Signal du Jour - short vol in XLP

Playing the "markets react then think" mantra.

Flat.

When every commenter expected a sanguine opening for the futures on Sunday evening, the market again did the opposite and opened flat. We won't lie—we're in the camp of those surprised, considering how gloomy the newswire felt over the weekend. However, given that we took the scary short volatility trade over the weekend, we can't hide a little bit of satisfaction this morning.

We started last Monday with a tactical hedge in SMH. It probably paid off if you kept it over Friday, but we wouldn't recommend holding it much longer.

This week, though, there's no tactical hedge on Monday, and we'll continue taking the scary trades—after all, that's what we're paid for. However, as we explained in our Sunday Note, we'll take calculated risks as much as possible.

We're considering XLP, the ETF tracking consumer staples. Why? It's traditionally a defensive sector. If even companies selling cigarettes, toothpaste, and diapers are severely impacted by the geopolitical context, we may have bigger problems than managing risks in short straddle positions.

Let's take a look.

The context

Enough with the geopolitics. Iran and Israel are going at it; we get it. For us volatility traders, this automatically creates opportunities, as the market tends to overreact rather than think. In the process, it may lift prices in asset classes that are usually stable and predictable.

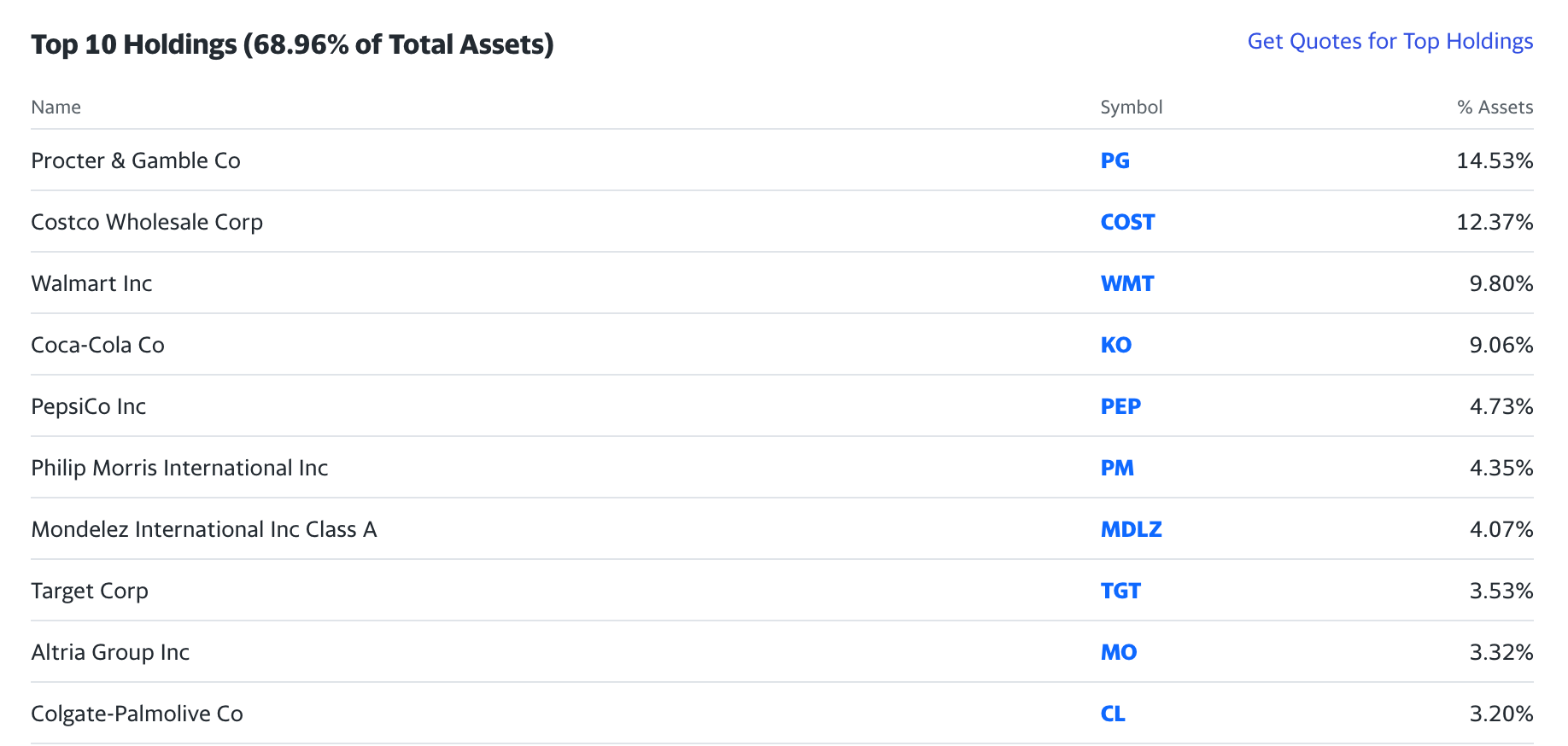

That's precisely the case for XLP, the ETF tracking consumer staples—the stuff consumers need, no matter what. It's a concentrated ETF, with 69% of the assets in 10 holdings.

All these names will be very familiar to readers outside of our American readership. They sell products that are easily recognizable to consumers worldwide. Considering the day-to-day nature of the items sold, XLP rarely deviates much from its long-term mean and usually experiences limited volatility.

Despite the war in Ukraine, seven rate hikes, a regional bank crisis, some intense debate about inflation, and a crazy six months, XLP has remained steady, hovering around $70. Its realized volatility, however, hasn't gone above 15 since January 2023, and it spent all of Q1 2024 below 10.

Now, let's examine the volatility profile and see how recent events have created some opportunities for short-term volatility.

The data and the trade methodology

Let's verify our hypothesis about relative stability in XLP by examining the volatility term structure.