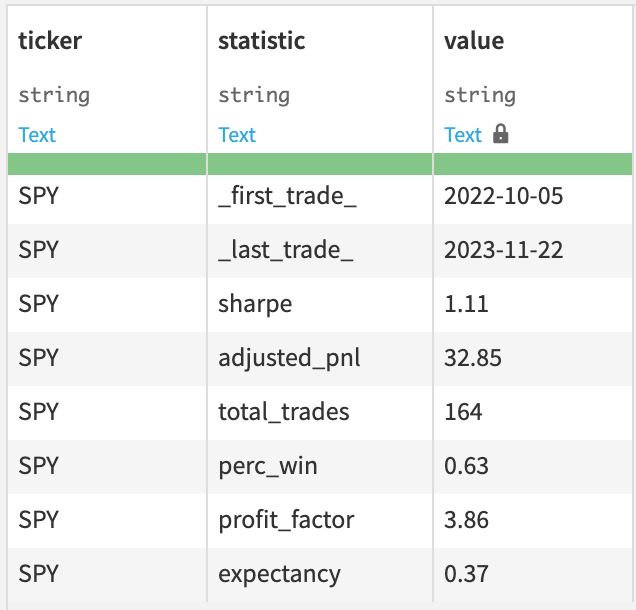

What to find - a seasonality analysis on 0DTE ATM straddles in SPY and an improved strategy in 0DTE with a Sharpe>1.

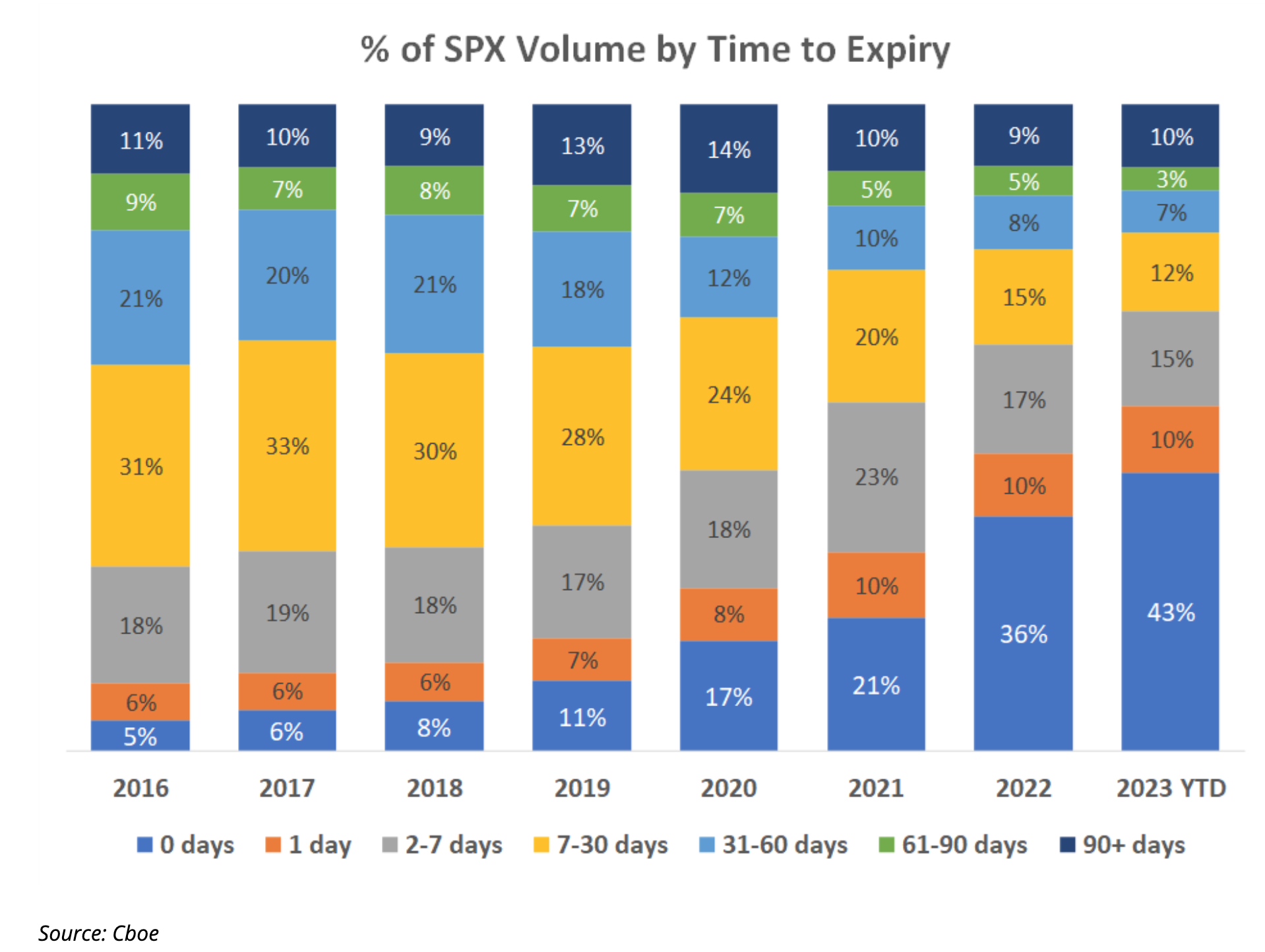

0 DTE (for 0 day-to-expiration) contracts have been the stars of the equity markets since their inception across the past two years. And if they have been the subject of less attention lately, they drive about 43% of the daily volume in the SP500 options contracts. In August, the tally went as high as 50%!

So much so that the Nasdaq has extended daily expirations to some of the most active ETFs like TLT or GLD. We can’t blame them: it is hard to say no to good business when you see it.

But back to the topic du jour - is there any form of seasonality when trading 0DTE in SPY?

Sell at the open and go away.

One of the most popular strategies amongst retail investors has been a variation of the infamous adage “sell in May and go away.” Instead, it has been transformed to “Sell the 0DTE ATM straddle at the open and go away.”

Many retail gurus have been reporting crazy gains with this simple strategy. And if we always encourage our readers to stay measured when looking at some screenshots, data elements support that theory.

The trade methodology:

- sell an ATM at 9.35 am

- close the trade at 3.50 pm to avoid any risks of assignments post-markets

(Side note - Why close at 3.50 pm and not let it go until expiry? There is a non-negligible risk of being assigned one of the two legs and the need to manage some stocks the next day. That could seriously affect the overall strategy performance. We have decided to flatten the position completely at the close to focus solely on this effect.)

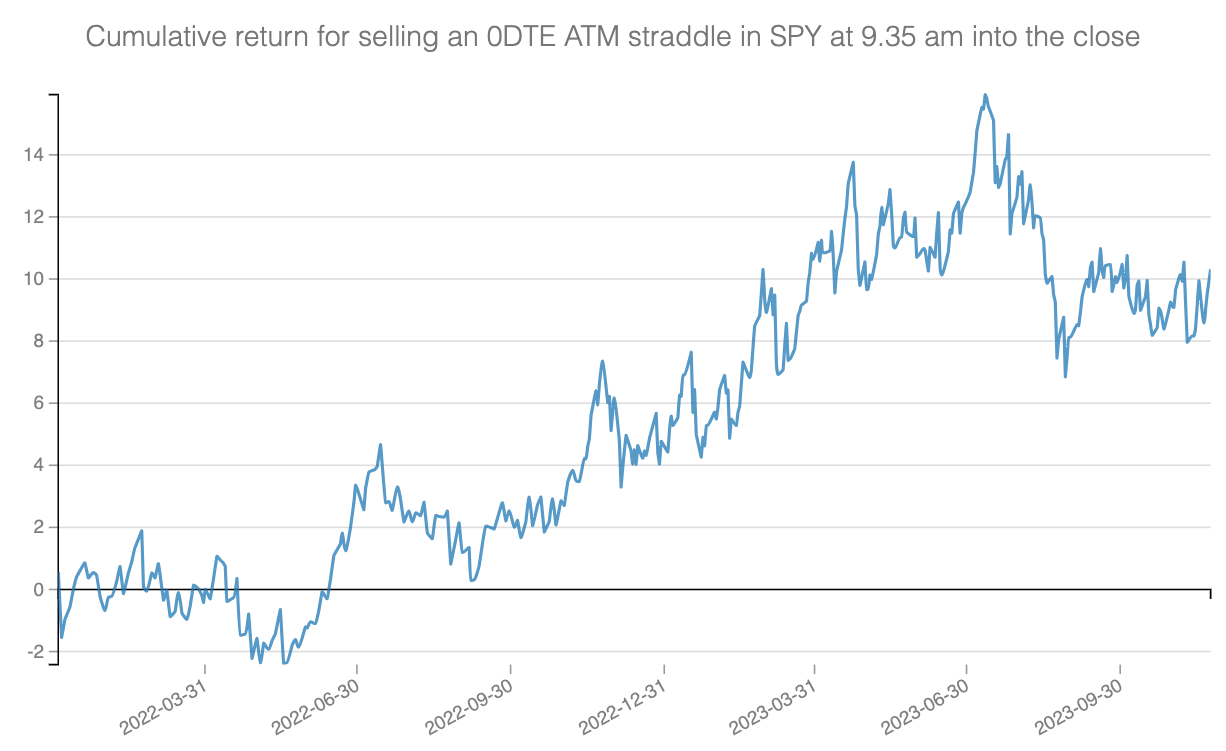

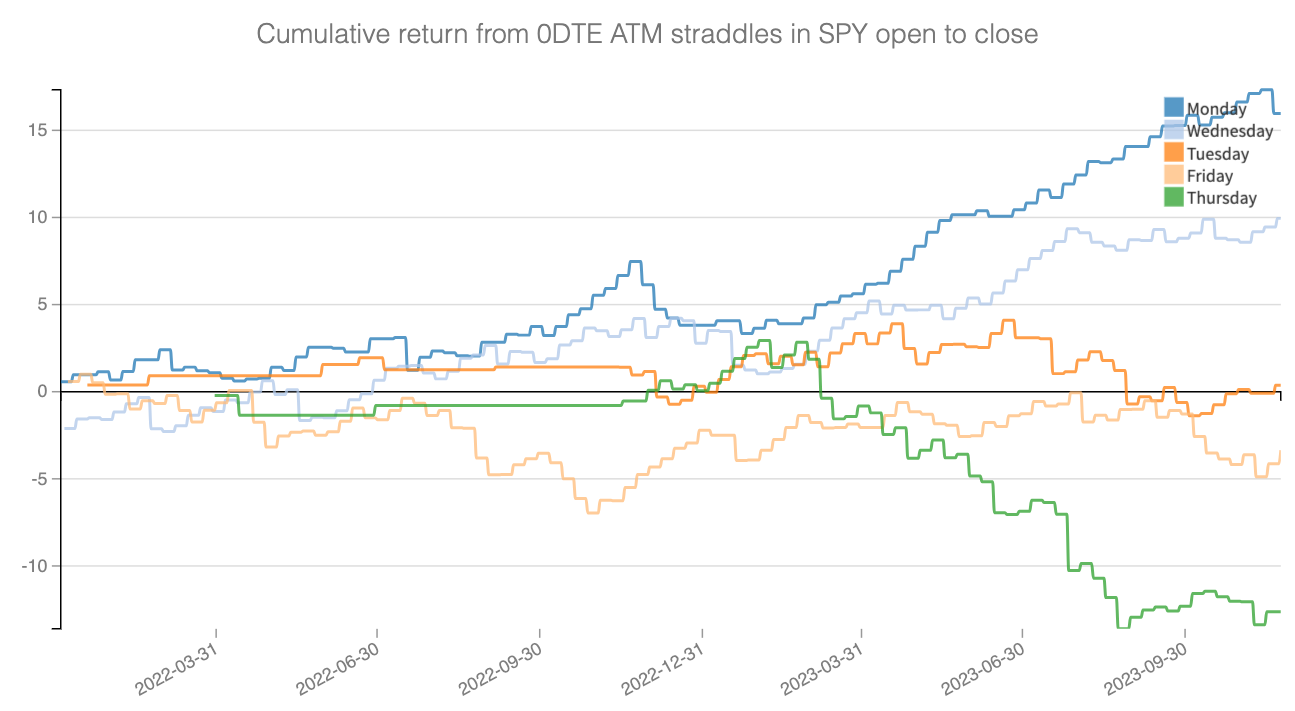

Let’s look at the strategy's performance for the past two years.

The chart shows a gradual uptrend, particularly noticeable at the end of 2022, due to two converging factors:

- The introduction of Tuesday and Thursday expirations enriched the suite of 0DTE options.

- A gradual decline in overall market volatility, acting like a gentle tailwind aiding those sailing, or rather, selling ATM straddles.

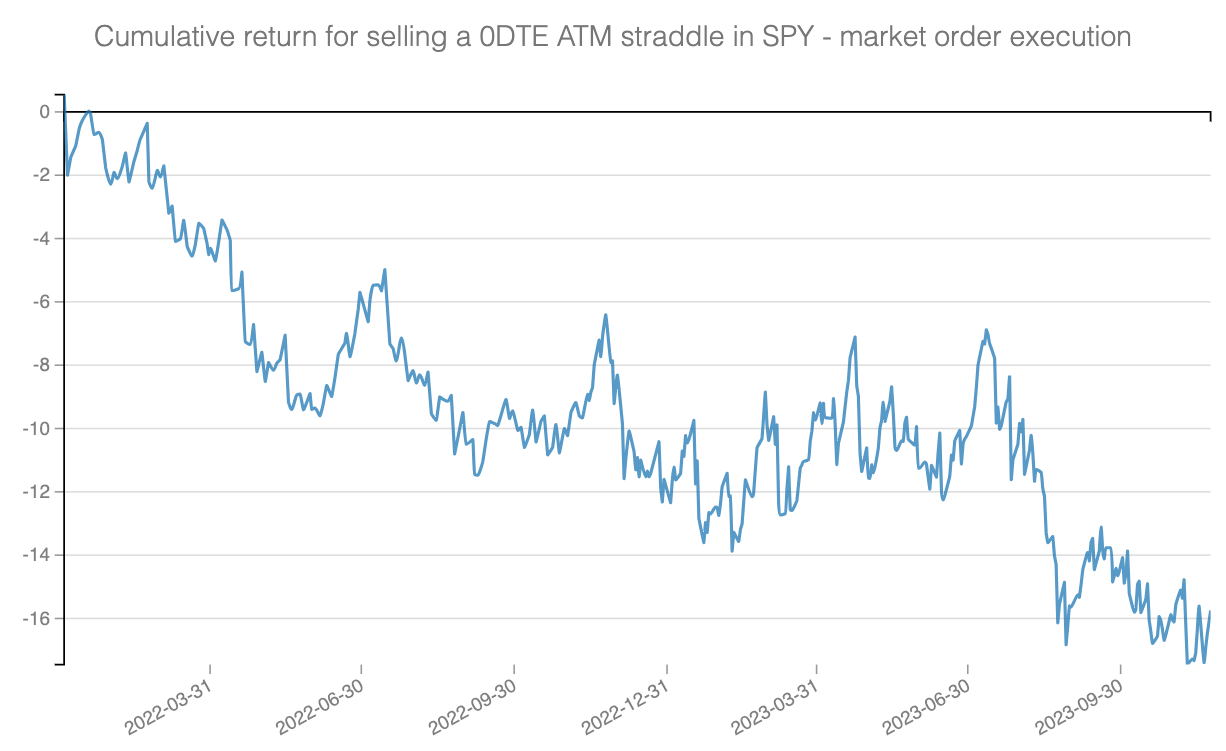

Despite these developments, the strategy still doesn't quite captivate us at Sharpe Two. A critical factor is its sensitivity to costs. Failing to execute at the mid-price could lead to consistent losses, not to mention the variable brokerage fees that can further impact profitability.

You know who loves 0DTE more than retail traders? Exchanges, brokers … and Citadel.

For the rest of the analysis, we assume that you always get a fill at mid-price - which, to be frank, considering the extreme liquidity in SPY 0DTE contracts, is not a crazy assumption either.

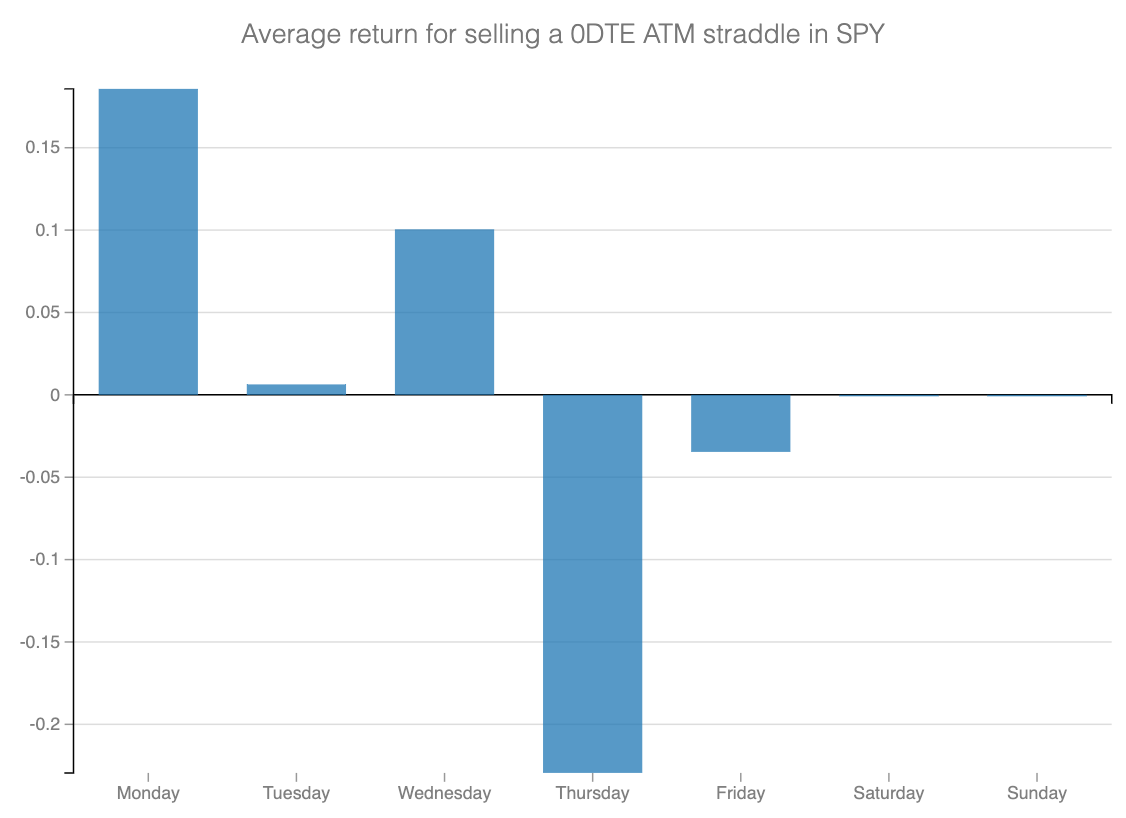

The curious case of Thursdays

Something interesting came up to the Sharpe Two while reading some of the forums. Thursdays are the crux of 0DTE straddle sellers. They all complain about how difficult it is to make money that day. We wanted to check things for ourselves, and … surprise, surprise, there is truth to that again.

A good explanation? It is likely correlated with the amount of economic news hitting the market. Thursdays are usually the busiest days, followed by Tuesdays and Fridays, which were also very poor-performing days.

If you have a better hypothesis, hit us in the comments, and we will investigate.

Is it enough to try a strategy where you buy a straddle on a Thursday instead of selling it? The idea has some merit, and even if we stay away from 0DTE at Sharpe Two, just for the thrill of it, here is what the pnl curve would look like per day of the week.

The data show that since their introduction in November 2022, Tuesdays have not made any money, while Thursdays are in free fall.

A strategy improvement

Let’s design the rational strategy based on the data:

- Avoid Tuesday and Friday - there isn't merit in applying that strategy on these days.

- Get involved on Mondays and Wednesdays

- Buy the straddle on Thursday

In Green, we have the rational strategy versus naively selling a 0DTE ATM straddle daily. It already looks much better.

Based on this performance over the past year, should you put the trade on?

While this strategy marks a notable improvement, the absence of a solid fundamental explanation for its seasonality and a "relatively" low Sharpe ratio lead us to pass on it.

Consider this: what if the current news cycle calms, diminishing the surprises often seen on Thursdays? In such a scenario, a long volatility strategy might consistently incur losses. Conversely, should we consider buying straddles on Tuesdays and Fridays should the news become more unpredictable?

At Sharpe Two, we prioritize strategies that are predictable and repeatable. Despite its intriguing aspects, this strategy falls short of meeting our criteria.

We advise investing with caution and responsibility for those inclined to try it.

To put it in layman's terms - do not YOLO in 0DTEs, you degens!

Follow us on Twitter @Sharpe__Two, and feel free to share our work with those you think would benefit from it.

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.