Signal Du Jour - Sharpe 1.61 Win Rate 70%

Worked like a charm last week

As expected, the equities market surged yesterday following the Fed's unofficial conclusion of its rate-hiking cycle. Now, the markets are hovering near all-time highs. In the coming days, expect some volatility as fund managers fine-tune their portfolios and get ready to pop the champagne.

One asset that's remained relatively unmoved by this news? Oil. Considering the steep movements we've observed in recent weeks, its calm response is almost surprising.

Remember, last week, we prefaced our short trade in USO by noting that high implied volatility usually signals a reason for caution, and we certainly didn't anticipate a smooth ride.

Given that our indicators are still flashing positive signs, we're introducing a follow-up to the one we initiated last week.

Haven't subscribed yet? Now's the time. We're expecting this one to be another exciting opportunity.

The context

Since the beginning of December, oil markets have continued their surprising descent, leaving many experts scratching their heads.

And despite the ongoing sanctions against Russian exports, production adjustments from Saudi Arabia, and persistent tensions in the Middle East, none of these elements had been enough to fuel a steady climb in oil prices.

Instead, we’ve observed some violent moves up and down as the market participants reacted to the prospect of an economic slowdown in major countries like China and India. Analysts also pointed to the US tapping into their national reserve as a reason why the prices couldn’t sustain their current level.

At Sharpe Two, we steer clear of making broad macroeconomic forecasts. Still, we're keeping a close eye on the market's volatility and assessing whether the current trends in price movements hold ground.

Despite the recent downturn in December, what's clear is that the realized volatility in the oil market hasn't skyrocketed. It's remained relatively stable, hovering near the year's highs. Some could see this as an indication that oil prices have reached their lowest point.

That's a possibility.

However, as volatility traders, our primary interest isn't in pinpointing the exact bottom. Predicting direction is hard, and now, with the Fed appearing increasingly confident about achieving a 'soft landing' in the economy... who can say how oil will react?

Instead, we're more focused on assessing whether the implied volatility in USO is still inflated. Traders may seek protection against a further decline or a sharp rebound.

The Signal and The Trade Methodology

Last week, we prefaced this section with a reminder: just because we're betting on overpriced volatility doesn't guarantee an absence of volatility. Despite the relatively calm week we've just experienced, it's crucial to reemphasize that point. Our ideal scenario is a market that behaves predictably, but what we're really banking on is that the actual movements in the underlying assets won't surpass the cost of the At-The-Money (ATM) straddles.

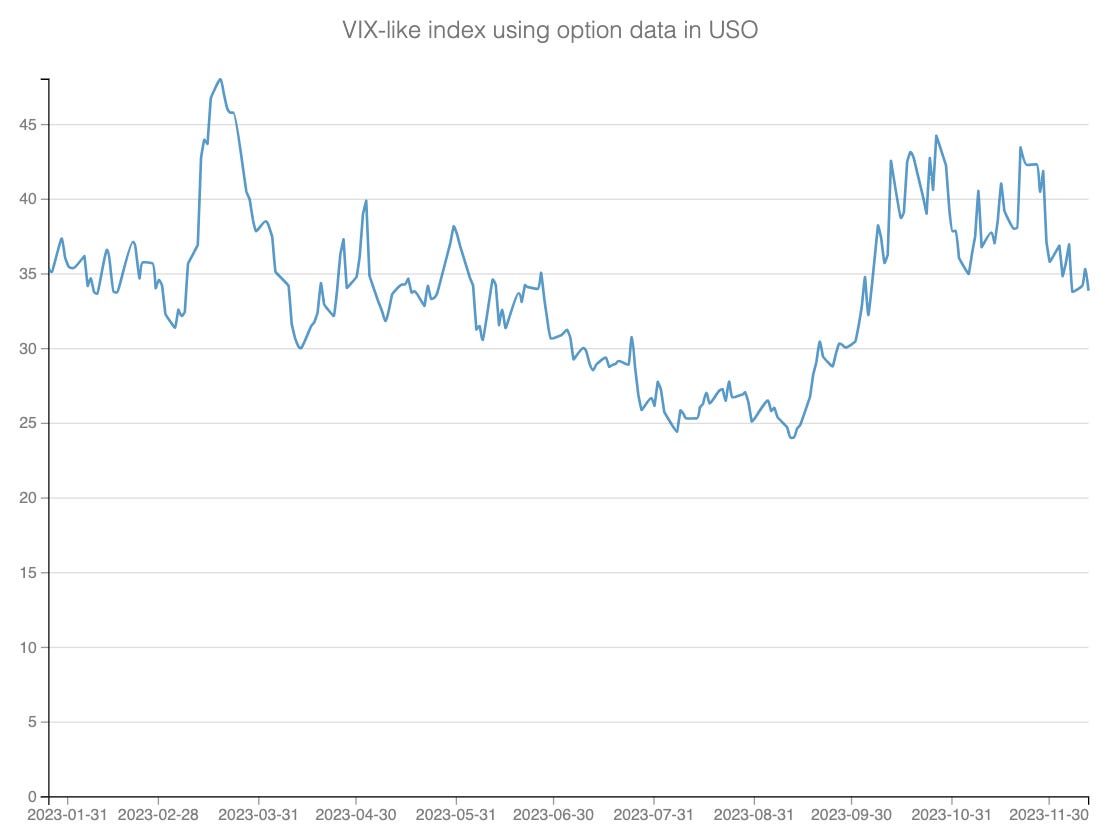

The graph we're looking at reconstructs the VIX for USO using data from options with 30 days to expiration. While we're not at the year's peak levels, the volatility is still notably high. This indicates that the market expects some movement in the next 30 days – a key factor to consider when discussing trade sizing.