Yesterday's equity market faced some turbulence as Fed Chair Jerome Powell quashed hopes for a March rate cut. Interestingly, the VIX remained relatively unfazed.

That's alright, though. The beauty of trading a broad and varied array of ETFs lies in the diverse opportunities that present themselves.

Our focus today shifts to the natural gas sector, specifically through UNG. February has just begun, and despite the potential for further drops in temperature, we anticipate a slowdown in the recent volatility of natural gas prices.

This scenario paves the way for volatility traders, especially those keen on selling insurance premiums in the market.

Let’s take a closer look.

The historical volatility in UNG has gone through the roof this winter.

The recent spike in UNG's price was as rapid in its decline as it was in its ascent, pushing its historical volatility to the highest levels of the year. Currently at an impressive 90%, UNG ranks as one of the most volatile assets on our watch list.

Why does this present a good opportunity? As volatility sellers, we understand that volatility is inherently mean-reverting. After peaking, it's likely that volatility will gradually diminish.

Our focus isn't on predicting the future movements of UNG's price. Rather, we anticipate that option sellers will maintain elevated quotes as a precaution against potential drops in temperature or geopolitical shocks that could affect natural gas prices.

Let's dive into the data to further understand the opportunities this scenario presents.

The data and the trade methodology

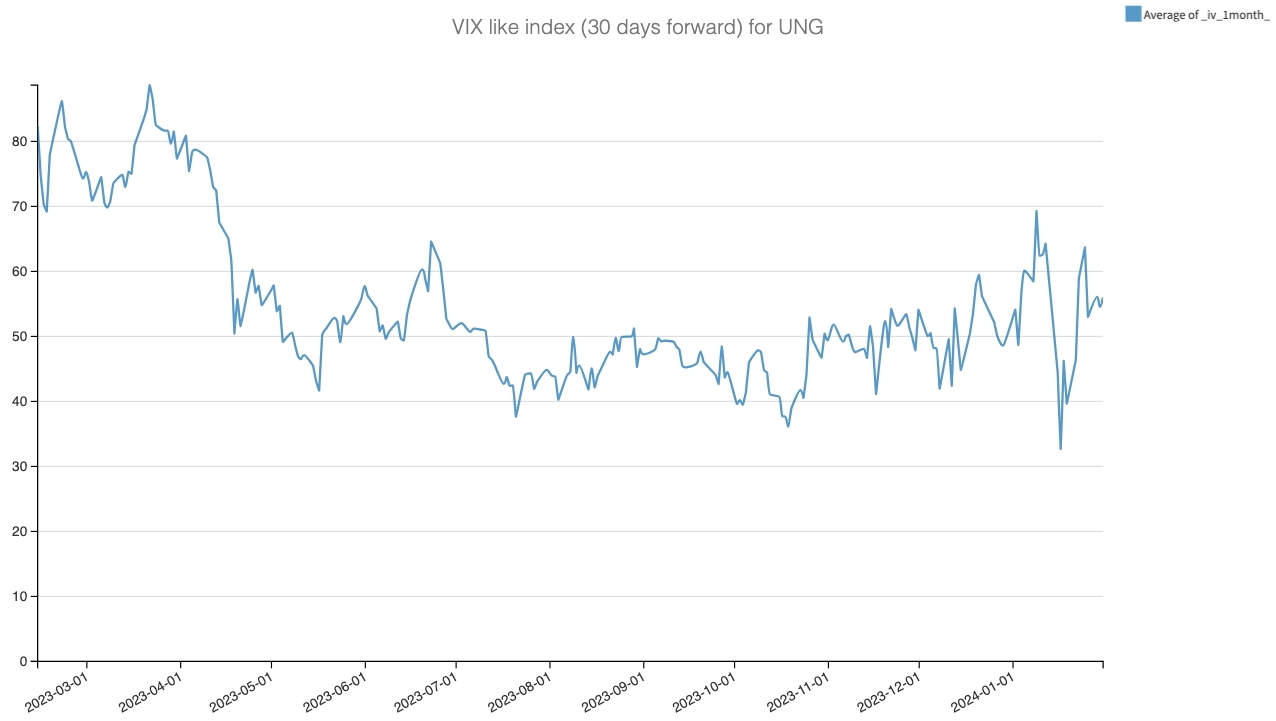

To start our analysis, we applied the CBOE methodology to create a VIX-like index for UNG.

While the index isn't at the extreme highs seen in early January, when Europe was first hit by a cold wave, it remains relatively high. This level of implied volatility suggests the potential for some trading opportunities on the sell side.