Signal Du Jour - Short vol in ASHR

Exploiting the Chinese Risk Premium

NVDA came up with stellar earnings yesterday, yet, the market reaction was muted. The confusion around the AI narrative is great now: on one hand, Saaspocalypse started and the casualties are already plenty, on the other hand the market frowns upon the massive capex investment to satisfy the incoming demand for compute, and to make everything final, the number of commits made by autonomous agents in GitHub repos has grown exponentially since the beginning of the year, signalling broader adoption and … well token consumption. We personally have never seen such a large number of people paying for an advanced AI subscription or let alone API keys. The beginning of a new era? Time will tell.

But in the meantime, we will let the markets deal with their own schizophrenia and focus on China, which is also leading the charge and competing head-to-head with the US in the AI race. We will be very curious about what comes out of the conversation between Xi and Trump at the end of March, and while we are certain that the situation in Taiwan will get most of the coverage, access to raw materials and advanced chips and compute will also be an important topic of conversation.

That is if the meeting actually happens: Xi has given a stark warning to the US, pushing them to act with “prudence” on the question of arms deliveries to Taiwan, ahead of the meeting. That is enough uncertainty for us to start seeing some ripple effects in the options market.

Let’s have a look.

The context

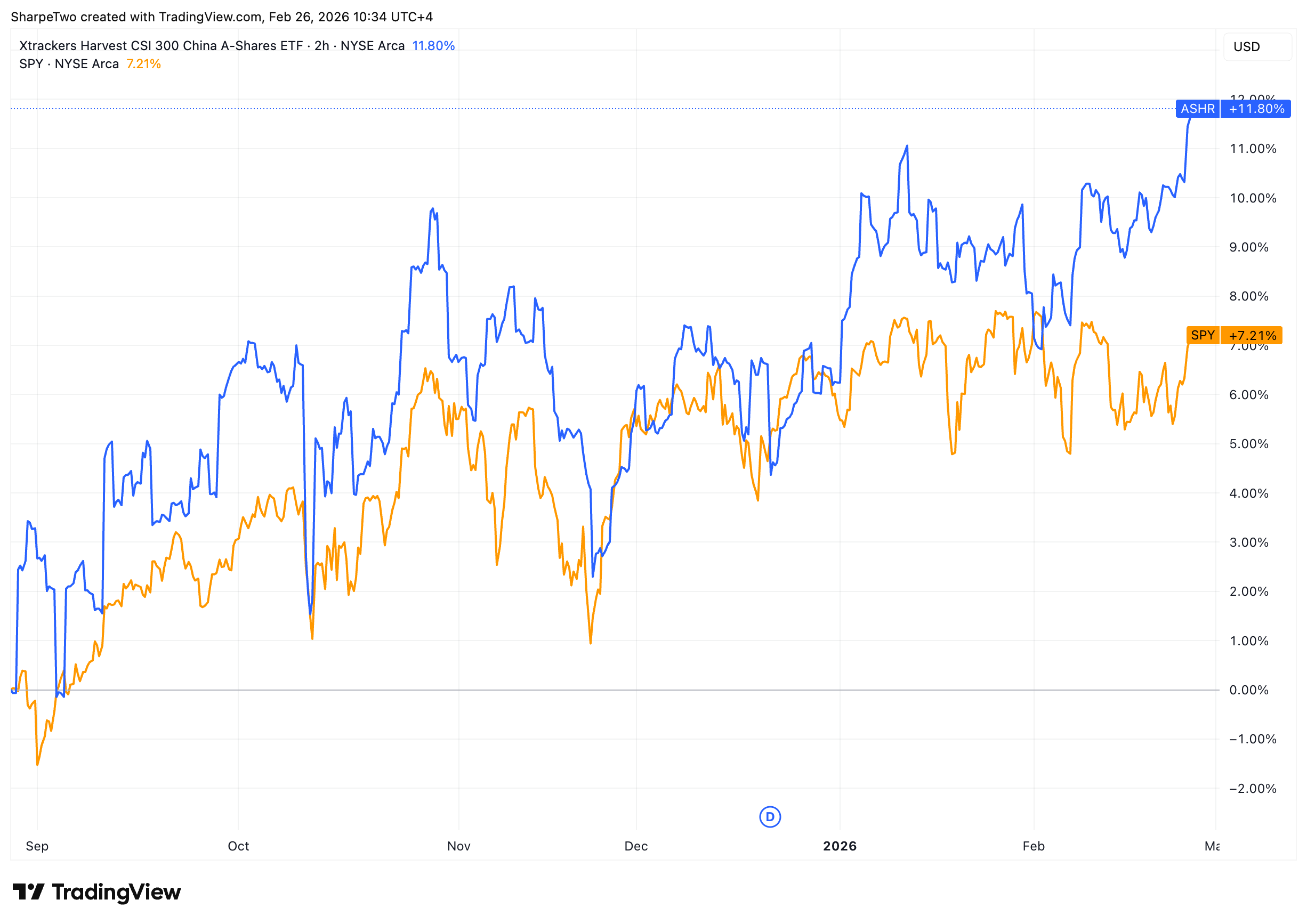

Since the tariffs arm wrestling with the US almost a year ago now, the Chinese stock market has recovered all its losses and while ASHR still trades at a massive discount to the highs observed in spring 2021, it is not unimaginable anymore that the index may get there over the next few years.

Yet, like their American counterparts, performance has been a little flatter over the last six months: still up a solid ten percent but with much more whipsaw than what we’ve been accustomed to in the past. This relative calm translates into one of the lowest levels of realized volatility observed over the last few years.

And while it increased a few points from the lows of 11.5 to almost 13.5 at the moment, nothing screams a potential explosion of risk over the next few weeks. One will have to keep an eye on the geopolitical situation: if the US administration decides to increase the heat ahead of the meeting, you could observe a renewed sense of agitation in ASHR. While this is a possibility, we also do not think it would contradict what our current realized volatility forecast shows.

Expect the risk to keep rising, potentially up to 15; however, you would need a serious new catalyst to go much higher than that. While we usually refrain from any geopolitical comment in our analysis, we will just simply note that October gives a good precedent in how Trump, while willing to trade blows occasionally with his powerful rival, isn’t committed just yet to sustaining an escalation.

With this in mind, let’s go have a look at the options market to see how we could structure a trade in the product.