Signal Du Jour - short volatility in GDX

A post April fools trade

Yesterday was the first trading day of the quarter, and we were pleased to see VVIX return to above 80. We were even more delighted to receive all the messages calling us out on our April Fools' joke. There was no silent retreat, ChartsTwo, or deep learning model to read technical analysis charts at scale.

We are a volatility trading publication and intend to stay one. Forever.

About a month ago, we entered a position in GLD as implied volatility was creeping up. Today, we turn our attention to GDX, the ETF tracking gold mining companies. The precious metal's movements directly impact the sector, and as the tension around gold remains elevated, volatility sellers can take advantage of this.

Let's have a look.

The context

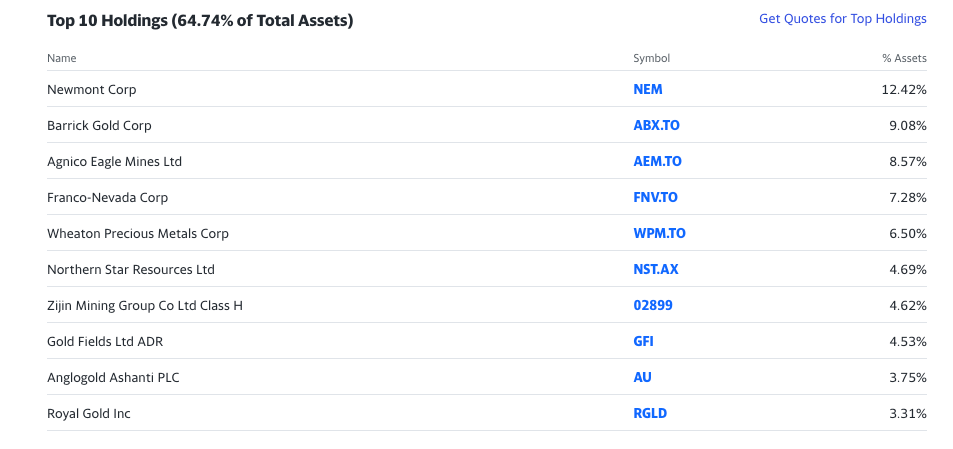

GDX is a popular ETF for gaining exposure to gold, but few understand that it is not a one-to-one correlation. Because this ETF tracks gold miners, it is impacted by metals' movements, but it also has its own dynamic. First, it is a concentrated ETF; about ten names represent 67% of the funds, with the top 5 taking 45% of the allocation.

When you buy GDX, you essentially get a lot of exposure to sector leaders like Newmont Corp and Barrick Gold. So much so that if you are a pair trader, there are some things to consider.

As volatility traders, our first stop is the realized volatility over the past few years to gauge the product's propensity to move. The least we can say is that since 2022, the price range between the low 40s and the low 50s has been fairly predictable. However, we’ve seen smoother price curves in the past.

As a result, the realized volatility is constantly above 25 and tends to exhibit periods where it will peak or decrease sharply, depending on the context of the underlying asset.

As a result, we can anticipate seeing the price of options reflect the relative risk in GDX. First of all, a reconstruction of the VIX index for GDX is somewhat elevated to account for the sharp movements up or down typical for this ETF.

With an average value of around 45 and some impressive peaks to the upside, this chart confirms our intuition. It indicates that option prices tend to overstate the actual realized movement in the underlying. This opens good opportunities for volatility sellers.

Let's look deeper into the data.

The data and the trade methodology

At this stage, it is important to decide which part of the expiration we should trade on. For that, we will build the variance risk premium for each available expiration in the contract.