The long-short strategy, where one asset is bought, and a similar one is sold, is a staple in the finance world. This technique traces back to 1949 with Alfred Winslow Jones, the pioneer of hedge fund management.

Tiger Capital and his legendary founder, Julian Robertson, popularized the approach in the 1980s: he used to purchase stocks in the top 10th percentile while selling those in the bottom 10th. This strategy banks on the premise that fundamental discrepancies will widen the value gap between these stocks.

In the commodities market, a well-known play is trading the spread between Brent and crude oil. Despite some technical differences, both are essentially oil, and their price disparity typically hovers close to a historical mean.

When we started on a trading floor about 13 years ago, right in the middle of the European debt crisis, we were assigned a book of German bonds to trade against euro short-term interest rates (EURIBOR) before moving on to the American 10Y versus the Canadian 10Y, then Canadian 10Y versus Australian 10Y.

Good old times …

By now, you've probably grasped the essence of long-short portfolios: they involve assets with similar characteristics, with the expectation that their price differences should hover around an established mean. Deviations from this consensus can often prompt action from a savvy trader.

In this piece, we're exploring a position in the realm of high-yield corporate bonds. Our focus isn't so much on the bonds themselves but on their volatility. And since we're discussing a long-short strategy, we'll specifically examine the volatility dynamics between JNK and HYG.

Let's dive into the details.

The context

2023 marked one of the most volatile years in the history of the bond markets. The primary driver of this turbulence was the market's anticipation of the Federal Reserve's interest rate policies. The third quarter witnessed a steep 18% drop in long-term US government bonds (TLT), followed by a remarkable recovery in the fourth quarter as investors adjusted to the prospect of a more relaxed monetary policy.

The accompanying chart illustrates the significant movements in TLT, HYG, and JNK.

For those less acquainted with the bond sector, the nearly parallel performance of HYG and JNK might come as a surprise. However, this similarity is quite logical – both ETFs track a variety of high-yield corporate bonds. Despite minor differences in their holdings and fee structures, they essentially serve the same purpose.

An interesting development to note is that since October, there's been a subtle yet increasing divergence in the performance of HYG and JNK. The gap between them has widened more than usual. We haven't delved into the reasons behind this – and it's essential to investigate before considering any pair trading decisions based on this divergence.

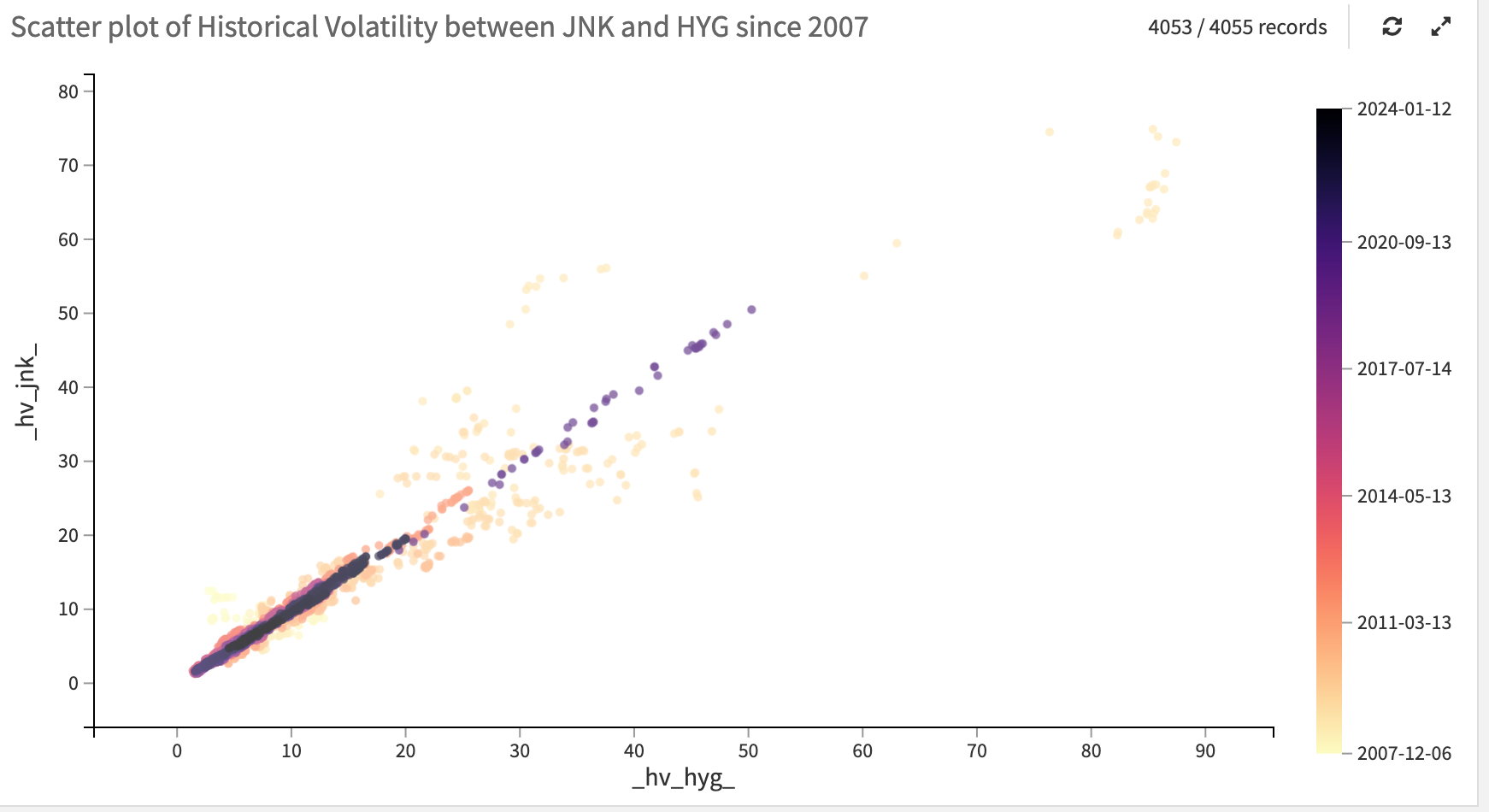

Our focus, however, is on the difference in their respective volatilities, starting with realized volatility.

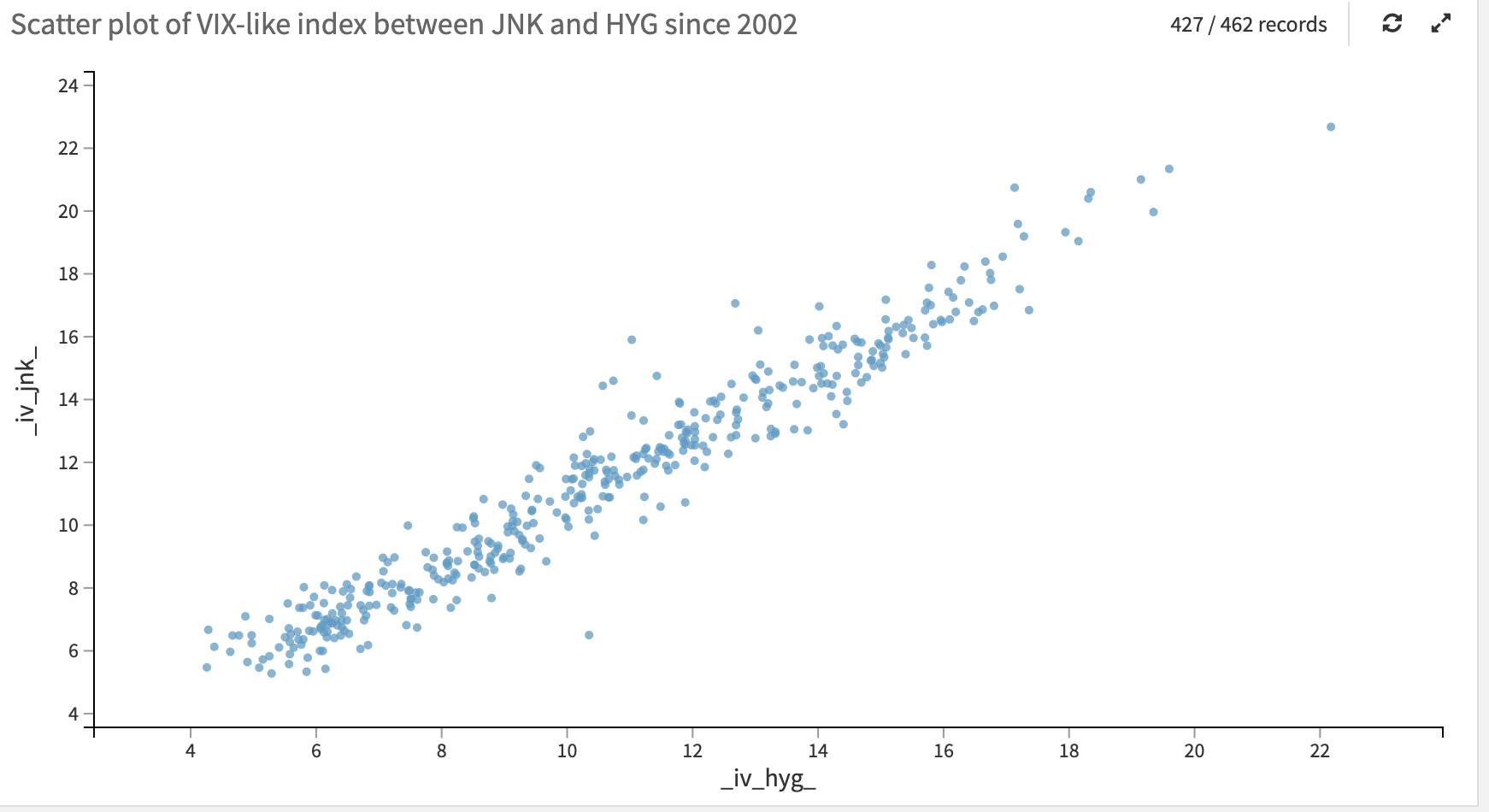

The most striking aspect is how the correlation became near-perfect over time in terms of realized volatility. This can mainly be attributed to long/short traders’ understanding that two similar assets should move in tandem. Yet, when we turn to their implied volatility, the story changes.

This divergence in volatility between HYG and JNK presents an intriguing opportunity for a mean reversion strategy. Let's take a moment to let this concept fully resonate.

Both ETFs are comprised predominantly of high-yield corporate bonds, making their day-to-day price returns nearly identical. However, while there's a notable correlation in their implied volatility, the correlation between their implied volatility isn’t nearly as perfect. Therefore, enough deviation from the mean should generate meaningful trading signals.

Our strategy hinges on this premise: if the implied volatility of one ETF is disproportionately high compared to the other, we consider shorting the higher and buying the lower. This approach is based on the expectation that two assets so alike should exhibit similar implied volatility structures.

Should their volatility structures fundamentally diverge, it would challenge the assumption of their similarity. What might cause investors to drive up the implied volatility in JNK but not in HYG, if the assets are indeed very similar?

Having laid out the logic of our trade, it's time to delve into the actual option prices to formulate our entry strategy.

Note: The remainder of this article is exclusive to our premium members. Consider subscribing to gain full access to our in-depth analysis and insights.

The time-series of these two ETFs closely align with each other, and their ratio averages out to about 1.25, with a standard deviation of 0.14. This suggests that significant deviations from this average typically revert back to the norm relatively quickly. We identified some notable trading opportunities in December last year. As we gear up for the upcoming earnings cycle, new divergences have emerged between JNK and HYG, hinting at the potential for swift mean reversion.

For a pure volatility arbitrageur, the correlation and divergence between JNK and HYG would form the foundation of a robust trade. Typically, such a strategy would involve extensive statistical analysis to validate the mean-reverting hypothesis and determine the best course of action.

We won’t follow that path, though: to validate our strategy, we'll look at the prices of each ETF's straddle compared to their own history over the past three months. Ideally, we want to see HYG's straddle prices being unusually high or JNK's particularly low over this period. The perfect scenario would be where HYG is more expensive than usual while JNK is cheaper.

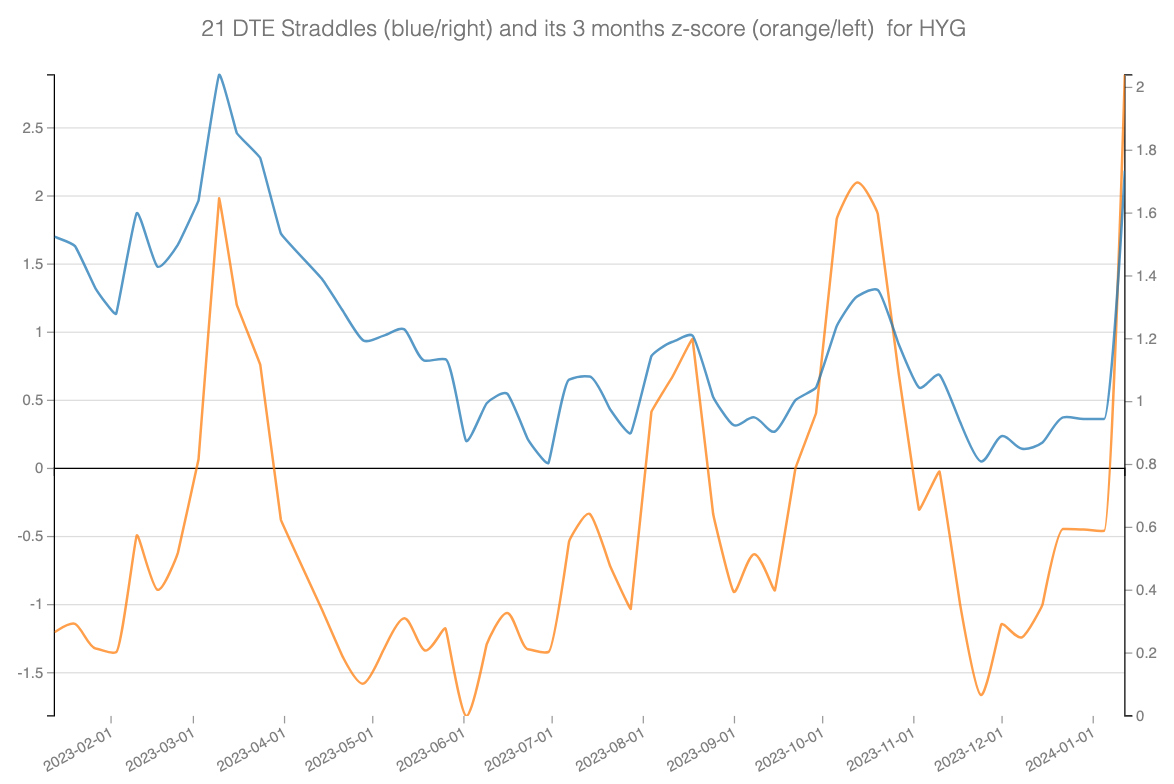

First, let's examine HYG:

This chart is quite revealing, likely indicating a sudden repricing of implied volatility as we approach the new earnings cycle. With a Z-score above 2, it's clear that HYG is currently priced higher than usual – comparable to the levels seen during last year's regional banking crisis.

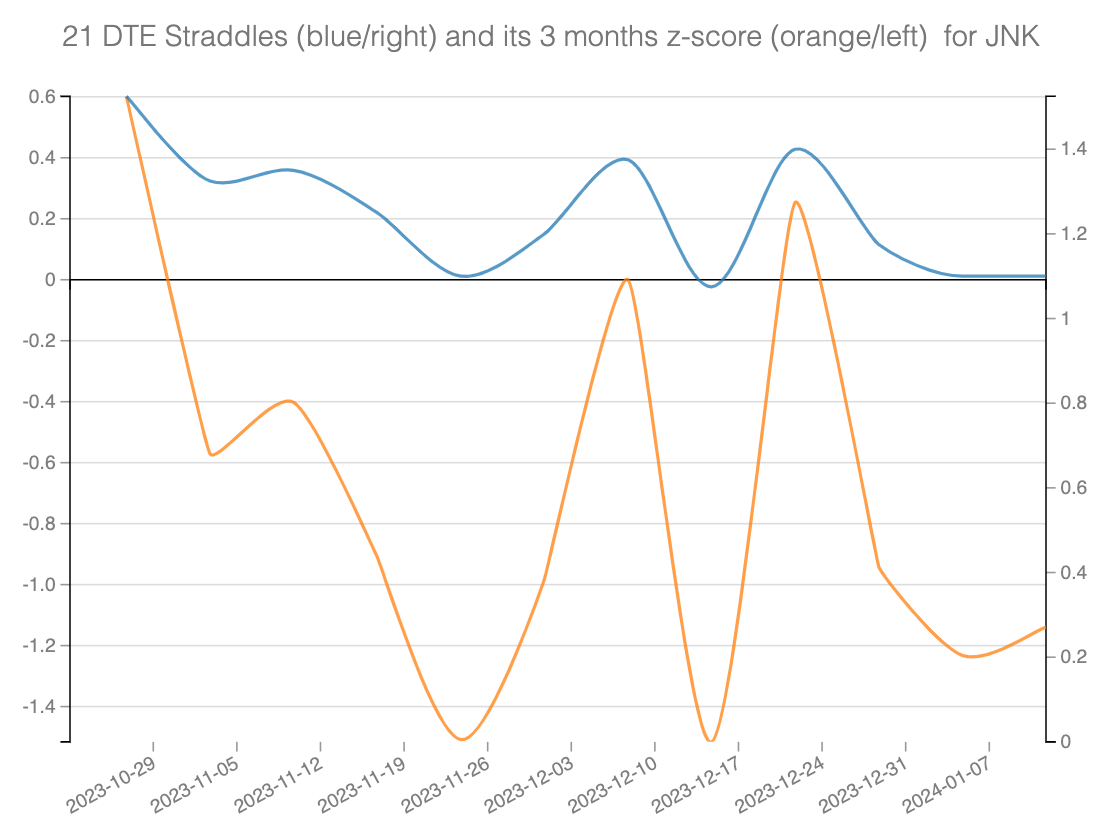

Now, turning our attention to JNK:

Here, we find that JNK's straddle price Z-score is below -1. This suggests that JNK is relatively cheap at the moment, with its straddle price at $1.1, the lowest it has been in the past three months.

This is the perfect scenario we were hoping for; time to move on to the implementation of that trade.

The trade methodology

We've identified a notable divergence in the straddle prices of JNK and HYG, presenting an opportunity for a long/short volatility trade.

To implement this trade effectively, the ideal approach would be to balance the vega collected on both sides. However, given the similarity in volatility profiles between these products, we'll simplify by considering an equal credit of $1 on each leg of the trade:

- Sell the 78 straddle expiring on 2024/02/02 in HYG for approximately $1.7.

- Buy the 95.5 straddle expiring on 2024/02/02 in JNK for around $1.1.

To maintain a $1 exposure on each leg, the proper sizing would be 11 contracts for HYG and 17 for JNK. For retail traders, this sizing might be substantial. A more manageable approximation would be a 12 to 18 ratio, aligning closer to a 2 to 3 ratio.

Ideally, you would focus on the ratio between the two, more than the price of each individual leg - as discussed earlier, a normal ratio is 1.25 (we are currently at 0.64). Any entry in a ratio below 0.97 is still 2 standard deviations wide and leaves plenty of margin for price normalization before the expiration.

Alternatively, a 1x1 ratio is also viable, especially considering that each leg independently shows promising characteristics for a trade entry.

Regardless of the chosen approach, it's crucial to adhere to a risk management strategy that aligns with your financial situation and investment goals.

As always, invest wisely.

Be sure to follow us on Twitter @Sharpe__Two for more of our insights. If our work resonates with you, don't hesitate to share it with others who might find it helpful.

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.