It's already Thursday, and it is time to visit the grocery store. Not to buy anything, no, but instead, to sell overpriced straddles to fund managers. Today is a special occurrence where we, the market, tend to overpay for protection, just in case.

Indeed, this Friday is NFP day, a critical figure for assessing the health of the American economy and gauging the Fed's policy. Yesterday, Mr. Powell appeared as tight-lipped as ever, reiterating a message now perfectly assimilated by the market: "The Fed is in no rush to cut but is acutely aware that waiting too long will hurt the current resilient and strong American economy."

The next FOMC meeting is not for another month; we still have some important figures after this NFP to check the course of inflation. Therefore, as important as this figure may be, only a catastrophic reading to the downside could spook the markets—in theory.

That's the thing with the market—it always takes a divine pleasure to take your most certain expectations and throw them in the toilet with a ravaging smile while you watch your P&L turn from green to sanguine red.

"But why so mean, Mr. Market?"

"Because I can."

Because it can or because it should, according to sell-side economists.

"In any case, it will, at some point. Maybe not this Friday, but we never know. And better safe than sorry."

You may be disappointed by the lack of rationale driving the heads of fund managers, who are easily swayed by analysts worldwide, especially when they have something to sell to them. The pitch usually has two parts: an obscure asset class or geography, a hidden gem that will make their year, their reputation, and their career, quickly followed by the protection that comes with it.

However, on NFP day, the focus is first and foremost on major asset classes.

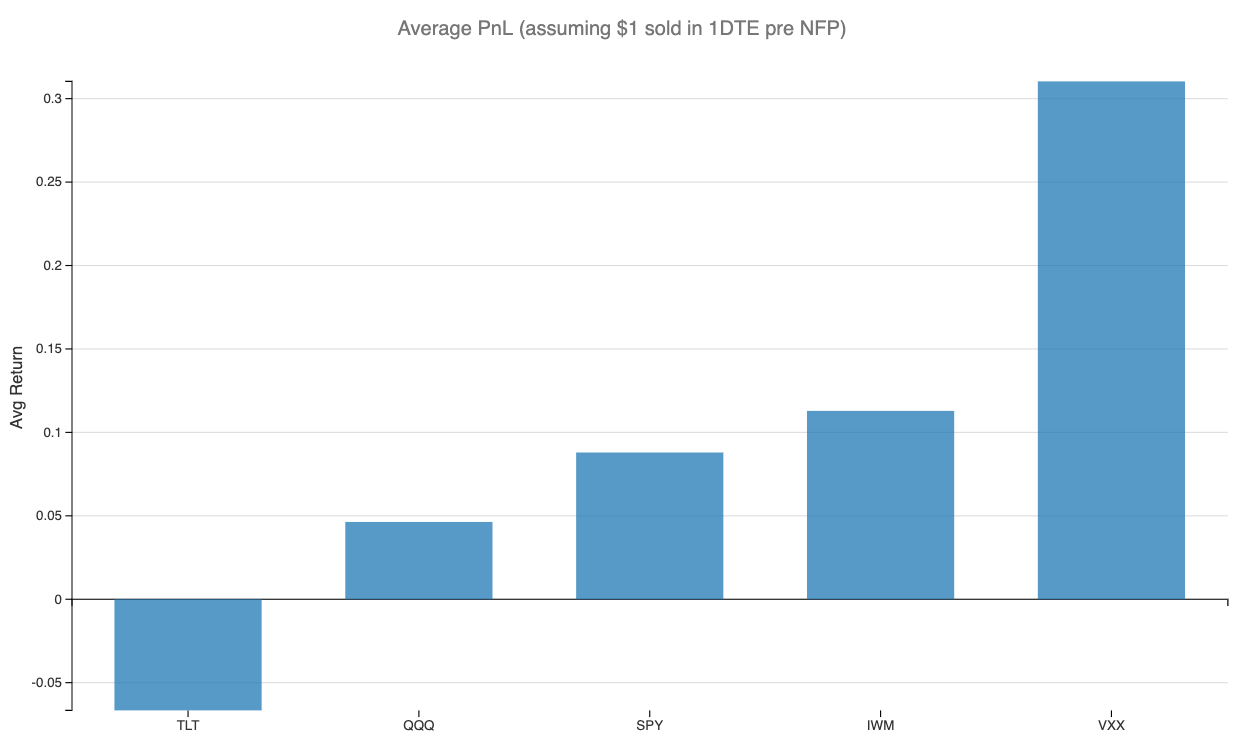

Let's review data on how much insurance costs in major indices overstate the actual movement in the underlying. To that end, we will compare the returns on straddles sold on Thursday before the NFP and closed at the end of the day on Friday.

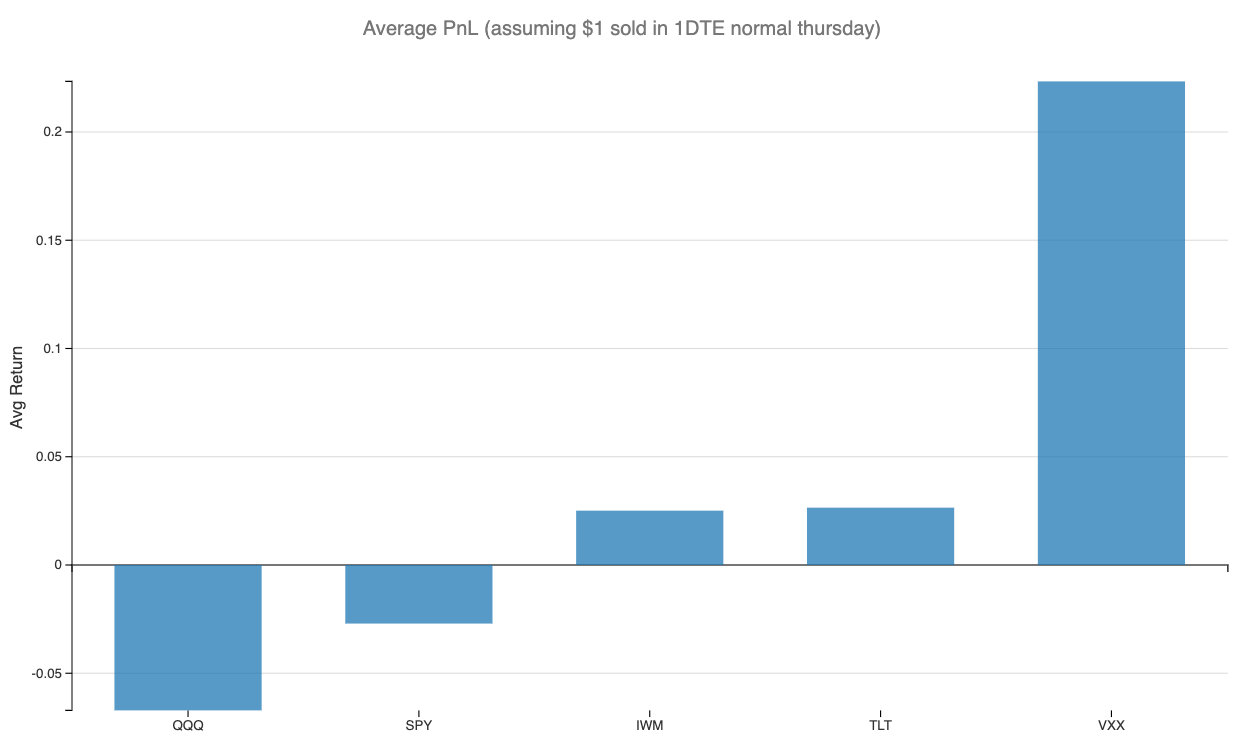

Since 2022, all major indices have exhibited some performance on the Thursday before the NFP. How does this compare to any normal Thursday?

While VXX tends to perform no matter what, its performance still improves by almost 50% on average. As for the other major indices, they tend to become much more profitable than on any other Thursday.

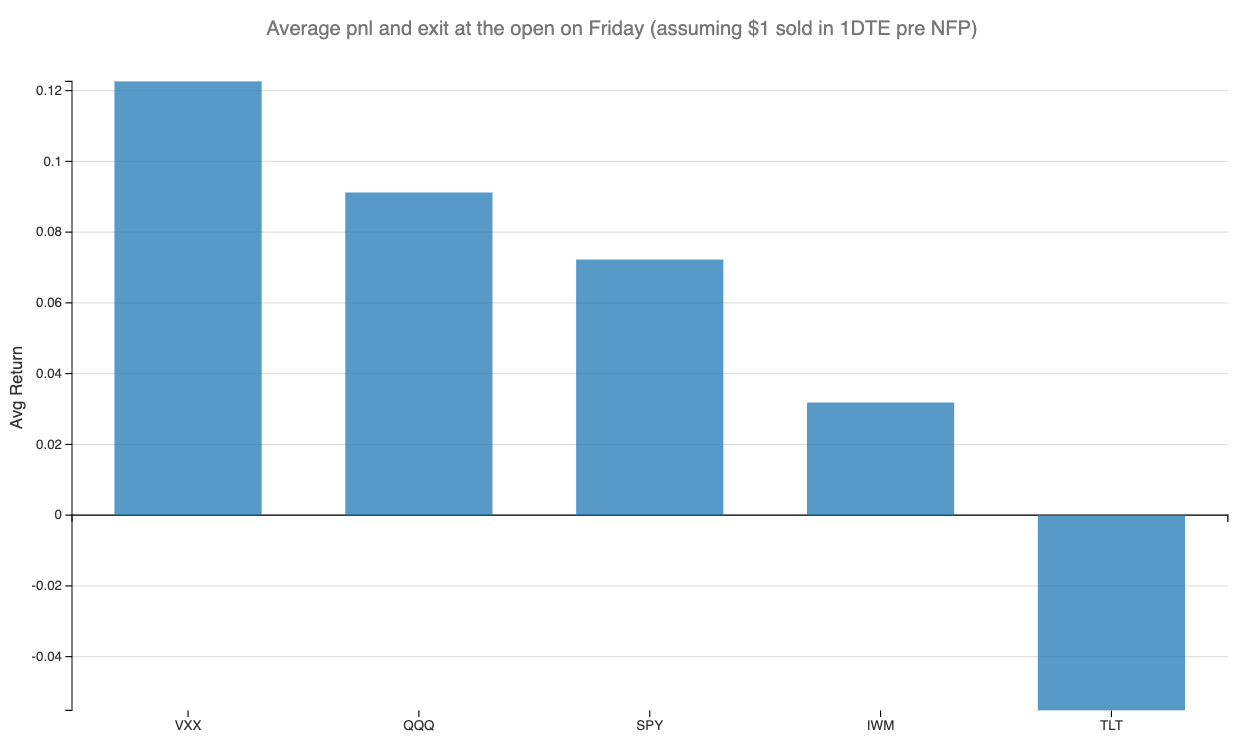

Now, if you wanted to capture only the NFP effect, a sensible thing to do would be to exit right at the open, as the uncertainty driver would now be behind us. Let's see what that would mean from a return perspective.

The results greatly improve for the QQQ but tend to be less favorable for IWM. In the end, you decide how to execute. We are simply messengers.

With that in mind, let's define this week's rules and list.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

The rules

Before we start, let’s do a quick round-up about the rules.

- Short an ATM straddle in the 1DTE contract 05/04 as close as possible to the close on Thursday night. In all our metrics and charts, we assumed an execution at 3.50 pm, but the entry timing doesn’t matter too much: avoid getting in too early, but getting in too late gets you less premium.

- Exit the position as close as possible to Friday’s expiration. Again, we assume an execution at 3:50 p.m., but depending on your risk tolerance and satisfaction with the returns, it can be useful to manage the position earlier.

- One word of caution: if you get assigned, leave the trade altogether and eliminate the underlying. If you decide to keep it and “sell premium against it,” it is at your discretion and outside this strategy's scope. It’s okay to keep the other leg expiring out of the money; there is no reason to pay an extra dime to your broker. Ensure it is far enough from any post-market move — the settlement happens at 4.15 pm, not 4 pm.

One last thing—we still have a few spots left in our Discord community, where we monitor this strategy and many others mentioned in this newsletter. Contact us if interested, and we will share the pricing details.