The election is getting closer, and the tension on social media is palpable. We’ve come across countless posts predicting an ultimate crash following Tuesday’s pullback. But by Wednesday, those losses were methodically erased, and as we write this note, futures are back near all-time highs. Does that mean it’s time to go all-in on the long side? You know us—we wouldn’t recommend that. However, keep an eye on the VIX. It’s sliding—dipping below 20 one hour, then ticking back up slightly—but overall, there are no major signs of immediate trouble. The same goes for realized volatility: there can’t be a crash without a volatility spike, and so far, we haven’t seen one. Let’s see how things evolve as we head into the end of the week.

In the meantime, today, we’re diving into a niche ETF—TAN, which gives exposure to the solar sector.

Let’s take a look.

TAN never recovered from the COVID craze.

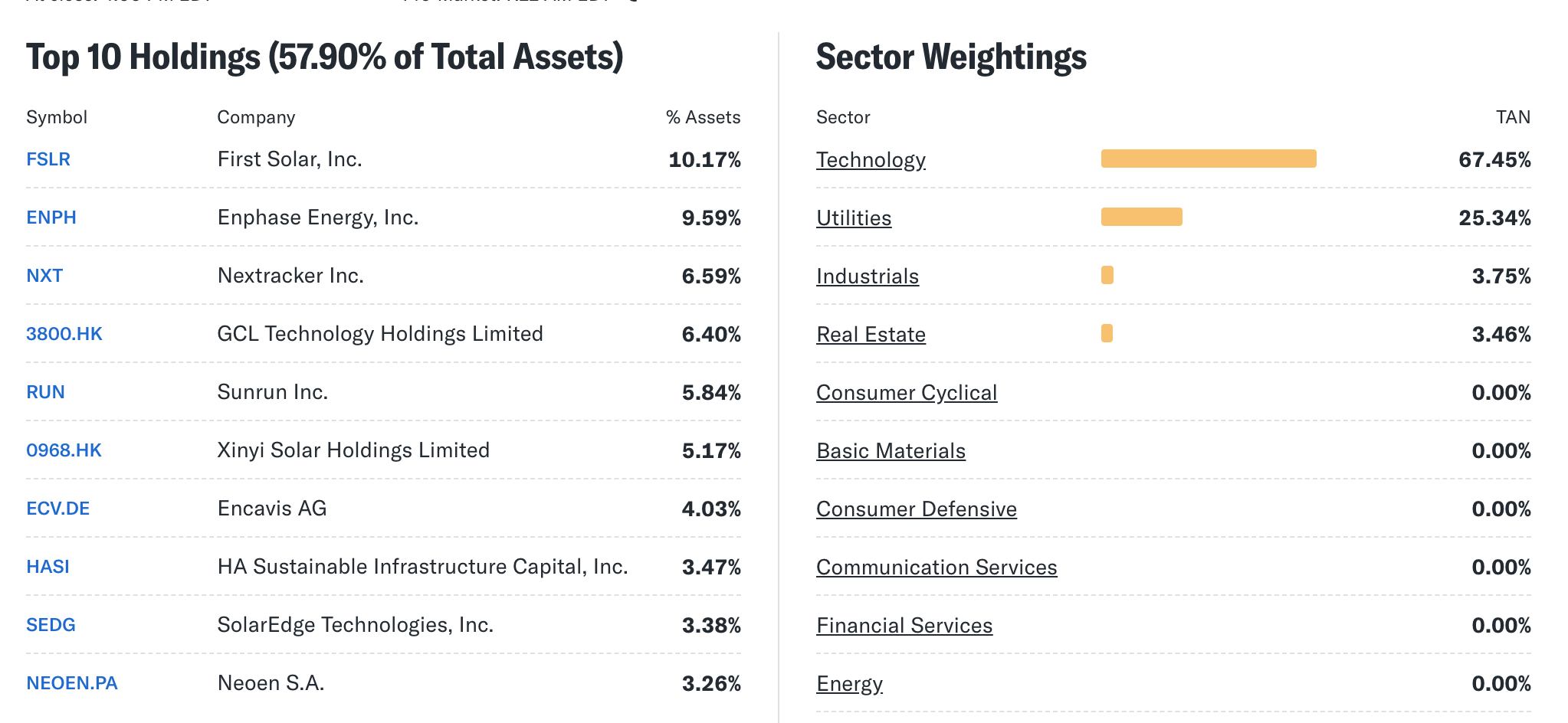

But what exactly makes up TAN? First, TAN invests in companies globally, not just in the US. Second, it’s quite concentrated—10 names make up about 58% of the portfolio, with FSLR alone accounting for 10% of the fund.

Why does this matter? It’s earnings season, and knowing which individual names could move the index is crucial. FSLR’s earnings are due in 12 days, on October 29.

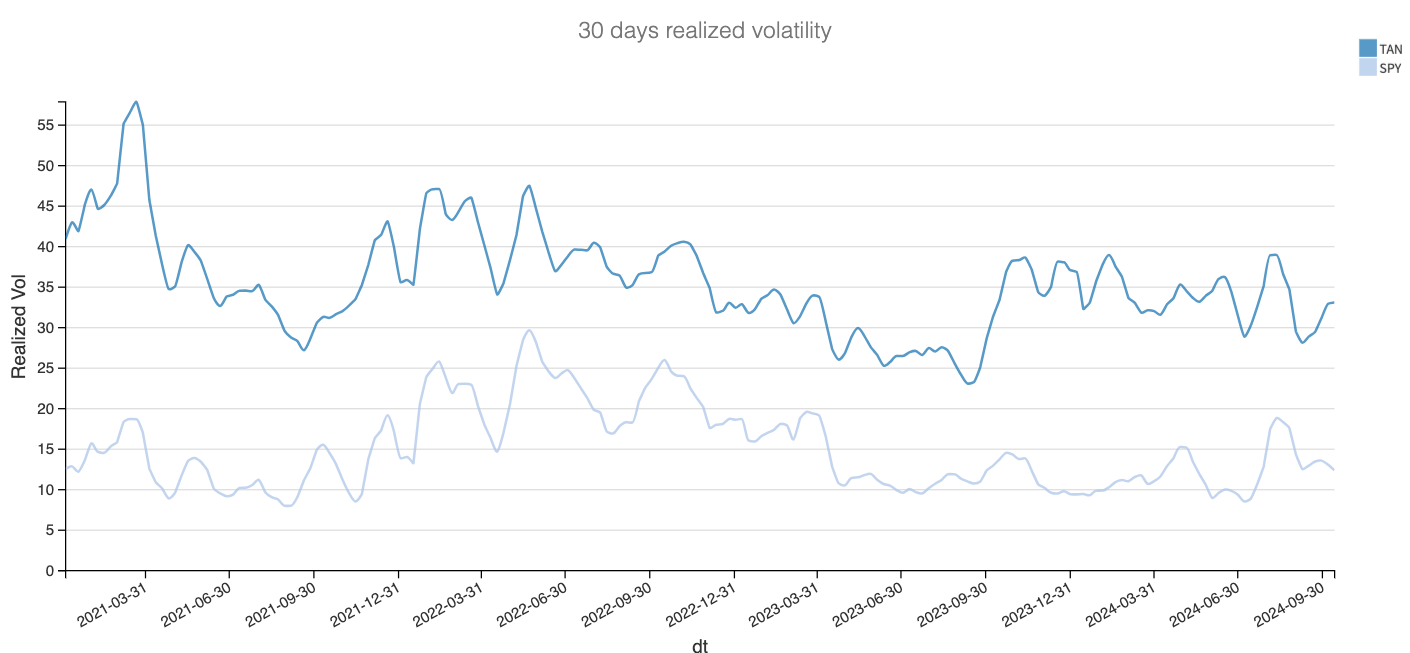

From a realized volatility standpoint, TAN is far more volatile than your typical blue-chip index like the SP500.

Since 2020, TAN has averaged around 30% realized volatility—twice as much as the SPY. So far in 2024, volatility has been range-bound between 28% and 38%. Barring any major events in the coming weeks, we forecast realized volatility to stay within this range.

With that context, let’s dive into the options data and explore how to structure a trade in this product.

The data and the trade methodology

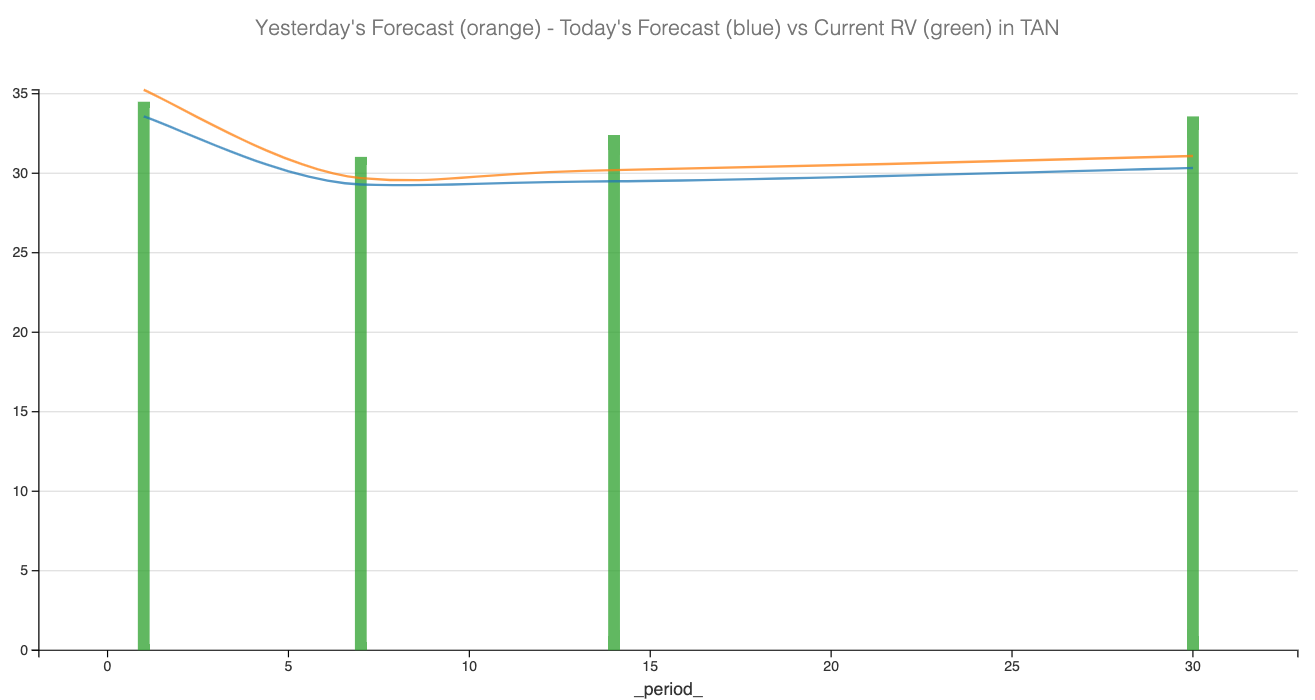

Let’s start by analyzing the variance risk premium (VRP), which is the difference between realized and implied volatility in TAN. We will focus on options expiring in 30 days.