Signal du Jour - Short Vol in US Equities

Realized volatility is in backwardation therefore...

With most of the earnings season behind us, equity markets continue to cling to their upward trajectory. Just last week, NVDA's impressive earnings reports propelled the NASDAQ to new all-time highs, while the VIX concluded the week below 14 for the 14th time in the last 15.

So, when will the tide turn? We can't say for sure and aren't interested in this type of forecasting. Instead, we’d rather embrace the current sentiment in the marketplace.

Despite lingering uncertainties surrounding monetary policy and upcoming elections, nothing currently suggests a need for alarm. Therefore, let's make the most of this period of low volatility. Today, we're eyeing short volatility strategies in SPY and IWM. And why steer clear of QQQ? Given the recent surge in semiconductor stocks, it wouldn't shock us to see the index drift even higher, and as usual, we’d like to avoid delta-hedging.

Let's have a look.

The context

Since the Federal Reserve signaled that interest rates have peaked, hinting at potential rate cuts in 2024, US equity markets have embarked on a bull run, eliciting a blend of wonder and skepticism among many observers.

Yet, we won’t deny the looming challenges on the horizon. Inflation remains stubbornly high, companies grapple with the impact of elevated interest rates, and the specter of a banking or real estate crisis continues to hang over the US economy.

The political landscape adds another layer of concern. Numerous commentators question the current market optimism with a potentially turbulent election on the calendar for later this year.

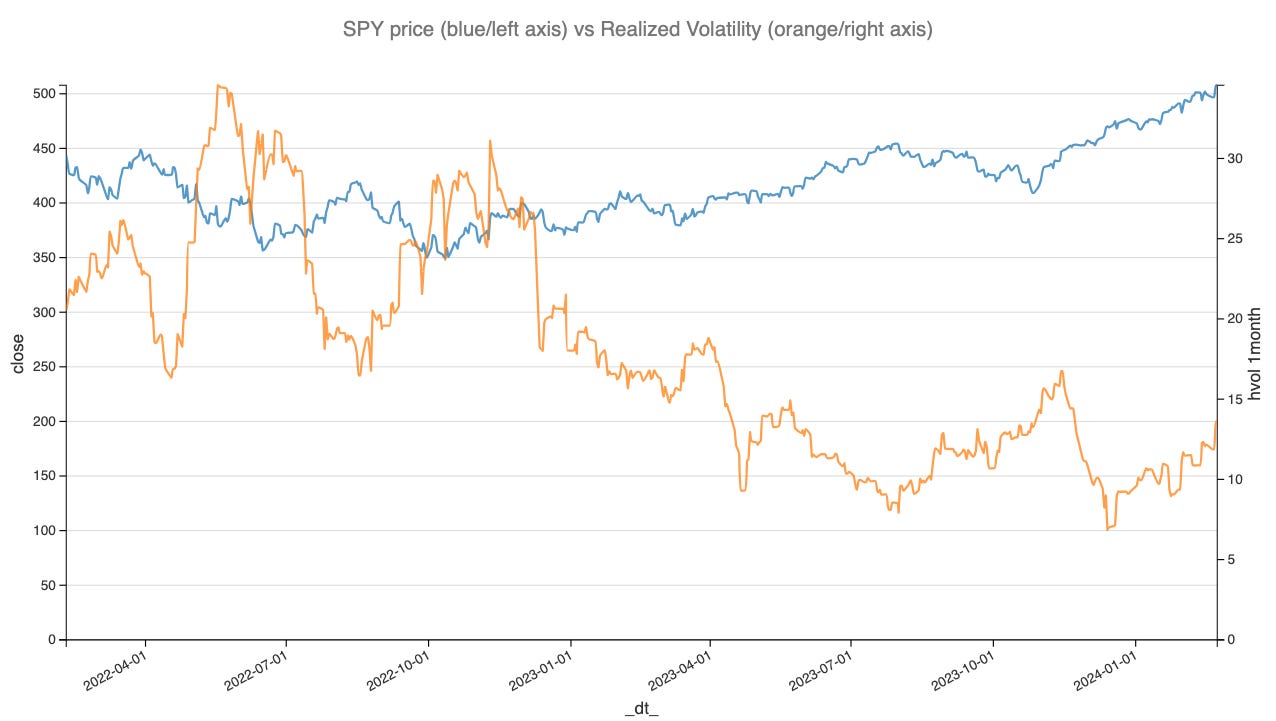

We'll refrain from adding yet another opinion to the brouhaha. However, it's worth noting that amidst the bull run, realized volatility dipped to two-year lows, averaging around 10 for most of January. It began inching up during the earnings season and "peaked" at 13.6 last week alongside NVDA's earnings report.

At a VIX of 14, it becomes apparent that selling volatility doesn't offer a substantial margin for error.

It's crucial to shift our focus to realized volatility and try to understand if it is likely to keep expanding or, as the market seems to be anticipating it, it is likely to revert.

Let's dive into the data.