Signal du Jour - short vol in ASHR

Introducing the Chinese Risk Premium

41.

That’s the number of times the S&P 500 has hit new all-time highs this year. Whether you’re concerned about the state of the economy, the upcoming election, or global tensions, the markets have decided that none of this is enough to curb their excitement.

We’ll see if the US GDP brings back more concerns about growth and potentially stirs up some volatility.

While we wait, today, we turn our eyes to China and, more specifically, to ASHR. This is partly because the author of this newsletter was there briefly last week but mainly because we like to present great opportunities to our community, and we bet you will like that one.

Let’s dive in.

The context

When you land in mainland China, the contrast with the West isn’t as stark as you might expect: perfect eight-lane highways, a plethora of electric vehicles, towering skyscrapers, and, of course, an all-encompassing digital life seamlessly integrated into a couple of apps (Alipay and WeChat). It’s impressively convenient, though it raises concerns about how all that data is being used—but that’s a topic for another day.

A few conversations with locals, however, reveal more than a Financial Times headline ever could: “It’s harder to get a job. The economy hasn’t bounced back to where it was before the pandemic. We have to save more money because tough times are ahead.”

The day after we left the country, the government announced a series of stimulus measures on a scale not seen since the Great Financial Crisis. The market, awakened by the idea of cheap liquidity, surged in what had been, until then, a rather bleak Year of the Tiger.

In just two weeks, FXI, the go-to ETF for Chinese equities, shot up by 20%. It climbed back to its highest levels of the year. ASHR, which is composed solely of top-tier Chinese stocks, went from negative territory to nearly 7% gains. What exactly is in ASHR? Let’s take a look.

These companies are household names in mainland China, with the ETF heavily weighted toward financial services, industrials, and technology—the backbone of the Chinese economy.

With such a rapid move to the upside, the seven-day realized volatility in Chinese-related ETFs has spiked significantly over the past few days.

However, this hasn’t been enough to meaningfully impact the 30-day realized volatility.

It’s true that realized volatility in ASHR has been ticking up throughout Q3, while it has interestingly declined in FXI. Still, we would need extreme market action over the next few days to expect realized volatility to reach the highest levels we’ve observed recently. It’s not impossible, but it’s not what our forecasts indicate.

With all that in mind, let’s examine the reaction in the options markets since the stimulus was announced and see how we could structure a trade in this unusual situation.

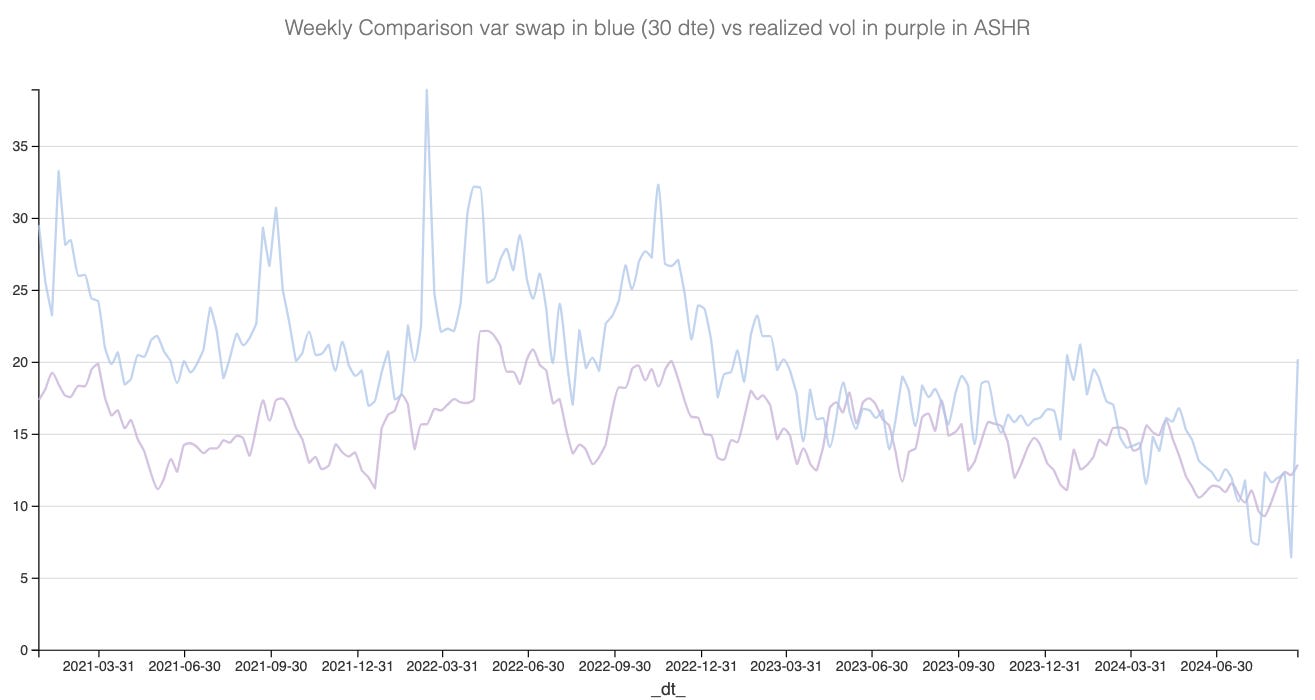

The data and the trade methodology

Let’s start by comparing the realized and implied volatility from options prices, measured at 30 days. This will give us a sense of the VRP (Variance Risk Premium) in ASHR.