A week with a combination of FOMC and NFP plus earnings from AMZN and MSFT: it feels like Christmas ahead of time! Gear up for some intraday volatility and try to avoid getting caught in reversals. We admit it's easier said than done, and that's why we prefer a market-neutral strategy over directional bets and focus on implied volatility.

That said, markets are now global, and we don’t have to focus on a specific geography or asset class. Today, we explore a trade in USO, the ETF, that exposes us to various futures contracts on oil. This doesn’t mean oil won’t move if the markets experience significant disruptions. However, we think it may move less than other asset classes and, more specifically, less than the options markets imply.

Let’s take a closer look.

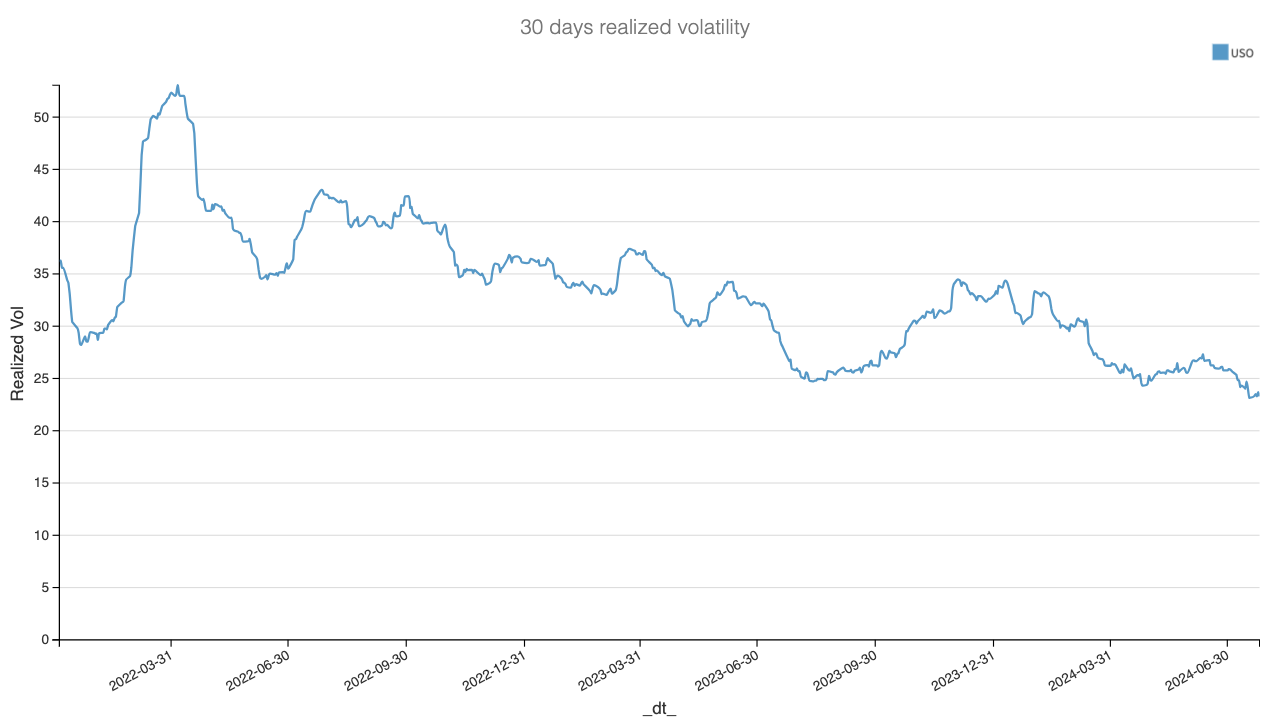

USO prices remained within a well-defined range between 66 and 82, defying the forecasts of even the most advanced analysts.

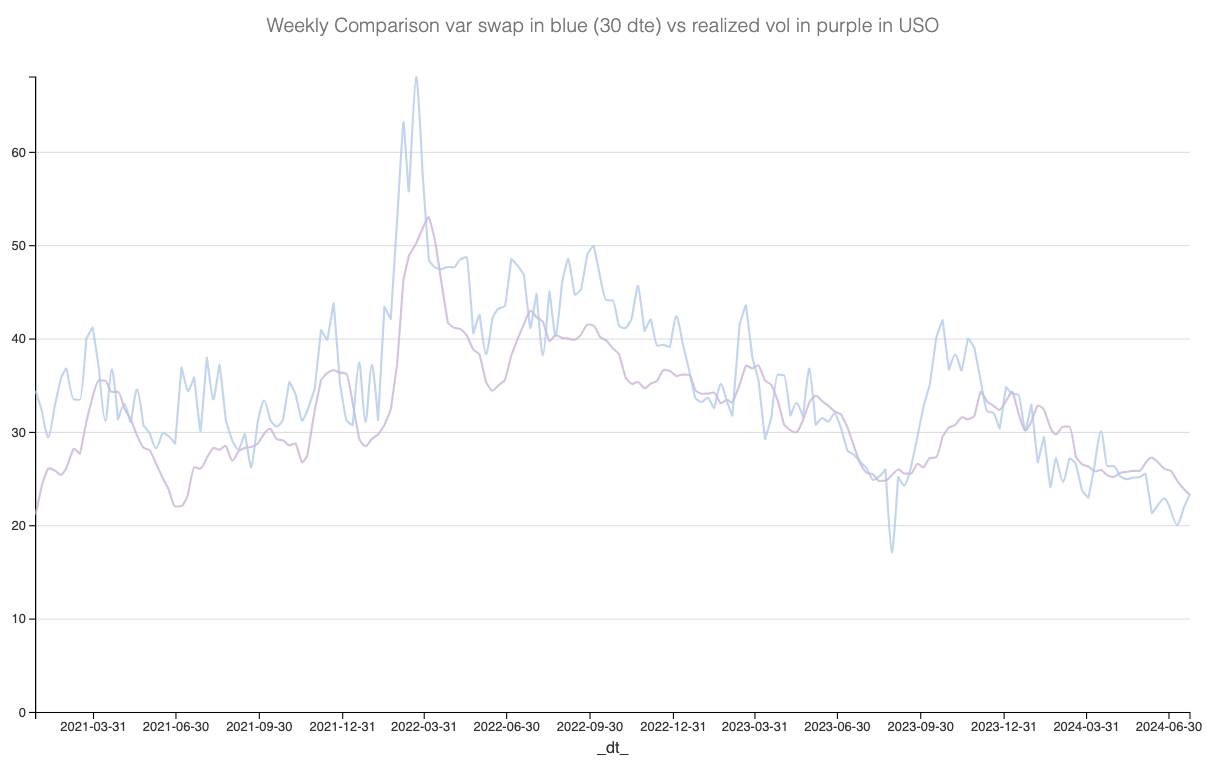

As shown in the chart above, some of these moves were wild, reacting to unfolding geopolitical events. Consequently, the realized volatility in the product remained elevated for most of this period but has enjoyed a steady decline in 2024 despite the ongoing tensions between Israel and Iran.

With realized volatility just below 25%, we are at the lowest levels observed in the past two years. Does this mean nothing will happen? Absolutely not. Geopolitical tensions can arise anytime, and the market is aware of this. We suspect that a premium embedded in option prices may be overestimating the current state of the market.

Let’s take a closer look.

The data and the trade methodology

First, let's examine how option prices in USO have evolved and compare them to realized volatility.