Signal Du Jour - Short Vol in SMH

Getting closer to the gamma risk zone.

Another FOMC press conference, another non-reaction from the market. It’s not that we didn’t learn anything new; it’s just that nobody seems to care. The market either isn’t paying attention or prefers to kick the can down the road. So, December it is then, to see whether we get another 25-bp cut or not.

In the meantime, equities are back at all-time highs and the VIX remains firmly in the can’t-be-bothered zone. Why would it be otherwise? Trump and Xi apparently had “an amazing meeting” and “a great relationship,” while tech earnings, though reigniting talk of another AI spending spree, didn’t really disappoint.

These conditions feel almost eerie, and for anyone trying to trade volatility, they’re not great. The VRP is positive enough to make long vol bets counterproductive, but not wide enough to justify selling it aggressively either. So what’s left? Usually, getting closer to expiration cycles to find short-term opportunities and… higher gamma risk.

Let’s have a look.

The context

SMH has had a terrific year and is up 100% since the lows of April. Easy to see in hindsight, sure, but still an astonishing run considering how much bashing semiconductors have taken on social media, and the steady dose of skepticism in traditional financial media and among investors.

We’re not here to dispute any of those arguments. But it’s worth reminding the obvious: sometimes, you have to tune out the so-called smart analysis preaching doom and gloom and focus on the opportunity ahead, even when it looks expensive. That’s exactly what professional investors have done. And headlines like “AMZN to cut corporate jobs to integrate more AI” only reinforce the justification for these valuations, not weaken it. We’ll close that parenthesis.

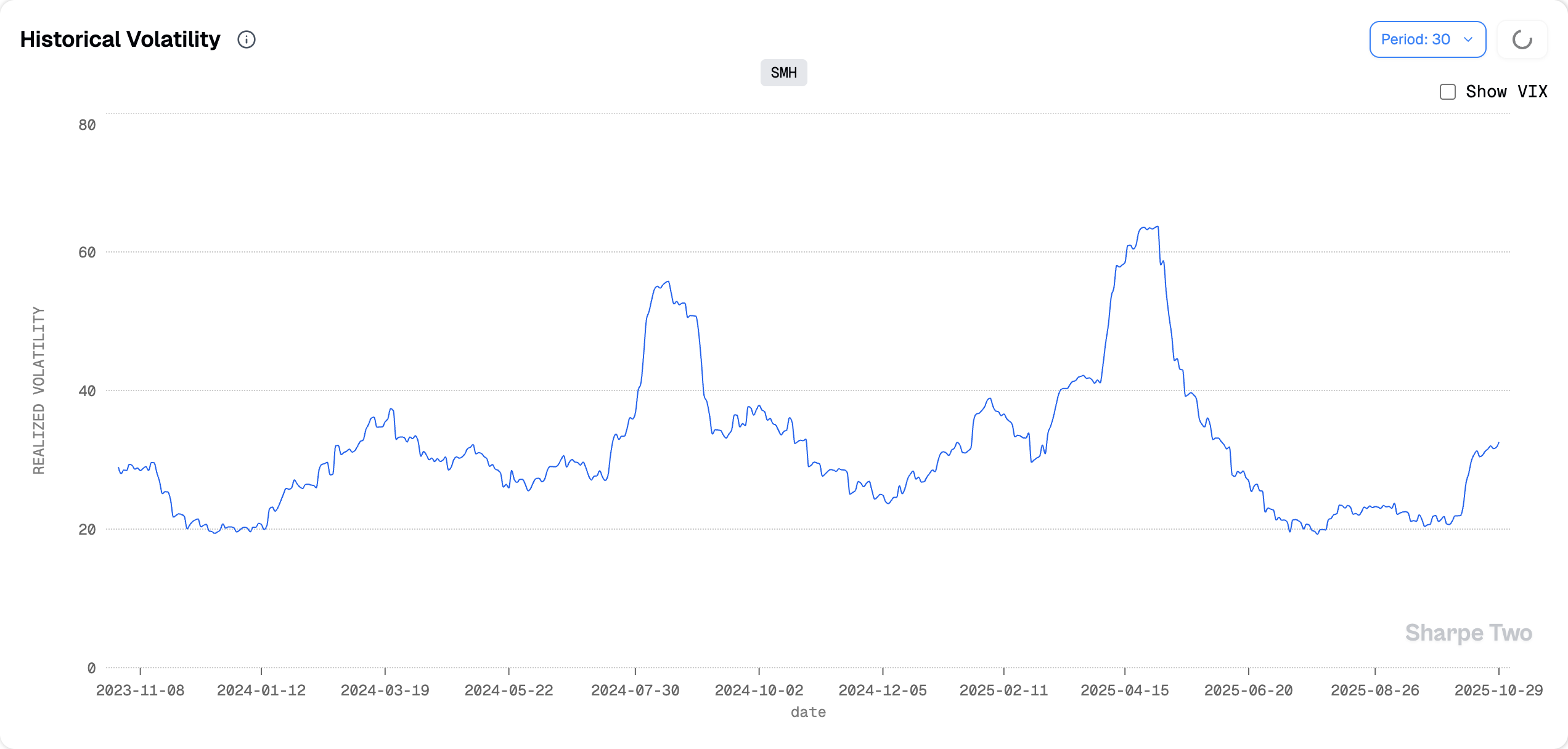

From a realized volatility standpoint, things have been remarkably calm through the summer and pinned near a two-year low around 20% annualized, before gradually ticking higher through October.

We’re now trading around a more normal 32% and roughly what we’ve been accustomed to seeing in SMH when things aren’t in hyper-stress territory. Could volatility keep rising from here? Absolutely. We’re in the thick of earnings season, and partnership announcements between major semiconductor players are flying left and right, the same wave that just propelled NVDA to become the first $5 trillion company ever.

That said, if we set that risk aside, the data tell a different story for now.

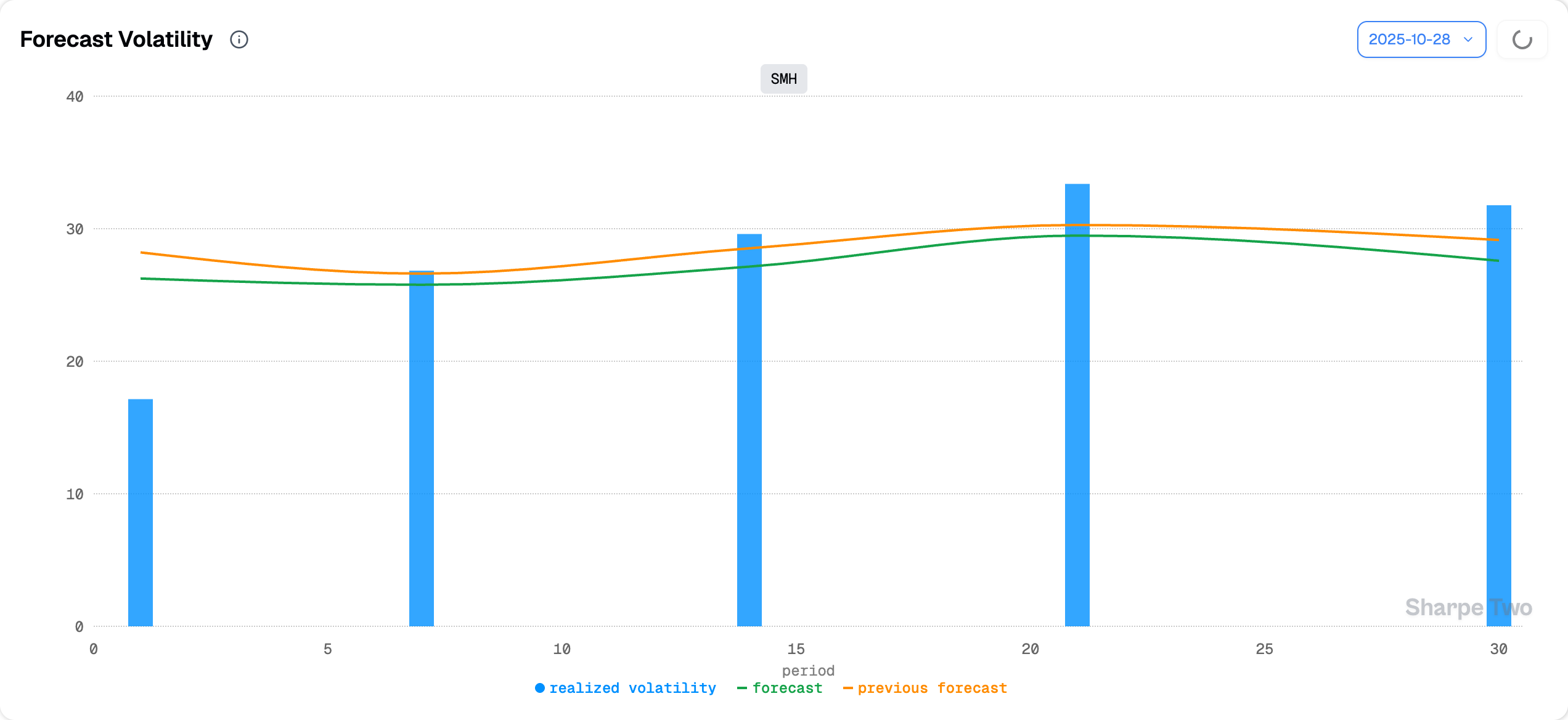

We expect things to cool off a bit, gradually returning below the 30% level and particularly in the short term, where weekly realized volatility could drift closer to 25%.

We’ll insist on this: the shorter the time frame, the harder the prediction. Any headline can trigger a volatility spike that won’t benefit from the same smoothing effect seen over longer horizons. But with that, often comes richer premium.

Let’s see if the odds are on our side to make the most of it.