To be honest, we were considering writing about a long-tail signal instead. The FOMC presser, while informative, didn’t spark the expected bout of volatility. As usual, the market was quick to sell the expensive options it had loaded up on—just in case the world stopped turning Thursday morning. And with VIX back below 20 while 30-day realized volatility sits at 19, and nothing suggesting the next headline will be kind to equities… well, you can do the math.

But instead, we’re focusing on yet another short-vol signal. Because while equities have been swinging from left to right, there’s one asset class that has been eerily muted so far in Q1: bonds. Despite the Fed’s growth forecasts yesterday, price action remains subdued. And if recession chatter is picking up and economic growth is slowing, shouldn’t the corporate bond sector be feeling a little more pressure?

Today, we’re diving into HYG, the ETF that tracks high-yield corporate bonds. Let’s take a look.

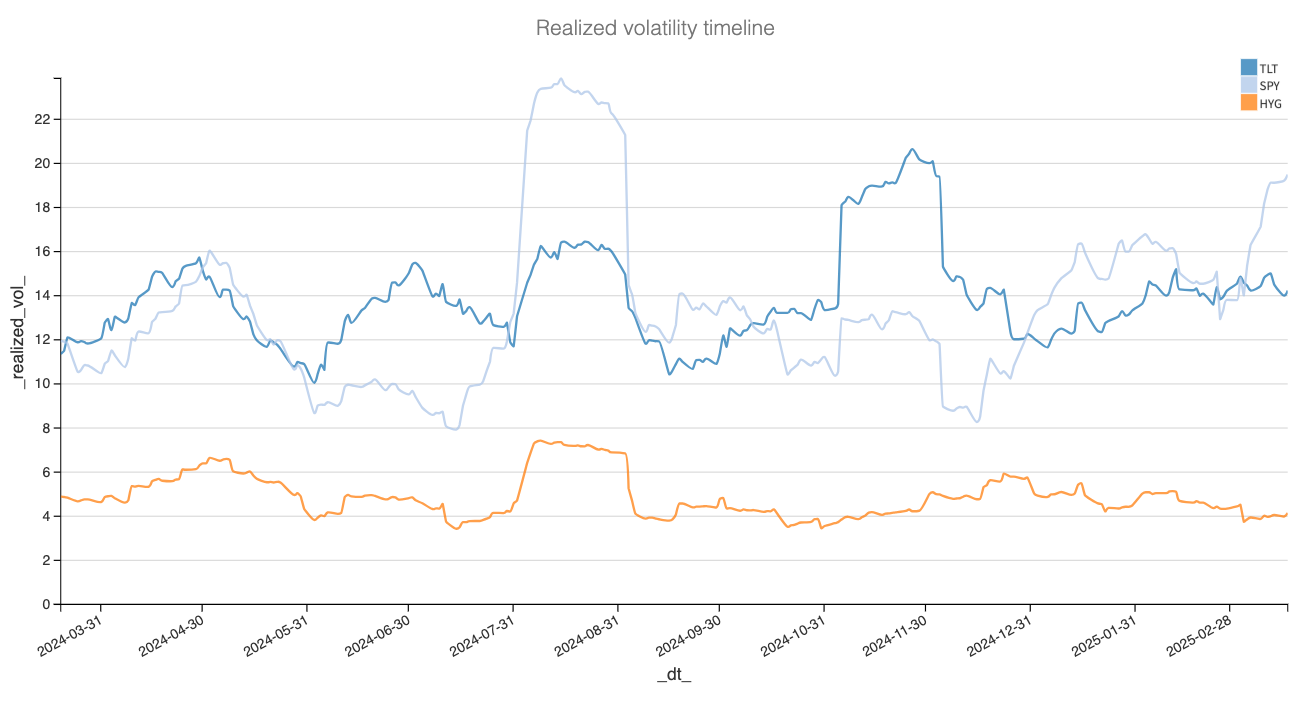

While the famous bond-equity inverse correlation made a comeback in 2024, it’s clear that the diversification hedge hasn’t worked quite as expected during the Trump 2.0 debacle. Sure, rates are slightly lower in 2025 (since bond prices move inversely to yields), but overall, they’ve been holding steady.

Even more striking is what’s happening in high-yield corporate bonds. You’d expect that with equities swinging up and down (but mostly down lately), we’d see some real stress in credit markets. But that’s just not the case—at least not yet.

Realized volatility-wise, the contrast is even more striking—every equity shock in 2024 was mirrored by a move in bonds, but not in 2025, where things have been pretty quiet. So quiet, in fact, that in the case of HYG, this might be one of the calmest periods in the bond sector over the past few years. We’re not bond experts, but that does come as a bit of a surprise given all the chatter about a potential recession, slow growth, and the impact of tariffs on corporate balance sheets.

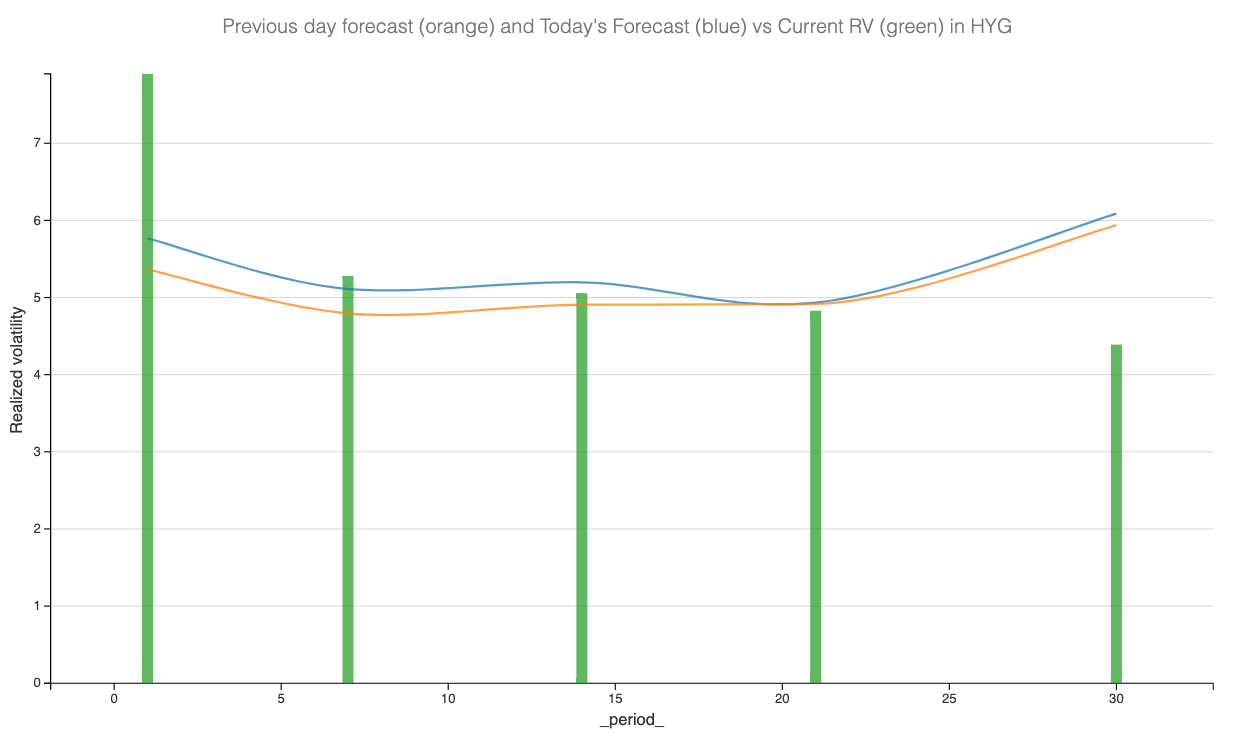

From a forecast perspective, no surprises here—we expect things to stay roughly where they are, oscillating between 4% and 5% annualized realized volatility.

That said, while these models are great for direction, in a market where the next headline can trigger an outsized and unexpected reaction, they should serve as guidelines rather than hard rules.

Now, despite all this quiet, let’s check the options market and see how we can structure a trade—assuming things stay as stable as they are right now.