Signal du Jour - short vol in XLC

VRP trades are harder. Not impossible.

Another quiet week should be ahead of us—unless inflation goes through the roof or Powell announces a rate hike. In other words, anything different from the same narrative we've heard for three quarters in a row now. You get the idea.

At this stage, we won't pay too much attention to these things. We don’t say they don’t matter but the mojo is simple: wake us up when VIX crosses 16 again. In the meantime, we have to scout the corners of the market where the premium hasn't completely vanished and where it's still reasonable for VRP harvesting strategies.

Let's not kid ourselves; it will become increasingly more complicated at VIX 12.5, but not impossible. Today, we look into XLC, a sectoral ETF tracking the communication sector. With the earnings for the major players in the group behind us—Disney reported last week—things should stay relatively quiet.

Let's get to it.

The context

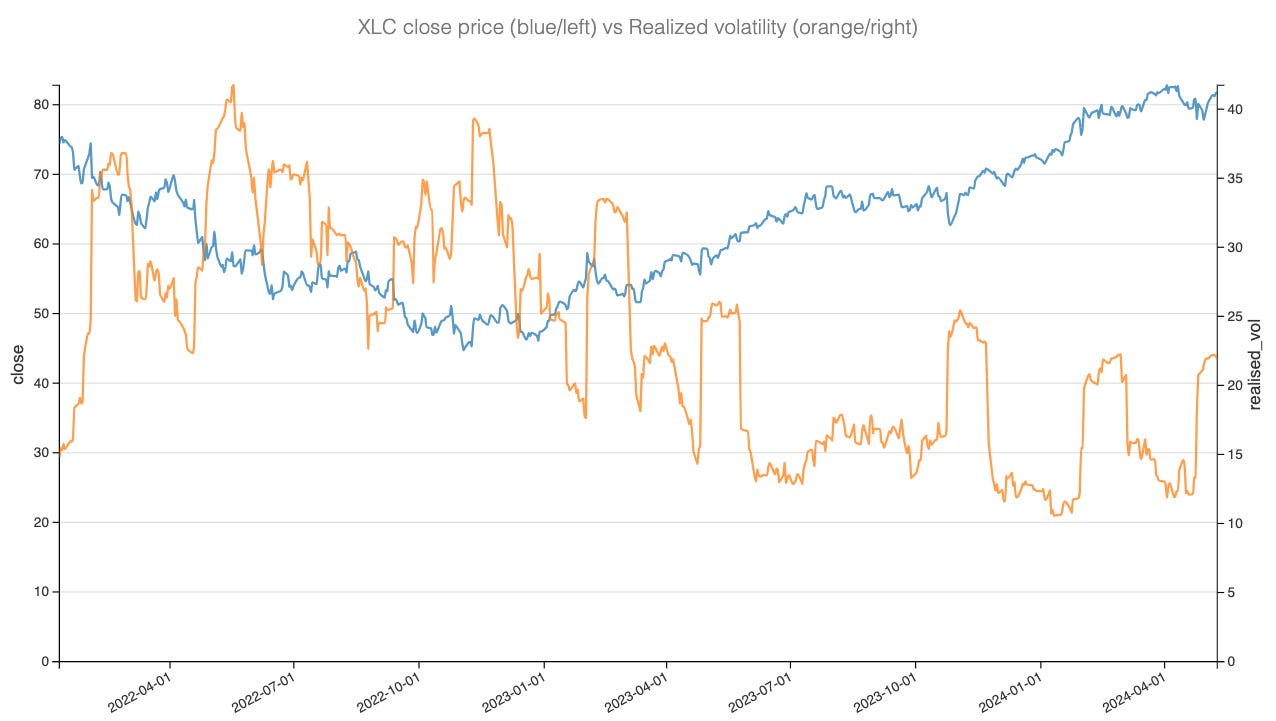

The communication sector has been doing well in 2024, and as a result, the realized volatility in the space has been fairly contained over the past 12 months. Yet, the importance of earnings for companies like Meta, Google, Netflix, and Disney has propelled it to the highest levels observed in the last 12 months.

This chart looks pretty amazing, doesn't it? Every three months, almost clockwise, realized volatility climbs to the highs of a period before slowly going back to normal until the next earnings season when the market will dissect once again the results of these heavyweights.

At Sharpe Two, we like to make weak predictions on realized volatility before entering a trade. In this particular case, it's extremely tempting to think that the current 23% post-earnings will slowly become 15% unless something major hits the newswire.

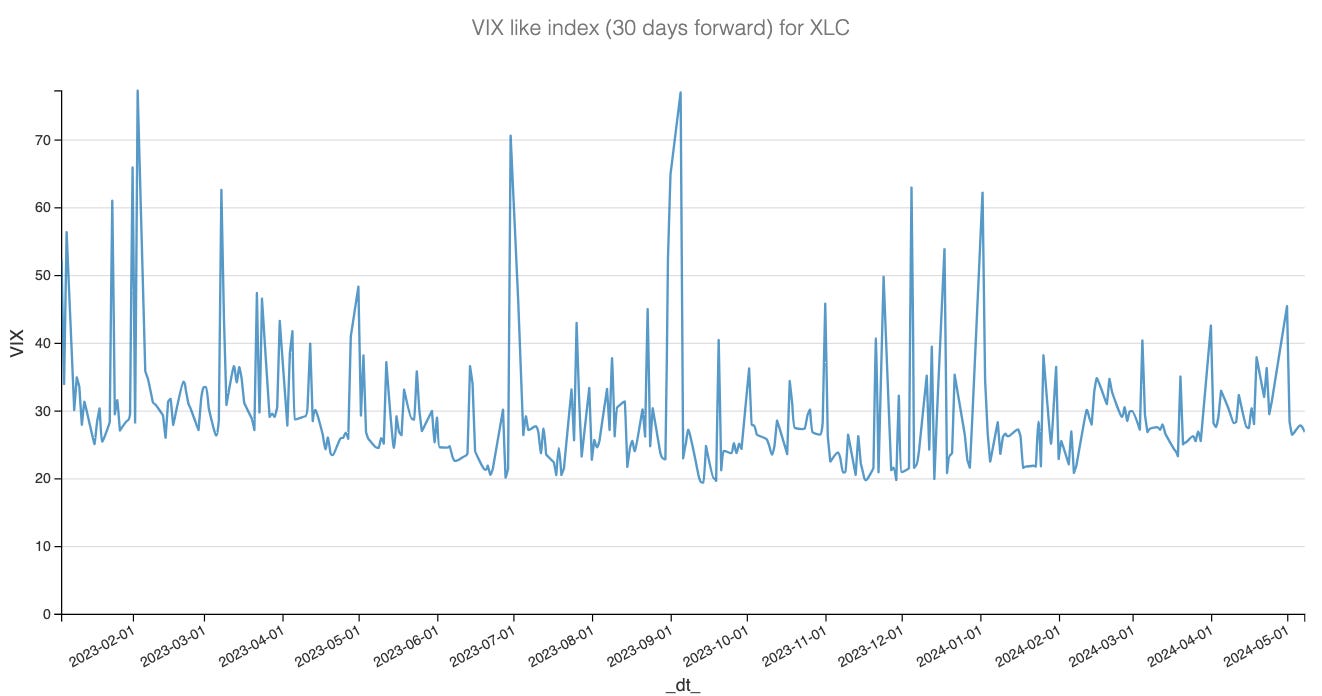

Right now, a first-level view of the options for XLC doesn't point in that direction. The VIX index for XLC using the price of 30 days OTM options, is not at some normal readings observed the past year, and already much lower than what we observed throughout the earnings season.

With things having normalized, let's now identify which part of the market still offers the best opportunities for volatility sellers.