Signal du Jour - short vol in DIA

The truth is in the straddle prices.

Wasn't it nice to have a weekend without worrying about retaliations between Iran and Israel? Everything was calm from a headline perspective, and judging by oil prices this morning, if you had sold some straddles on oil, betting that prices were still inflated after weeks of tensions, you'd be having a pleasant Monday morning.

Unless you're trading oil in yen, that is. Speaking of interventions, the BOJ has finally decided to use some of its reserves to combat the multi-decade lows observed in the yen. We must admit that we're a little frustrated. In the Discord Pre-market call yesterday, we discussed going long on straddles in FXY, thinking they were cheap, considering the likelihood of a violent upward movement. With the intervention behind us, implied volatility must have increased, and that opportunity has now passed.

So, what's left this Monday morning before the FOMC on Wednesday and the Non-Farm Payroll report on Friday? We'll look into DIA, where realized volatility has been fairly contained. But isn't that risky, considering the upcoming main events? Of course, it is. That's the service we provide to the marketplace. No free lunch, remember? Especially not on a Monday morning.

Let's get to it.

The context

We shifted to a different volatility regime earlier this month, which was largely driven by the recurring geopolitical tensions. However, while these tensions were the main source of alarming headlines, the Fed has quietly begun its communication exercise to warn market participants about the likelihood of a rate cut in June. Well, the odds have melted like butter on a warm, sunny day in Mexico City, as inflation has been quite sticky for the past few months.

These two factors have led to an increase in realized volatility throughout April, following months of euphoria and calm in the equity markets.

Now, with two major events on the horizon, one might argue that realized volatility in DIA has the potential to go much higher. This is indeed a real possibility. However, we believe the market knows this and has adjusted options prices accordingly. Once again, if you were an insurance seller and knew significant risks ahead, you wouldn't casually price your policies like before.

Let's take a look at the data.

The data and the trade methodology

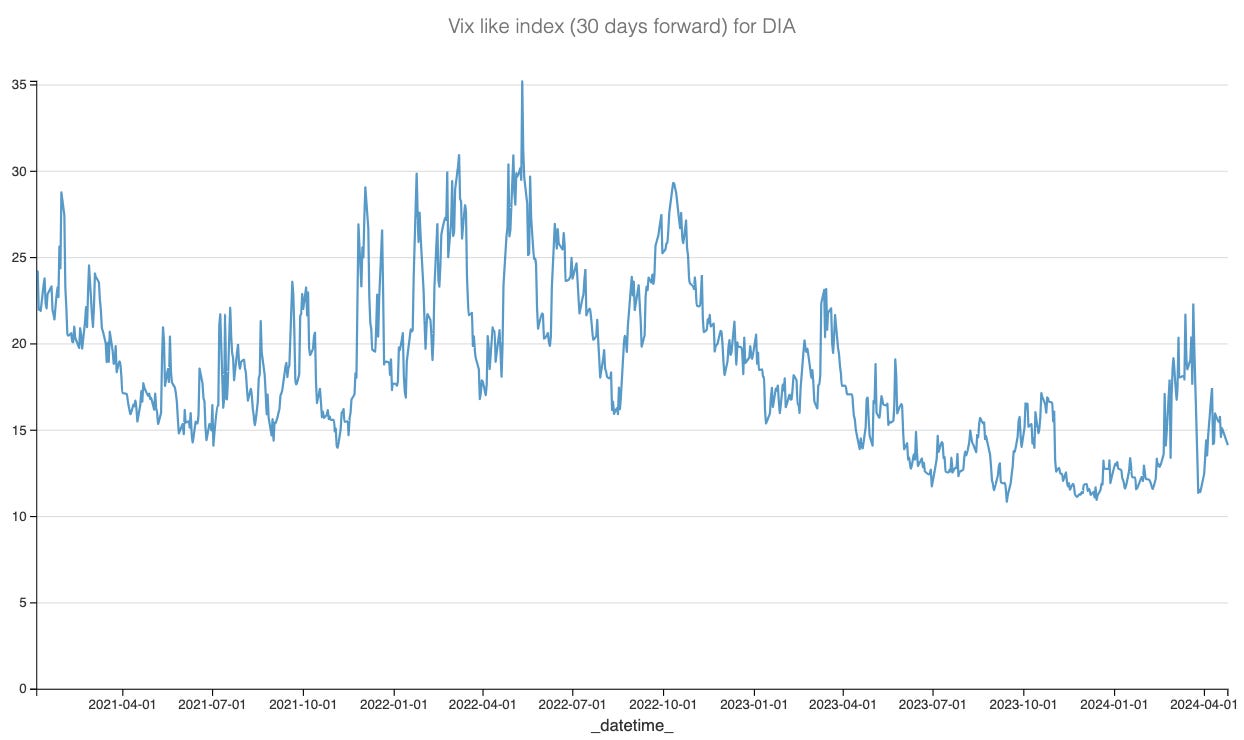

Let's start by examining the reconstruction of the VIX index for DIA.

This has already come down quite a bit from the highs of April, and one could argue that the prices are far less attractive than they were a few weeks ago from a variance risk premium perspective.