Risk premia is the price the market is ready to pay for a well-understood and identified phenomenon and the set of risks that come with it.

A great example is the mispricing of puts compared to calls, known as the volatility skew amongst options traders.

Most market participants' job is to put money to work, and their natural inclination is to be long the market. Think of money managers, like asset managers or pension funds. They want to be protected against any market downturn that could hurt their performance.

As the famous saying goes - there is no free lunch, and anyone (most of the time market makers) willing to sell these puts will demand extra compensation for the risk of seeing the market collapse.

💡 When an accident occurs, you send the bill to your insurer.

If it is expensive, I should sell it, right?

Even if it is more expensive, it is still an attractive value proposition for the fund managers, and they are willing to pay that premium for protection from the downside.

They also don’t need as much protection against the upside because … well.. they are long. If anything, they are one of the most significant call writers against stocks they own, as it allows them to collect premiums and boost their performance. And what if the call strike is breached? Well, they sell the stock at the price where they are delighted to see it go.

So if it is overpriced, all I have to do is sell it and make millions, right?

Well, not exactly. One of the common mistakes of traders discovering options and how options are generally more expensive than their theoretical value is to jump on selling puts as a way to generate income. This strategy can work but can also result in some awful outcomes.

💡 Selling because there is a premium is not a sensible strategy

As an option seller, you are an insurance provider

Think about it for a second. When you decide to sell options, you become an insurance provider to the marketplace. An insurance provider is in the risk assessment business and gives a quote based on the conditions it has been presented with.

It can be painful and frustrating to be on the other side of the trade and see how the premium can significantly vary depending on our personal circumstances (smokers looking for health insurance, 20-year-old single man looking for car insurance…).

Our job on the stock market is the same, except for a major catch. The insurance provider in the real world decides unilaterally what the price of your insurance will be. You can accept it or get a quote somewhere else.

In the stock exchange work, the market’s fluctuations decide the price of these insurance contracts at any moment, and you have no say in it. Therefore, your job is to reverse engineer the prices and see if you are well compensated for the risk; if not, you should stay away.

How do we do that? One way is to assess the variance risk premium. This fancy appellation describes the spread between implied and historical volatility. Traditionally, the implied volatility is higher than the realized, precisely because put sellers are demanding a premium for the risk they are taking.

Circling back to the point we were making earlier on - the decision to sell an option should not be based on the presence of the spread but on how wide the spread is.

💡 Selling options because of the implied volatility premium is not enough.

A concrete example with XLU

Selling OTM options blindly because they are overpriced compared to their theoretical value can lead to disastrous consequences.

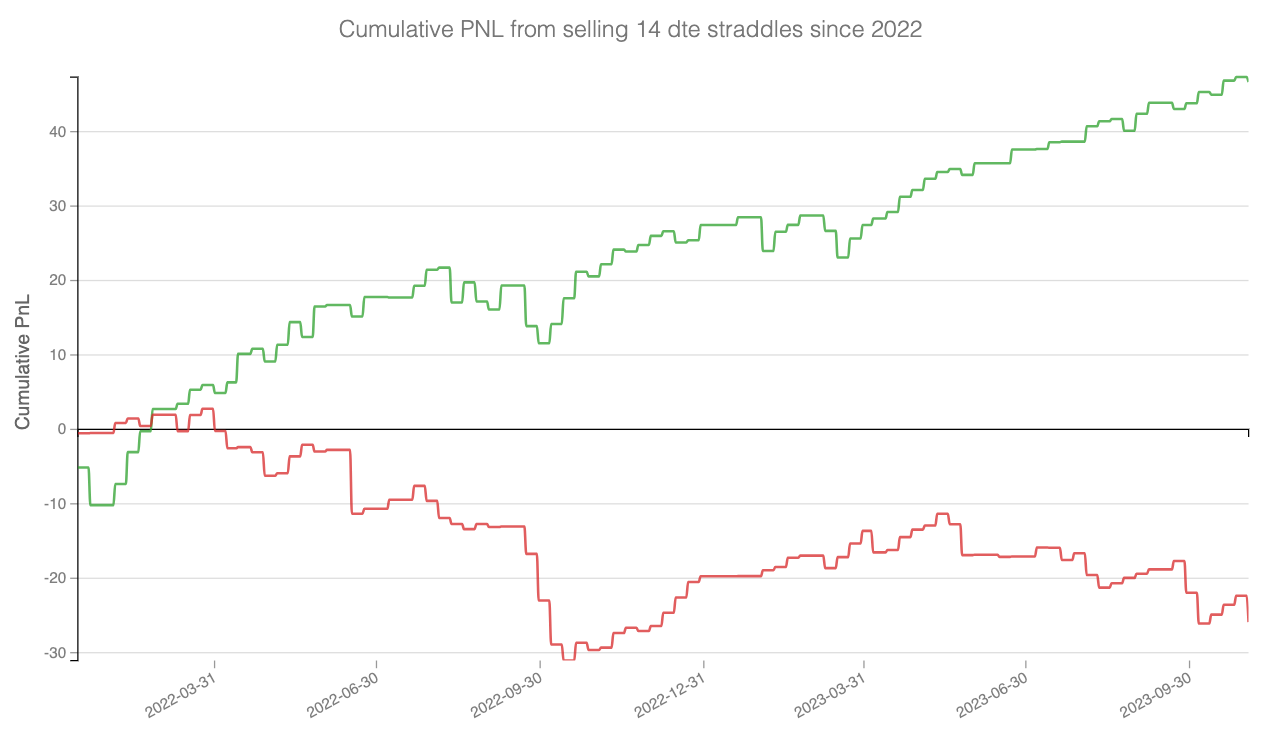

Time for a concrete example. In the chart below, we have decided to sell a 14 DTE (days-to-expiration) ATM straddle every Friday when they become listed on the market. We then hold it to expiration without management (delta hedging, restriking, etc).

This strategy resembles a lot of what is prone by many market strategists and brokers online and, as stated earlier, can have two very different end games.

We compare two different tickers.

The ticker in red is XLU, an ETF tracking the returns of a basket of utility companies. Utility companies (think water or electricity bills) are easily understood, and their revenue is reasonably predictable. The need for protection is still present but well-priced despite the apparent premium compared to realized volatility. Curious about the ticker in Green? Subscribe to know what it is.

The same strategy tells two different stories, as these two names clearly show. The one in green consistently makes money. XLU in red, on the other hand, doesn’t seem to go anywhere. It does lose a little, not in a catastrophic way, but it certainly doesn’t look like a one-hit wonder.

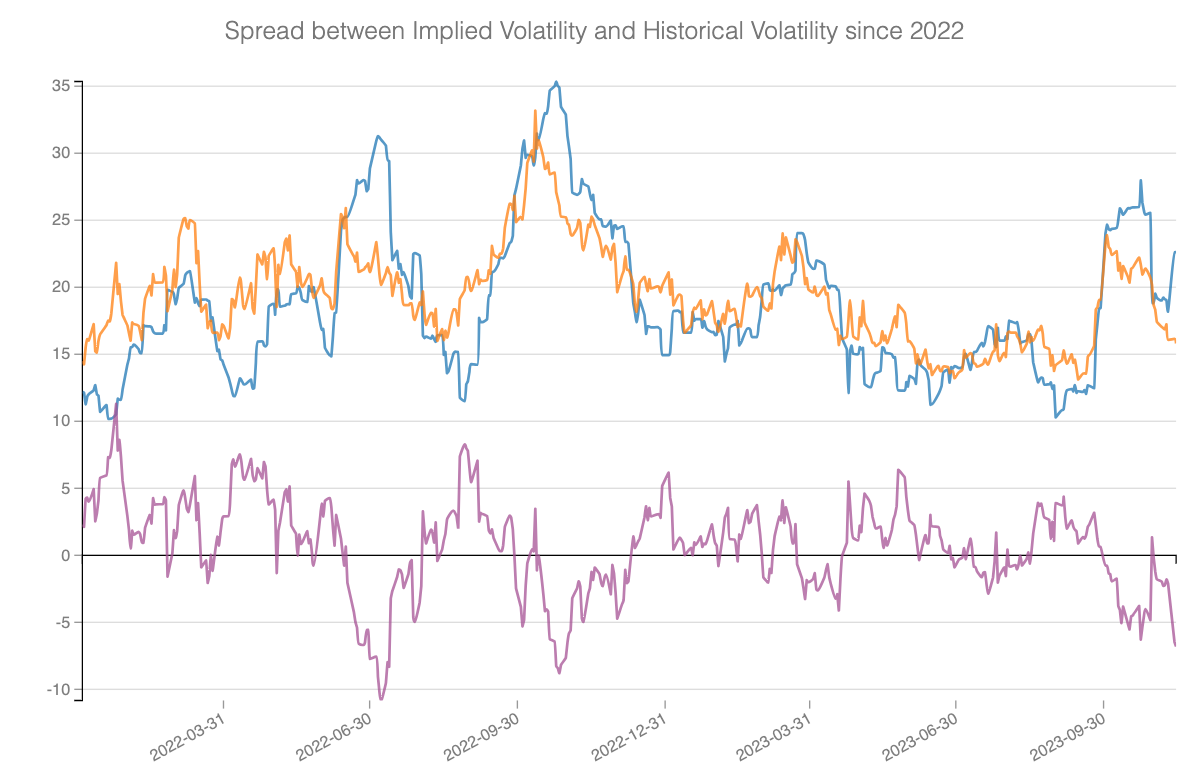

Does that mean that there is no money in selling straddle in XLU? No, and this is why studying the variance risk premium is so important. The chart below shows the variance risk premium in XLU since 2022.

In orange is an implied volatility index derived from option prices in XLU. In blue, you have the historical volatility using XLU close prices. The difference between the two metrics, in purple, is what can be considered the Variance Risk Premium. It is the excess amount of volatility that the market is asking in comparison to the actual realized volatility.

Walking on the edge

Although this method could be improved, it is enough to demonstrate our point: most of the time, the implied volatility from the option market exceeds the realized volatility. The purple line is positive except for specific occasions of high stress levels in the market. Yet selling it does not guarantee a profit as per the PnL line.

The standard approach to collect the variance risk premium is rigorously delta hedging the position. If the realized volatility is below the implied volatility sold, the PnL at the expiry will be positive.

However, delta hedging is not a magical solution, and often, the profits are way less evident when we factor in the high transaction costs and heavy management (we should be aware of our ability to make expensive mistakes).

💡 Delta hedging is expensive and prone to error.

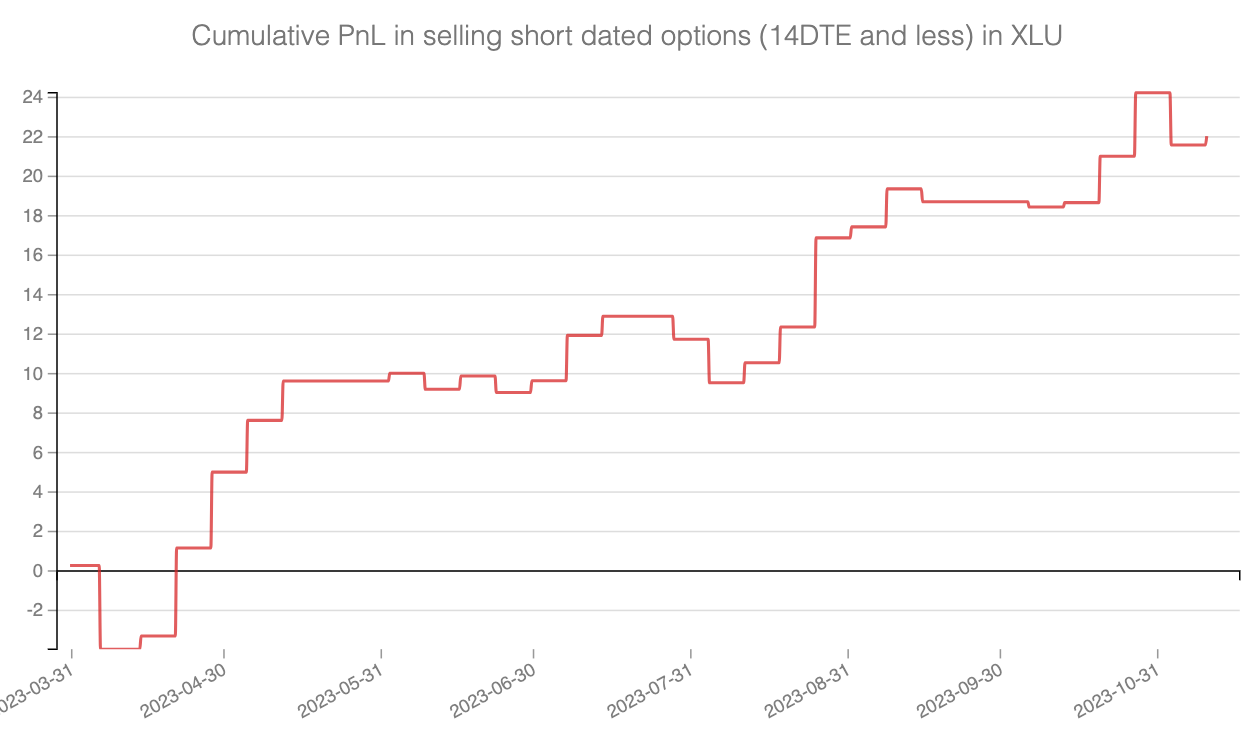

If we want to avoid delta hedging as much as possible, a finer understanding of the variance risk premium is mandatory. Selling it only when stretched to the maximum is a much better strategy. With the right kind of analysis, we could transform the stuttering red curve above into something much more appealing like that one.

At Sharpe Two, we aim to bring you the best of our analysis and process to extract edge from option data. Subscribe to learn more about the Green ticker or the methodology used to improve the XLU pnl curve. You will also receive trade ideas that can be implemented directly.

Thanks for reading Edge From the Trenches! Subscribe to receive daily trades and analysis.

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Disclaimer: The content provided here is for informational purposes only and should not be construed as financial advice.