Signal du Jour - short vol in TAN

A calculated volatility trade ahead of key earnings.

Last week was quite turbulent for the equity markets. While we argued yesterday that this agitation was here to stay, President Biden announced he is resigning from the election and endorsing VP Harris as his successor. So far, the market reaction has been pretty muted; the futures are slightly up, and we will monitor further developments throughout the day.

That said, with higher volatility in the market, more opportunities arise, making the life of volatility sellers a tad simpler: the variance risk premium appears stretched in a few interesting areas, and today, we present a trade on the ETF TAN, which gives investors exposure to the global solar industry.

Let’s have a look.

The context

You can find ETFs on pretty much everything, and if you are convinced an industry will do well, you can now find the correct ETF and bet on it rather than engage in tedious stock picking. However, banking on the global solar industry as a byproduct of the environmental transition in Western countries hasn’t delivered on its promises: TAN is down 20% in 2024 and about 40% from a year ago.

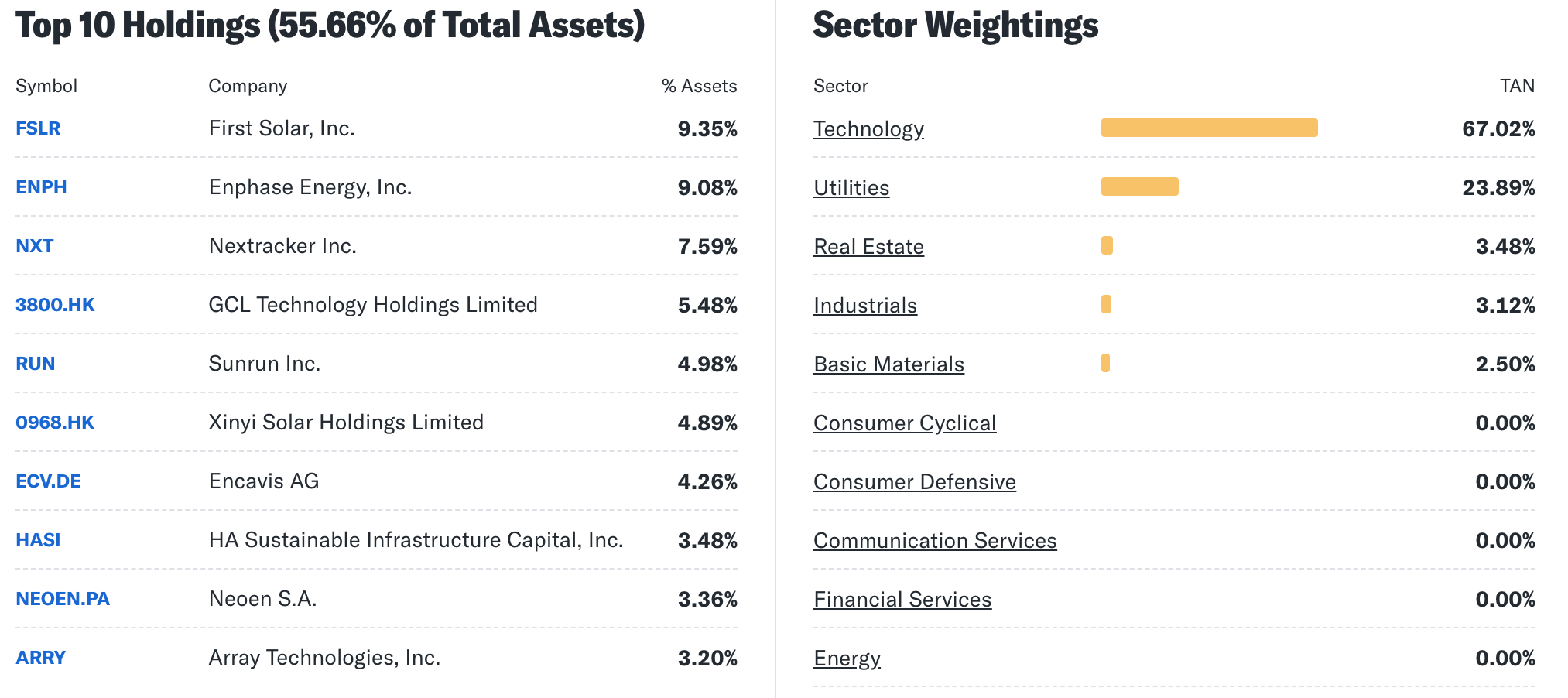

But what is in TAN in the first place? At first glance, an analysis of its holdings reveals a fairly concentrated ETF—18% of its holdings are in just two names—on companies that do not have the same guarantee of profitability and maturity as the classic blue chips. We also see a fair amount of exposure to some Chinese names like GCL and Xinyi.

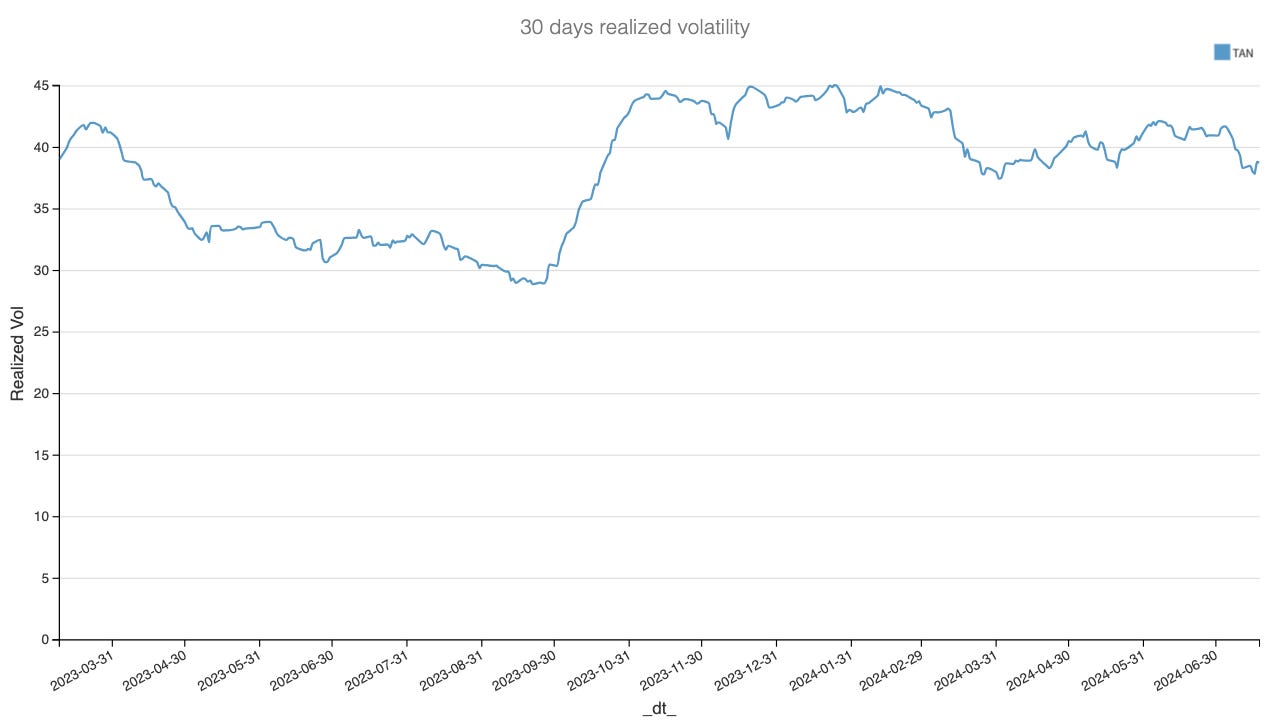

Now that we understand the constituents better, let’s focus on its volatility. As you would expect, the realized volatility is higher than what you would see in baskets composed of more established companies; however, it is fairly consistent at around 40%.

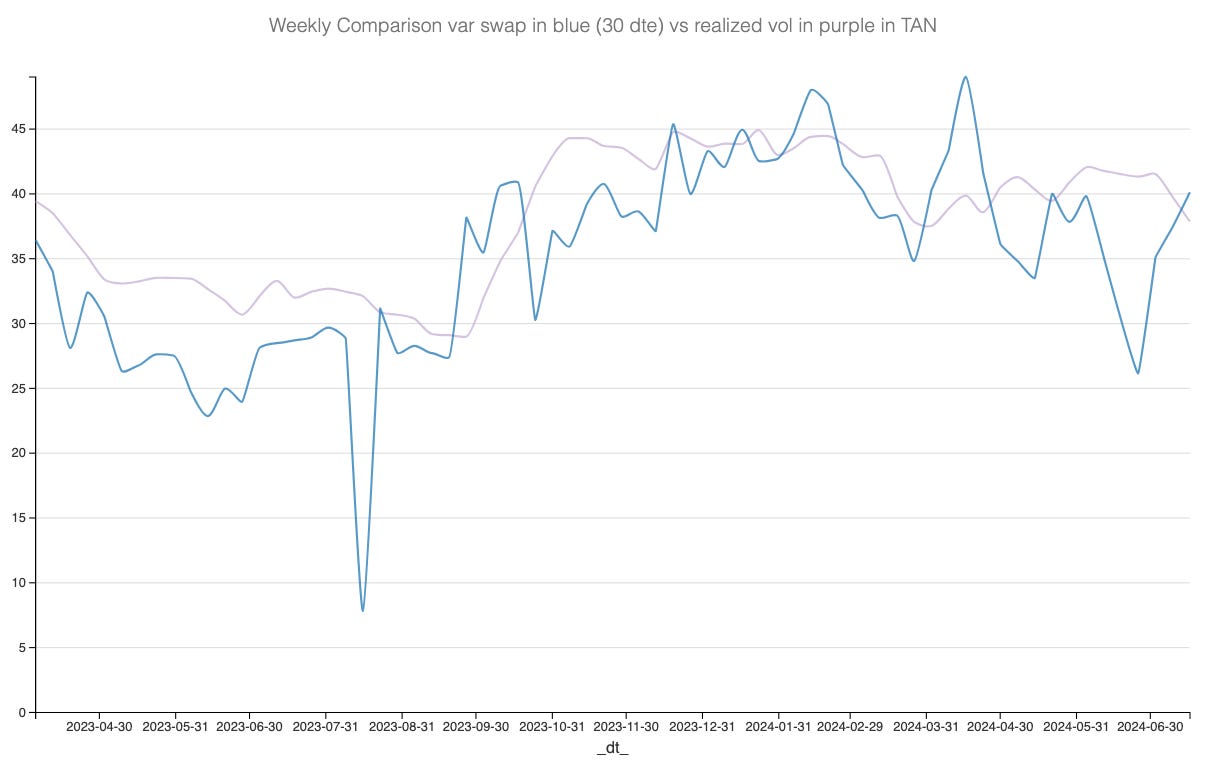

To recap, this ETF has some risks but is somewhat predictable and “stable.” Let’s now focus on options data to see how well we could be compensated to act as an insurance provider.

The data and the trade methodology

Let’s start by getting a feel for the variance risk premium in TAN. For that, we will compare the realized volatility to a measure of implied volatility using the options prices at 30 days.