Despite a minor intraday reversal yesterday, the US equity markets definitely have a holiday feel. Everything finished somewhat flat, and while VVIX has been consistently picking up from the very lows of the end of June, we can almost hear the crickets singing.

The good thing about trading a wide basket of geographies and asset classes is that we don’t have to stick to the US. Last week, we presented a trade on KWEB and Chinese internet stocks—today, we will focus on YINN, a leveraged ETF offering investors the possibility of getting three times the exposure to Chinese equities.

Let’s have a look.

YINN is giving 3x the performance of FXI… really? Yes.

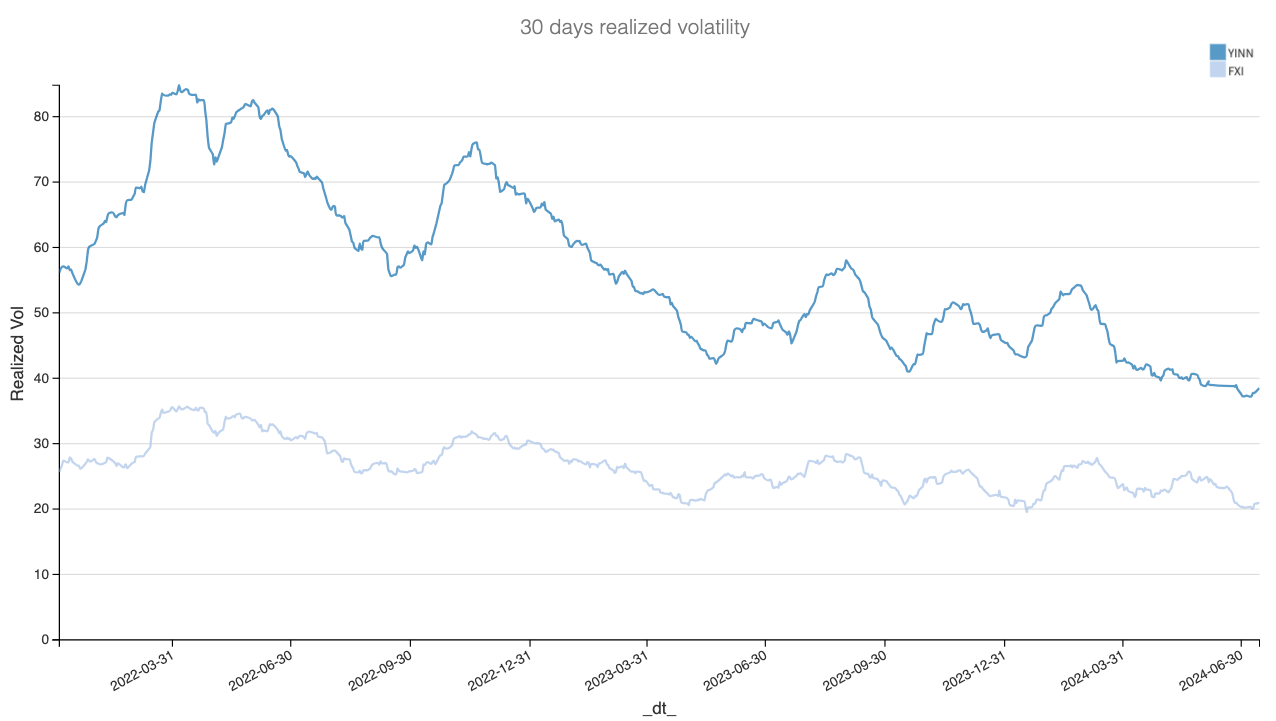

YINN is FXI on steroids: it aims to replicate three times the daily performance of the FTSE China 50. You might be jumping in your seat, looking at this chart, and thinking, "Well, clearly, they are not doing a really good job at it: FXI is up 13.7% while YINN is up 26.45%." And… you would be wrong. The same "optical illusion" happens when you look at the realized volatility chart.

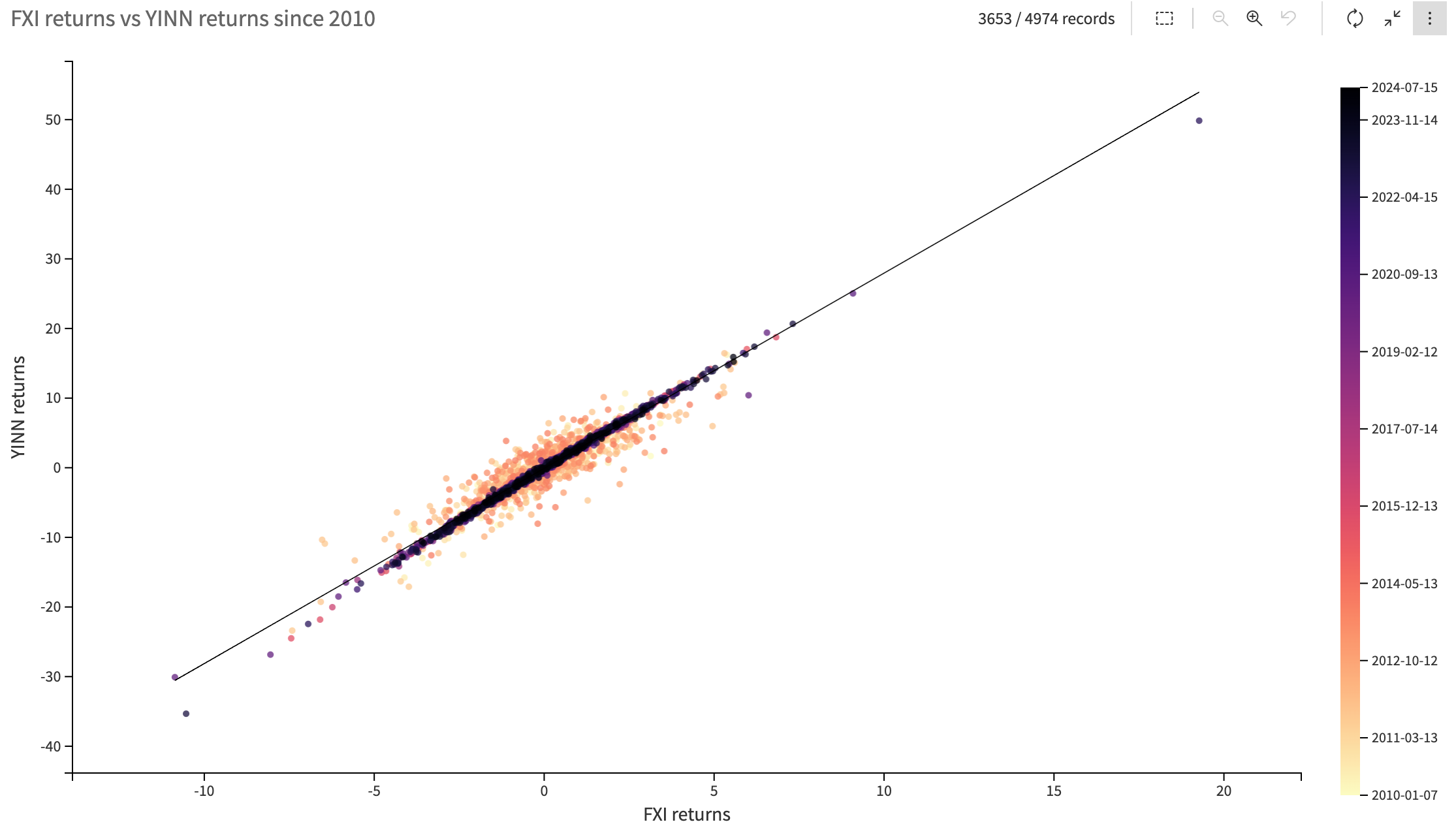

Percentages and prices are always very deceptive and hard for the human mind to fully grasp. The picture looks much better if we compare the daily returns of YINN and FXI since 2010.

If things were shakier in early 2010, opening the door for some very easy pair trading between the two, things would be much tighter … except when FXI losses are "abnormal." In this situation, the replication in YINN tends to overestimate what was realized in the index—something to keep in mind for pair traders.

This is interesting for volatility traders. We know that volatility is often measured as the standard deviation of log returns (that is at least how we compute it at Sharpe Two, using high-frequency data to get a measure of integrated or instantaneous volatility, which is much more precise than using daily returns). As the chart just showed, the replication is often really good but not perfect.

What do you think options traders will do regarding such a product? Add an extra buffer to avoid getting burnt if something bad happens in the ETF management.

Let’s have a look.

The data and the trade methodology.

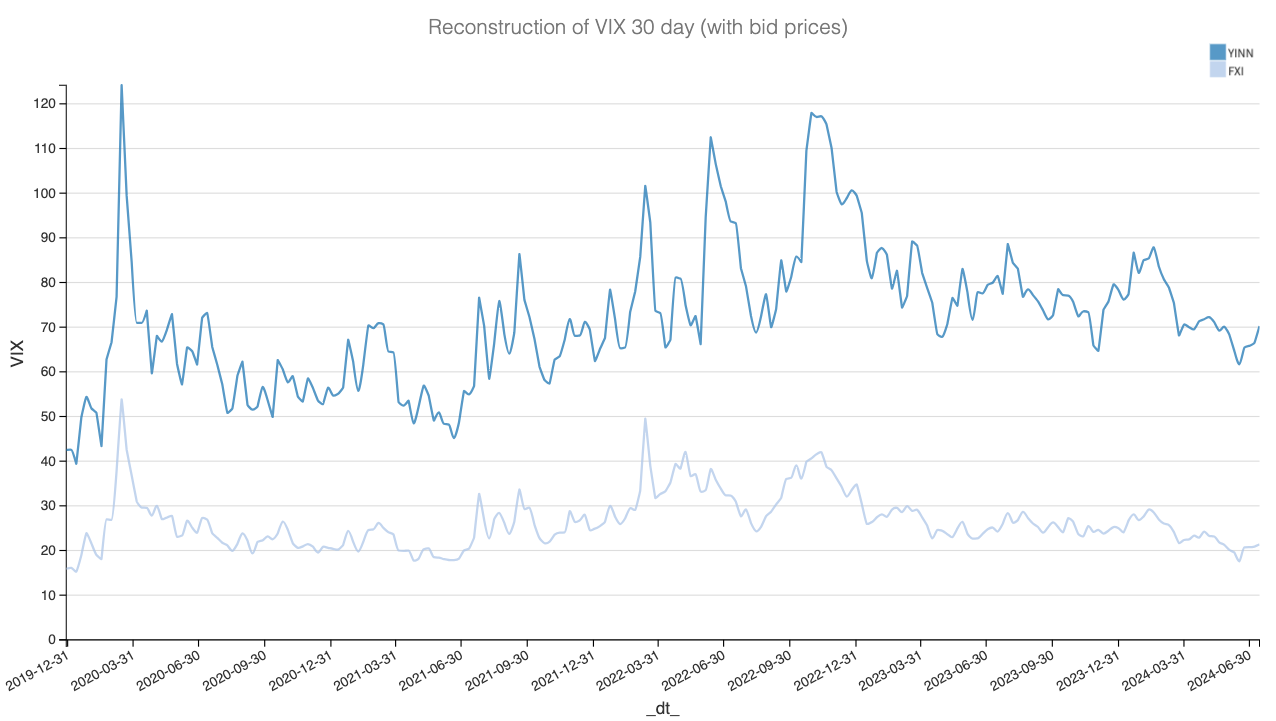

Let’s start by looking at the implied volatility at 30 days for YINN, calculated using the VIX formula (interpolation between two variance swaps around 30 days to expiration).

Interestingly, although not perfect, the options prices between the two products are visibly much better at incorporating the three x-factors between the implied volatility, especially when things are fairly calm and quiet, particularly since 2023.