Yesterday marked the first significant move of the year in the equity markets. The S&P 500 saw a notable rise of 1.4%, while the Nasdaq jumped an impressive 2.2%, buoyed significantly by Nvidia’s near 7% increase.

For those who followed our recent recommendation to go long on volatility in the indices, this movement was timely. If you're already in this trade, we suggest recentering it. Should you need more guidance on this, feel free to drop us a comment or an email, and we'd be happy to delve into it further with you.

Today, we're applying a similar approach but turning our attention to the bond market.

Historically, equities and bonds tend to show an inverse correlation. Although this relationship was put to the test throughout 2023, both are still driven by similar fundamental factors when it comes to price action.

With the new year just beginning, we feel it's an opportune time to add some positions on the long side, particularly if they're priced attractively.

If you haven’t subscribed yet, now's the perfect time.

Let’s dive into today's strategy.

The Context

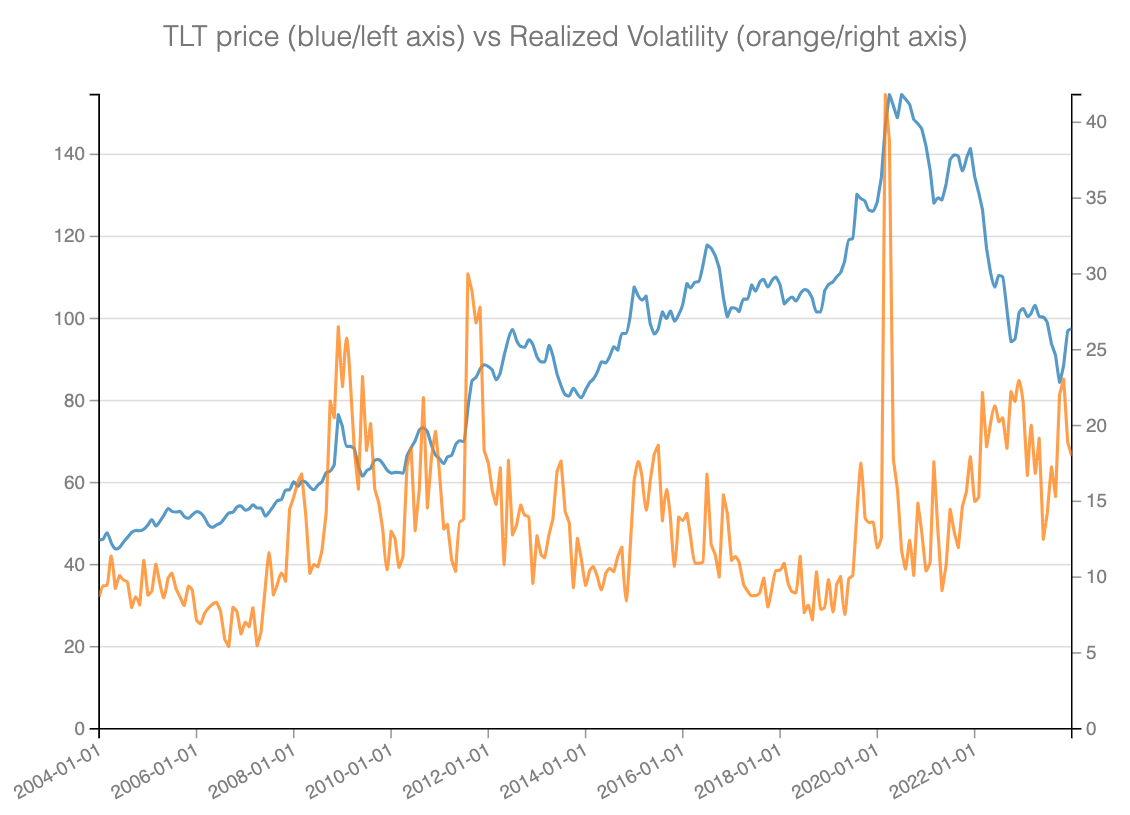

The bond sector experienced one of its most tumultuous years on record.

Apart from the extraordinary spikes during the Great Financial Crisis, the European debt crisis, and the onset of COVID-19, this past year stands out as one of the highest in terms of volatility for TLT.

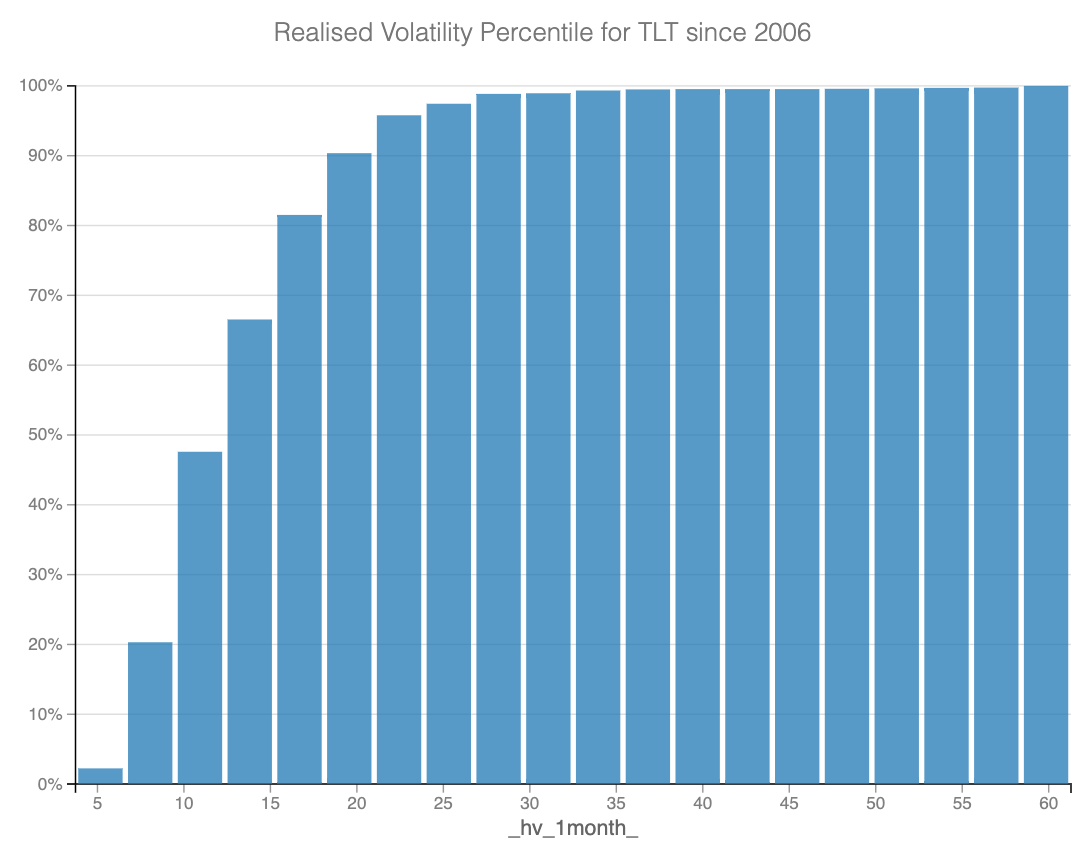

Currently, the realized volatility is around 17, but it was as high as 20 just a month ago, placing it above the 90th percentile since 2004.

This surge in volatility can be largely attributed to the unprecedented tightening cycle that began in 2022. Interest rates soared from a mere 0.25% in March 2022 to 5.25% by July 2023. After nearly a decade of ultra-loose monetary policy, major players in the bond market were compelled to reevaluate and adjust their portfolios to adapt to these new conditions.

The Fed's tightening cycle appears to be drawing to a close, as indicated by Chairman Powell last December. And, as is often the case, the market reacted with its usual measured response... just kidding. In a burst of exuberance, the market is now pricing in no fewer than six rate cuts for 2023. Why is this considered overzealous? While we won’t dive into a detailed macroeconomic debate, we'll stick to the facts: the FOMC committee has forecasted, at most, four rate cuts in 2024.

It seems someone is off the mark, and given the market's almost bipolar nature, we're inclined to side with the Fed's perspective.

As we discussed in our Sunday note, this week's major event is the upcoming inflation data. These figures have the potential to prompt market participants to reassess their expectations, especially if inflation turns out higher than anticipated.

With this backdrop, let’s now delve into the data to pinpoint the most opportune part of the expiration cycle.

The Signal and the Methodology

As is our standard practice, we begin our analysis by comparing the current price of the front-month straddle in the expiration cycle to the subsequent movement in the underlying asset. To facilitate a clearer understanding, we compute a z-score based on the last month's data: