Signal du Jour - Long Vol EWX

A bit of long Vega never killed no short-vol trader.

Yesterday, we proposed a short volatility trade in EWH. We were banking on expensive straddle prices and a stretched variance risk premium. Adding that Chinese New Year is just around the corner, we thought it had the characteristics of a solid opportunity.

But who knows? Whoever trades volatility knows that success often hinges on playing the numbers game. And sometimes, that means hedging our bets.

Here at Sharpe Two, we recognize the benefits of short volatility positions. However, we're not hesitant to explore long volatility opportunities when they arise, especially if they help balance our overall vega exposure. Today, we're looking at a potential long volatility trade in EWX, an ETF that tracks small-cap companies in emerging markets.

Let's take a closer look.

The context

Small caps in emerging markets? For many investors, these are no-go zones, often perceived as too risky to even consider.

The inherent riskiness of small caps, particularly in emerging markets, means they're highly sensitive to global economic shifts. They often exhibit exaggerated reactions, both on the downside and upside. Investors tend to chase their performance in good times and rapidly discard them during market downturns for safer bets.

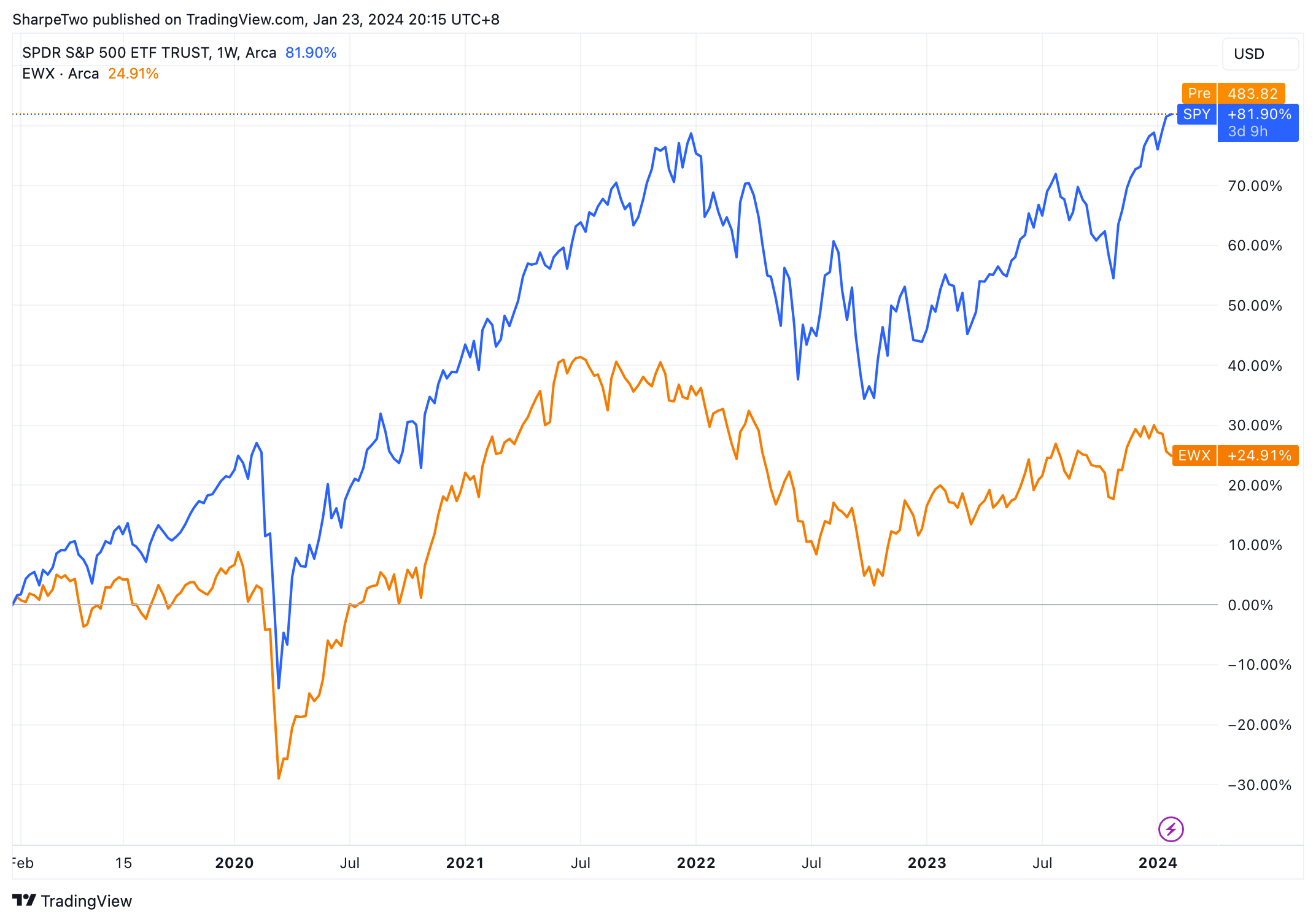

Let's take a look at how EWX has fared against the SPY over the past five years.

The ETF experienced significant losses during the COVID-19 crisis but then managed to narrow its gap with the broader market benchmark. Notably, it plunged during the inflationary struggles and the Russia-Ukraine conflict. What's intriguing is its underperformance during the 2023 rally, primarily driven by the tech sector and the Mag7—a sector and group of names conspicuously absent from EWX's portfolio.

Could we be on the brink of a performance mean reversion between these two? This isn't a far-fetched idea. Macro pair traders contemplating this trade should definitely crunch the numbers before taking the plunge.

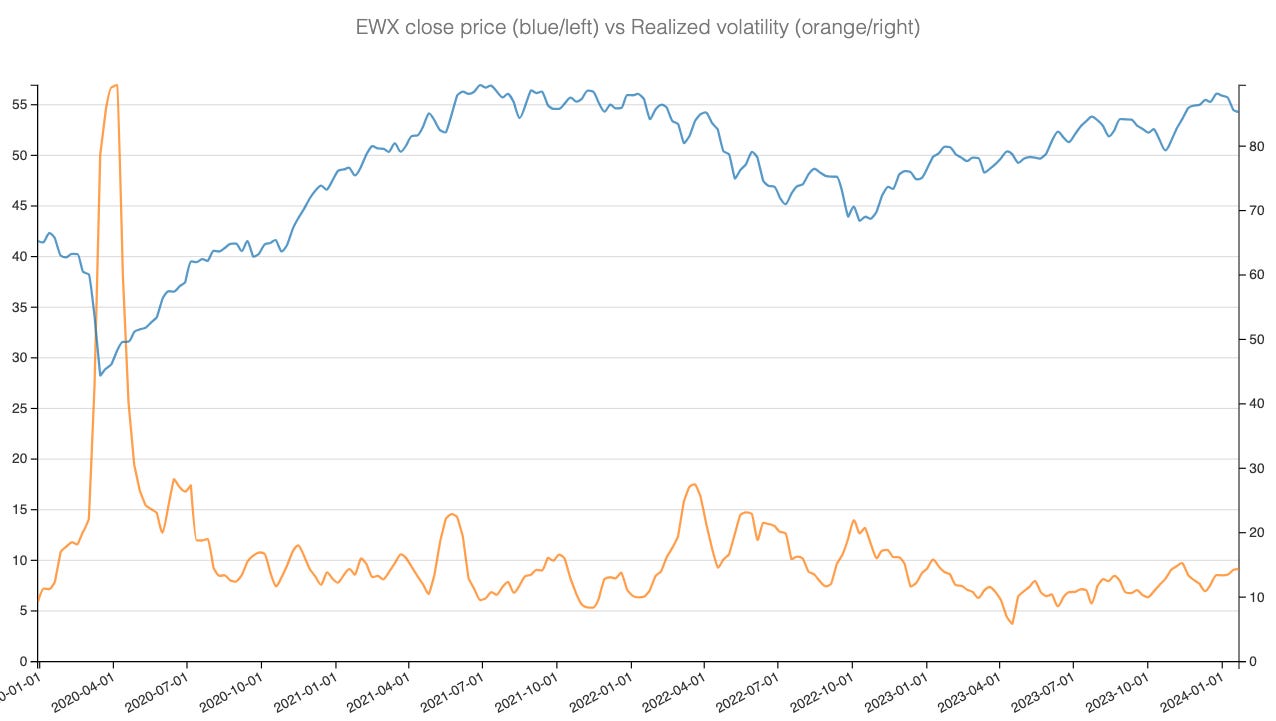

At Sharpe Two, our primary focus is on volatility, and what's particularly noteworthy in EWX over the past four years is its relatively contained realized volatility if you put the COVID-19 shock aside.

Currently trading just below 15, the realized volatility level indicates that barring some violent reactions to significant global events, the index tends to either drift upwards or downwards. This movement is typically dictated by the ebb and flow of global investor money.

As we edge closer to what's often the more eventful part of the trading year, and with the index hovering near all-time highs, there's a possibility that traders haven't fully adjusted their quotes to account for potential risks in the upcoming weeks.

Now, let's dive into the data to get a clearer picture.

The Data and the Trade Methodology

Let's set the record straight: we're eyeing a long volatility position in EWX, but we're not forecasting a market crash. Aware that no immediate market risks are on the horizon, our interest lies in the longer-dated options at the tail end of the expiration cycle. These options are more sensitive to changes in volatility (vega) and are likely to respond to any potential recalibration of the current wave of market optimism.

Time to look at the Variance Risk Premium.