period, fund managers often shift their focus to more administrative, albeit vital, tasks such as managing capital gains tax and optimizing portfolios. Market flow usually thins out, and the demand for protective contracts is generally more subdued.

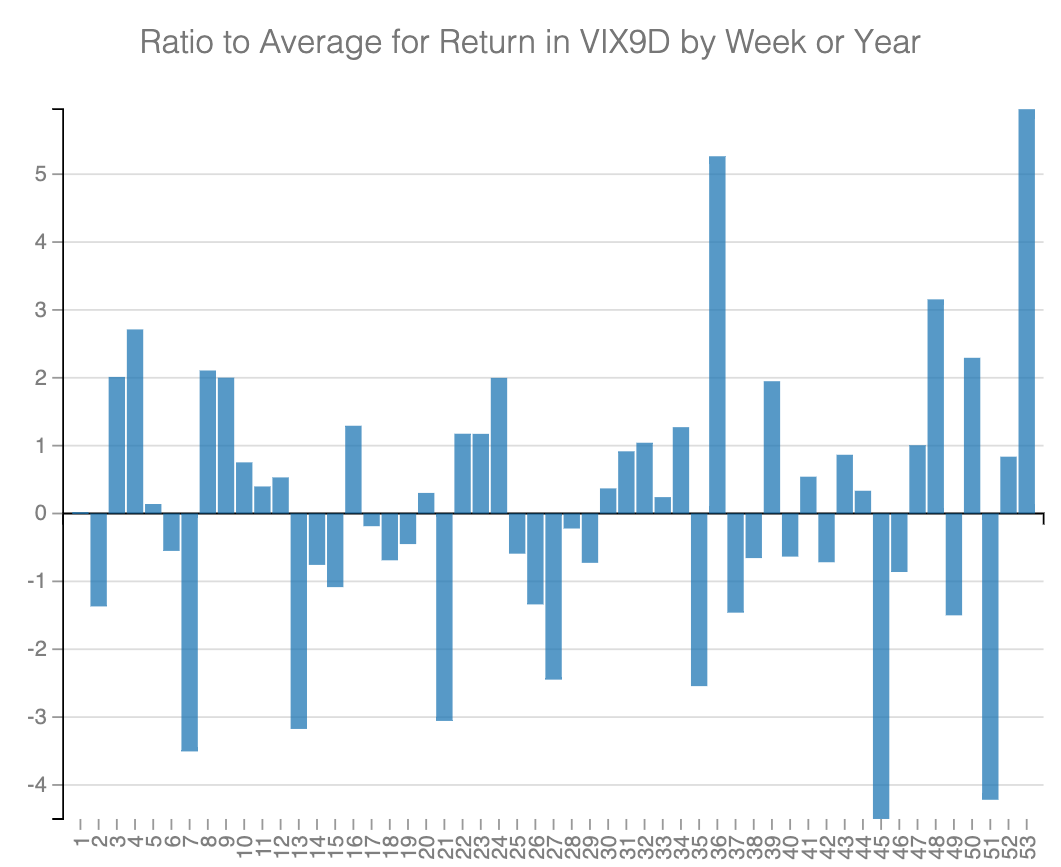

Now, let's turn our attention to VIX9D. This index is similar to the VIX but uses options to expire in 9 days, offering a clearer picture of the short-term anticipated risk.

Traditionally, Week 51 witnesses the lowest demand of the year regarding volatility.

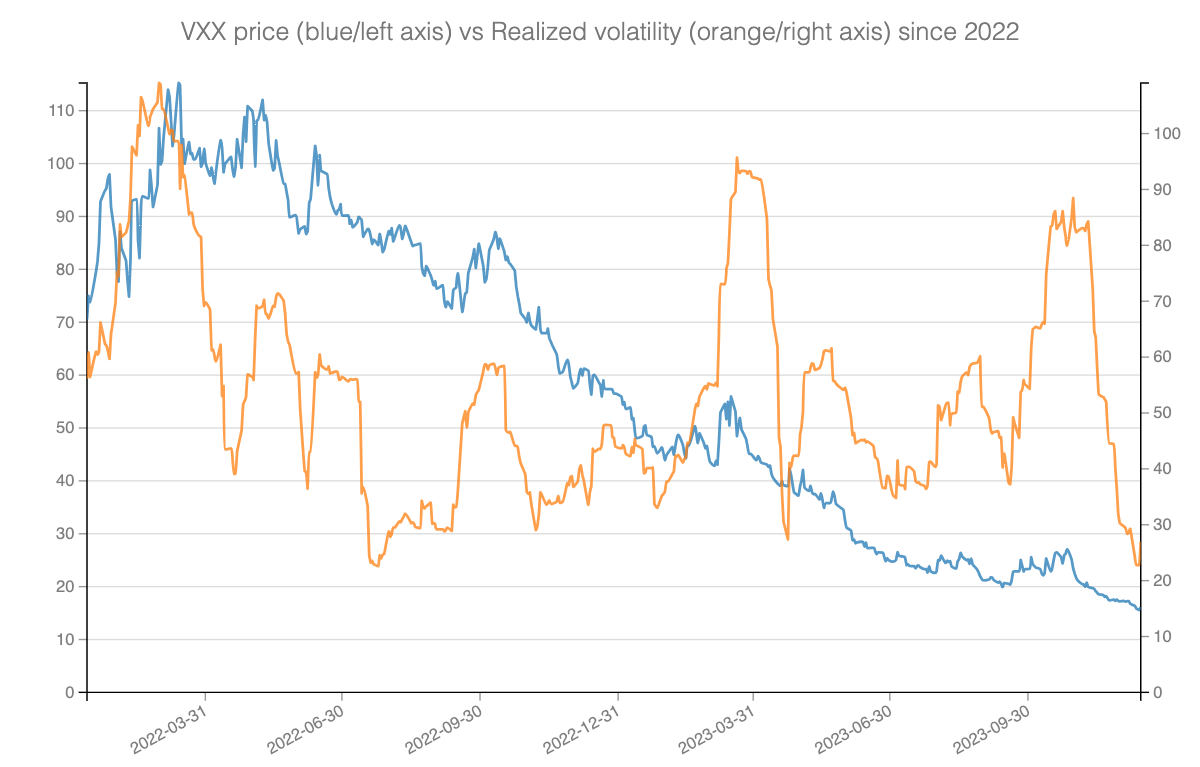

While the VIX itself isn't a tradable asset, we can still leverage this information. This is where VXX comes into play. VXX is a leveraged Exchange-Traded Product (ETP) well-known in the volatility world, alongside other VIX ETPs, for its tendency to trend towards... zero. Yes, you read that correctly. Designed to replicate the VIX index returns using futures, the contango effect in these products often leads them gradually toward zero over time. Take a look here:

The chart shows that the product slowly descended to zero, punctuated by occasional spikes when the VIX spikes. Some might suggest always being short on VXX. While there's nothing inherently wrong with this strategy, it's crucial that the sizing is appropriate. We'll delve into this in more detail in a future piece.

But shorting VXX isn't the only way to profit from it. You can also dip your toes into the options market. Instead of predicting the direction and exposing yourself to the periodic spikes, you can express a view of the underlying asset's volatility.

Given that Week 51 is traditionally not very active, let's explore if there's enough premium in the options market to consider a trade on the shorter end of the expiration cycle.

The signal and the trade methodology

A common misconception in the retail space about the VIX and implied volatility is that the VIX rises only when there is imminent risk in the market.

That is not true. It can rise even without immediate apparent risks in the market. This happens because the VIX methodology incorporates the prices of Out-of-The-Money (OTM) options, both puts and calls, and in case of a sudden rally driven by out-of-the-money calls, VIX can go up.

Reflecting this, with the prevailing bullish sentiment, VXX saw an increase of 3% on Friday, closing around 16.14.