Signal du Jour - Short vol in KRE

A strong signal before the macroeconomic shenanigans.

We are about one week away from the last main event of the quarter: a combination of inflation data and an FOMC meeting on the same day. With that in mind, some of our indicators detect that the volatility in the bond space is starting to get a bit expensive. We debated discussing that today, but we’ve decided against it. The volatility will likely keep rising as we get closer to the event, and we may revisit this signal early next week.

In the meantime, today, we look into KRE, the regional banking ETF. Last year's crisis is still fresh in everyone's memory, although it’s been a long time since we read an analysis about how imminent a crisis in the sector was.

Yet, the price of insurance has been on the rise.

Let’s take a look.

The Context

Although the movement in KRE has been fairly tame in 2024 so far, investors are still very much rattled by the potential impact of current monetary policies on regional banks. Who can sustain this “higher for longer” macroeconomic environment, and who can’t? We don’t have the answer to this question. Instead, we will spend some time reviewing how the cost of insurance over the past year has performed versus the real risk in the underlying.

Let’s start by looking at the realized volatility for KRE.

We can observe the last market event in March 2023, when realized volatility peaked. When we compare it to the realized volatility in SPY and XLF (the ETF-tracking financial companies), we see that there’s been a significant degree of agitation in KRE compared to the other two. Although things are converging, we are still solidly realizing 20 in realized volatility while the other two are in the low 10s.

This impression of calm is reinforced by the term structure for realized volatility.

The level of realized volatility is the lowest overall this year, even lower than what we saw in January 2024, when things are traditionally quieter. The dark blue line represents what happened in March 2023. For things to get that bad again, we would need some seriously concerning headlines, going far beyond whatever will happen pre- or post-FOMC meeting.

All of this is to say that, once again, we are in a very different regime from last year. This doesn’t mean that risks don’t exist but are not as pronounced.

Now, Let’s dig into the option data to understand how to structure a trade.

The Data and the Trade Methodology

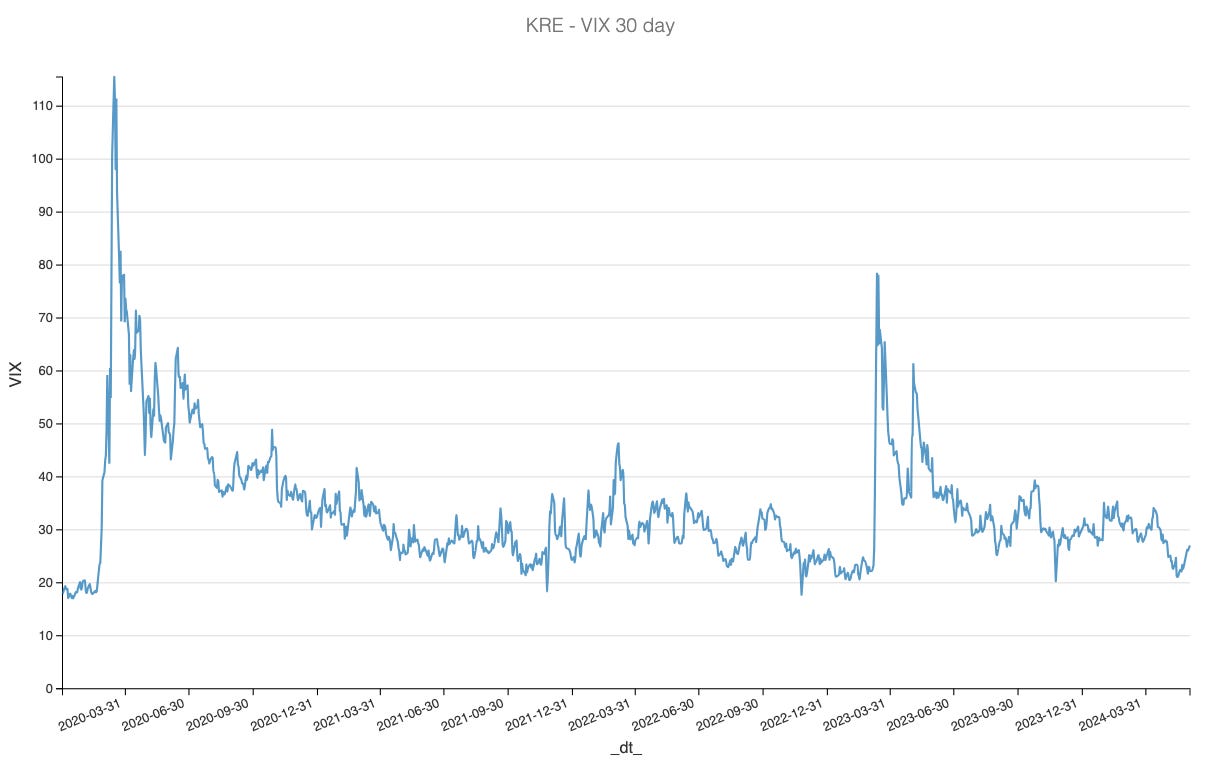

Let’s begin with a reconstruction of the VIX index for KRE.

Interestingly enough, although we are far from the highs observed during significant market distress, the current level of volatility is fairly normal. Currently sitting at around 27, we have rebounded from the low observed a few weeks back. Is this a sign that traders are gearing up for the FOMC next week? Let’s take a look at the term structure.