Signal Du Jour - Short Vol in USO

24 points VRP is hard to ignore

6th day of the conflict started by the US and Israel against Iran and the confusion is still at its peak. Who will run the country now? How long will the operation last? When will the Strait of Hormuz reopen? The list of questions is as long as your arm, and the answers are hard to gather. Yet, a few signs start to point towards a path to normalization (despite the media frenzy, which as a side note from a rational observer from Dubai, is half comical half embarrassing: isn’t there some real conflicts on the planet, with actual footage to report on?). First of all, as expected, the stockpile of missiles from Iran is apparently depleted and/or they may be unable to fire them anymore due to the systematic destruction from the US and Israeli forces. Second of all, the foreign minister of Iran has opened the door to a complete shutdown of the nuclear program, as long as the US does come with a satisfactory solution. It may be a bit of a stretch to see something happen within the next 24 hours. But what is the probability it happens over the next month? The next three months?

Let’s be clear about our position right now and throughout this article: we are not calling for an immediate resolution of the conflict, who knows exactly when it will happen, but we are betting that the market is grossly overestimating the risk of contamination or escalation from here.

Let’s have a look.

The Context

Two major interventions in two of the biggest oil producers on the planet which also happen to be big commercial partners of China, some may call that an accident, but … we don’t. Especially when the only superpower close to rivaling the United States is indeed China. These interventions gave the US some strategic repositioning in the Panama Canal as well as the Strait of Hormuz, which is pretty timely to control the flow of oil, and increase pressure on China’s interests if need be.

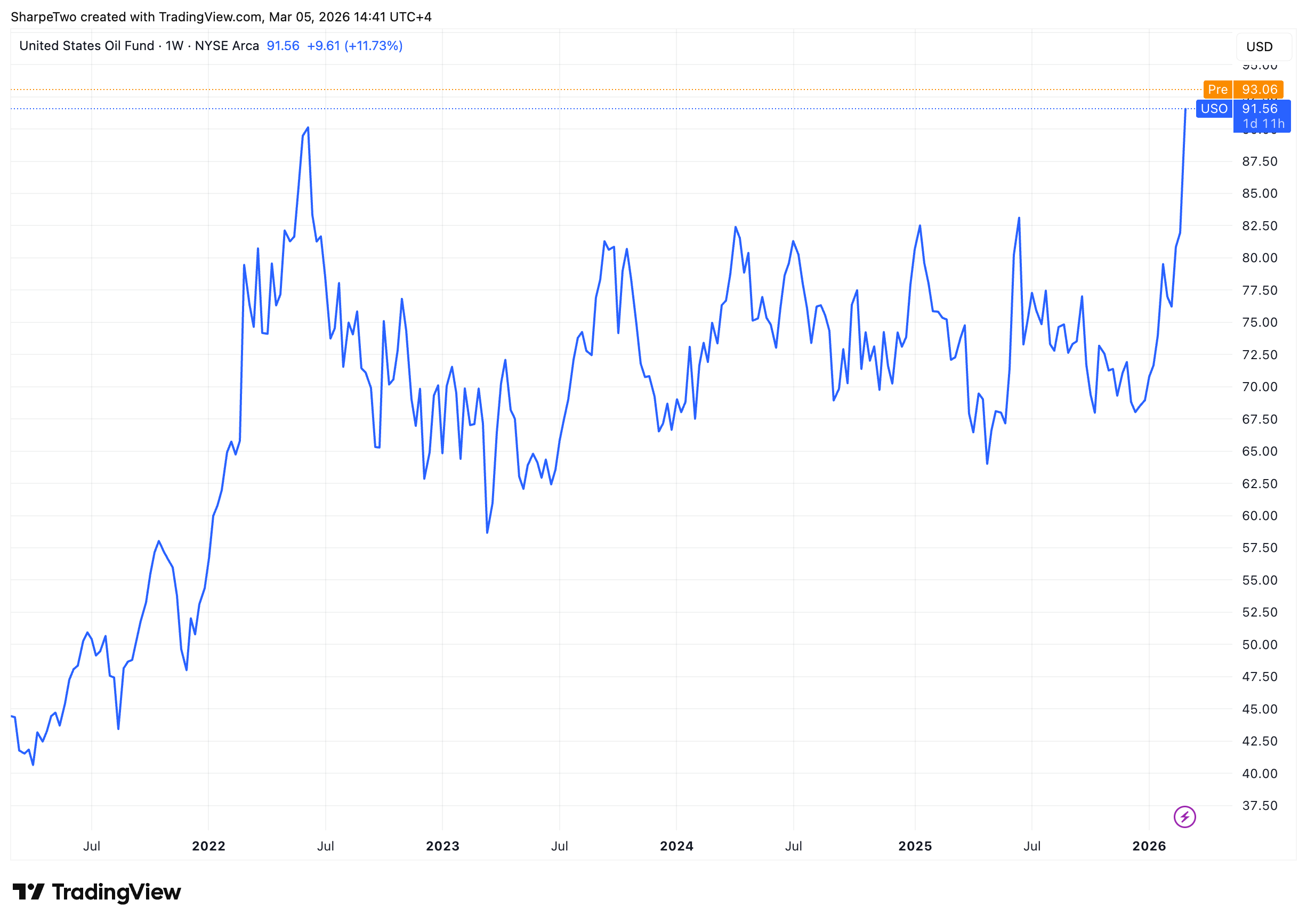

USO is now at an all time high of five years, which is well timed, as Trump and Xi are supposed to talk to one another in about 28 days from now, to discuss trade, tariffs, Taiwan and … well what happens in Panama and Hormuz. That is a longer context than we usually allow ourselves to do, but we thought it was good to put it back at the center of the conversation: while missiles and fireworks tend to distract the plebe, the real talk, in the end, is always money.

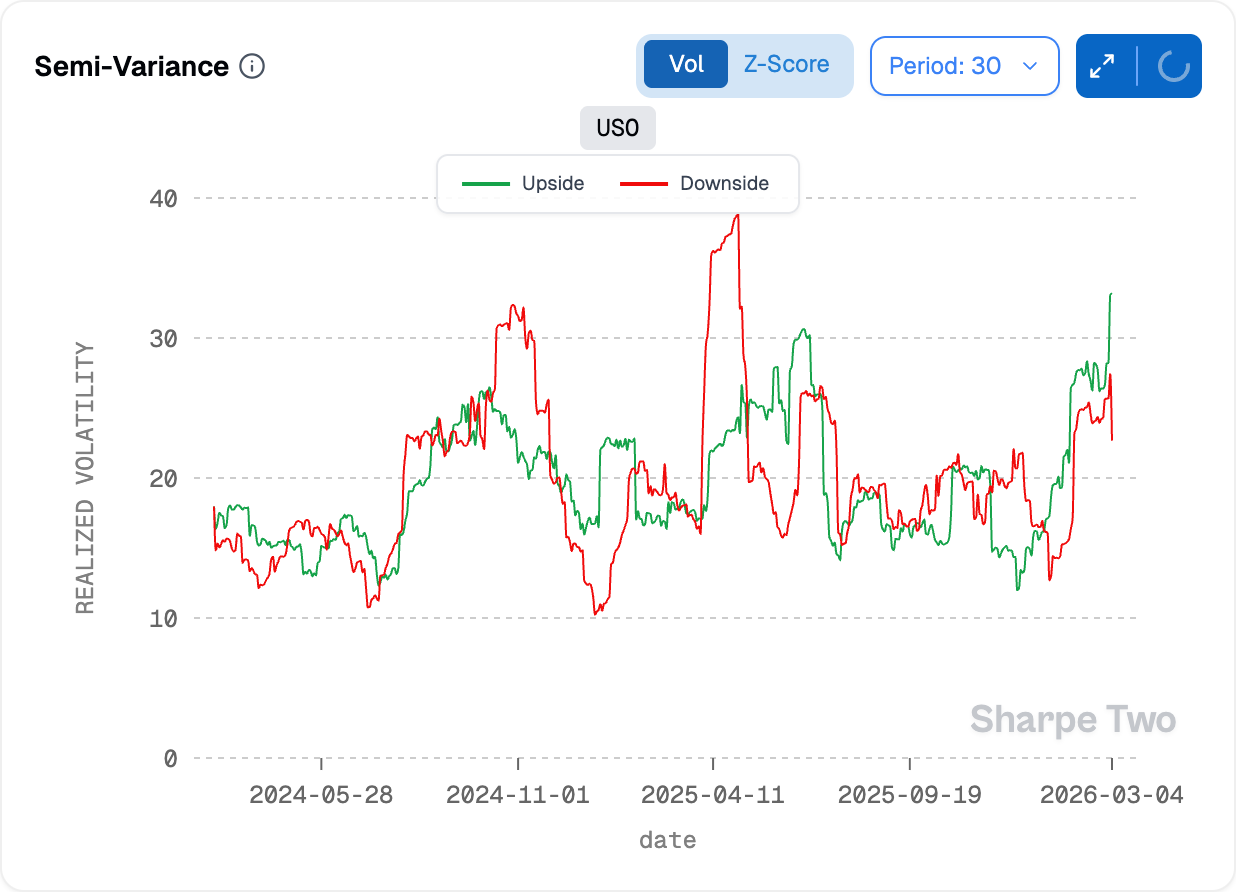

Trading at all-time highs was obviously not without consequence on realized volatility

From low 20s at the end of the year to low 40s 10 weeks later, the numbers are speaking for themselves: the market is pretty confused as to where all of this is going and in doubt, they keep buying at a hefty price. Because at the moment, most of the realized volatility is done on the upside, and very little on the downside

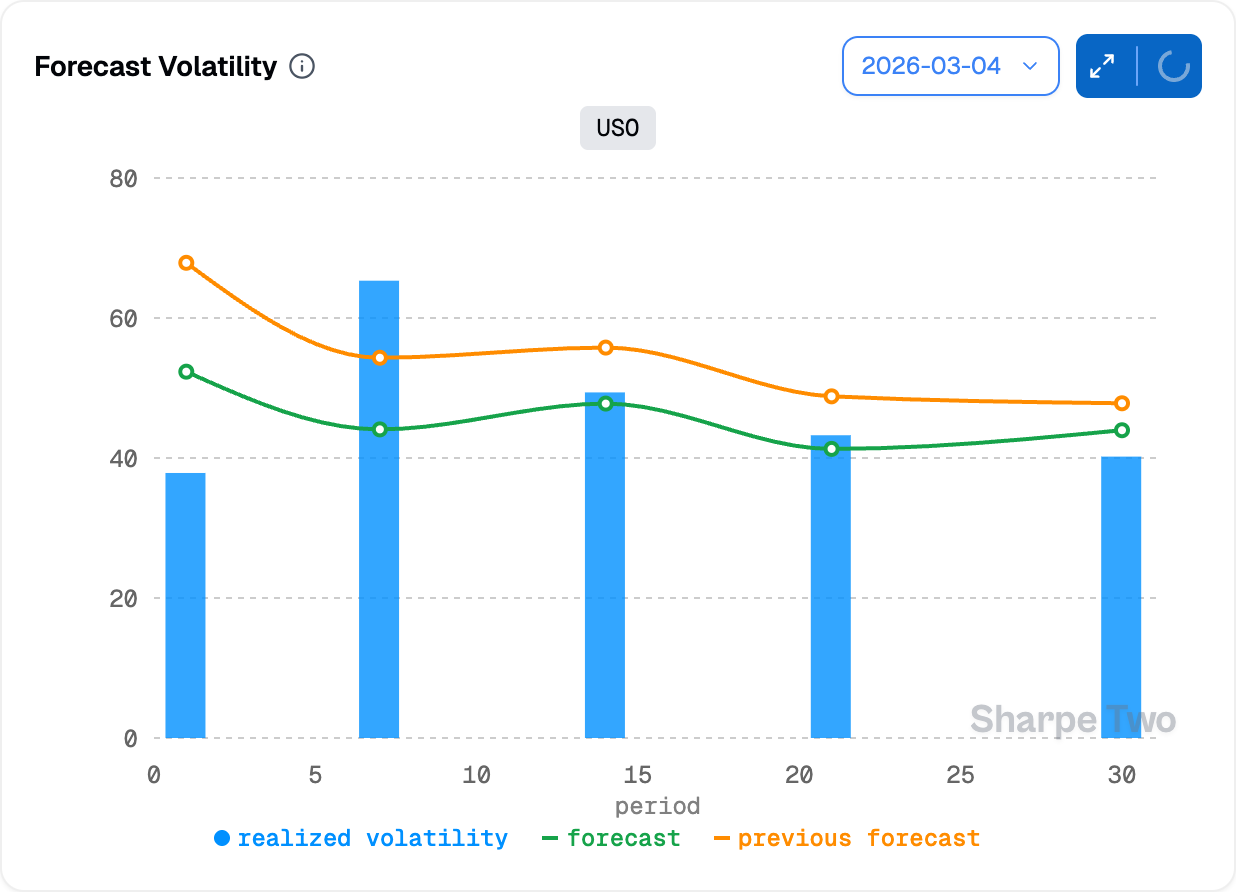

This has also some expected consequences on the skew of the implied volatility surface and we will see that in a later part of this article. Yet, in that context, it is pretty hard to predict where realized volatility will be. If things calm down over the next two weeks, how will prices react? Crater and stabilize? Mean revert quietly? Or stay there in anticipation for the next move from Trump? Not a simple way to look at it. From a data standpoint, things are no less blurry.

Yesterday’s forecast was at 47s, today closer to 40s, which reflects the high level of vol-of-vol, characteristic of these regimes where pretty much everything is up in the air and subject to change with the next headline.

Sounds scary? Great. That is exactly why the market may be overpaying for insurance. Let’s have a look at what the options market is now saying.