Forward Note - 20260301

Assessing your options.

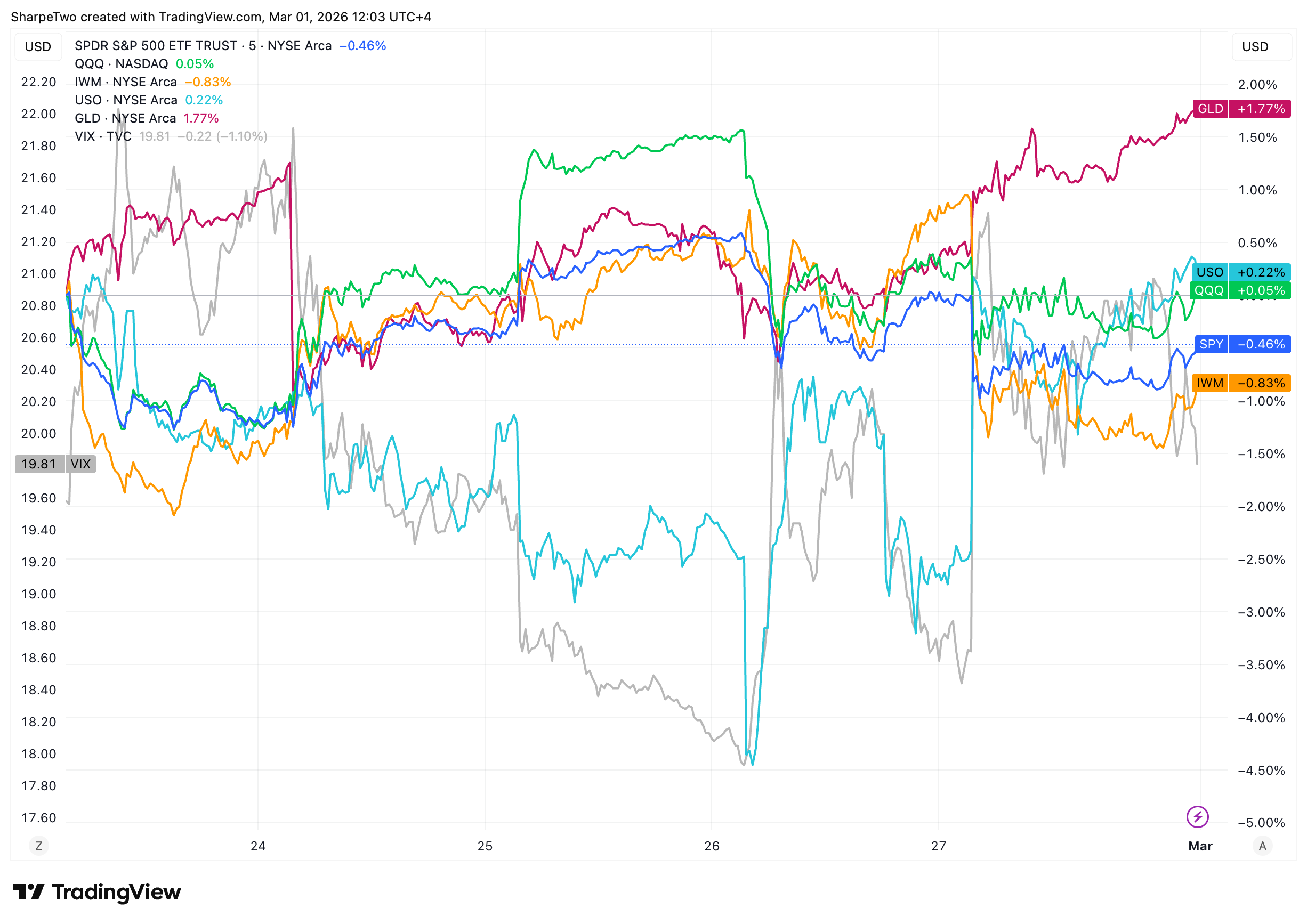

The market closed another choppy week. NVDA’s earnings were stellar, yet the reaction was muted — giving more credence to the prevailing mindset among participants: if the AI transformation is real, it is priced in. We will need further evidence from the businesses actually deploying the technology, not just the hardware provider, to form a more complete opinion.

With this in mind, US equities finished mostly flat and the VIX right under the 20 handle. Gold edged higher into Friday’s close; oil, mostly flat. The big question is what comes next.

The big development over the weekend was the massive joint American and Israeli strikes on Tehran, resulting in the death of Ayatollah Khamenei. After 37 years under his rule, Iran now stands on the brink of civil war — a divided country, a crippled economy, and an aggressive military that has been taking irresponsible, though predictable, actions over the last 24 hours. We write these lines as we hear (litteraly), above our heads, Iranian missiles and drones are being intercepted by the quiet but strong Emirati presence over its national territory. While we hope the situation stabilizes quickly, no one knows exactly what will happen.

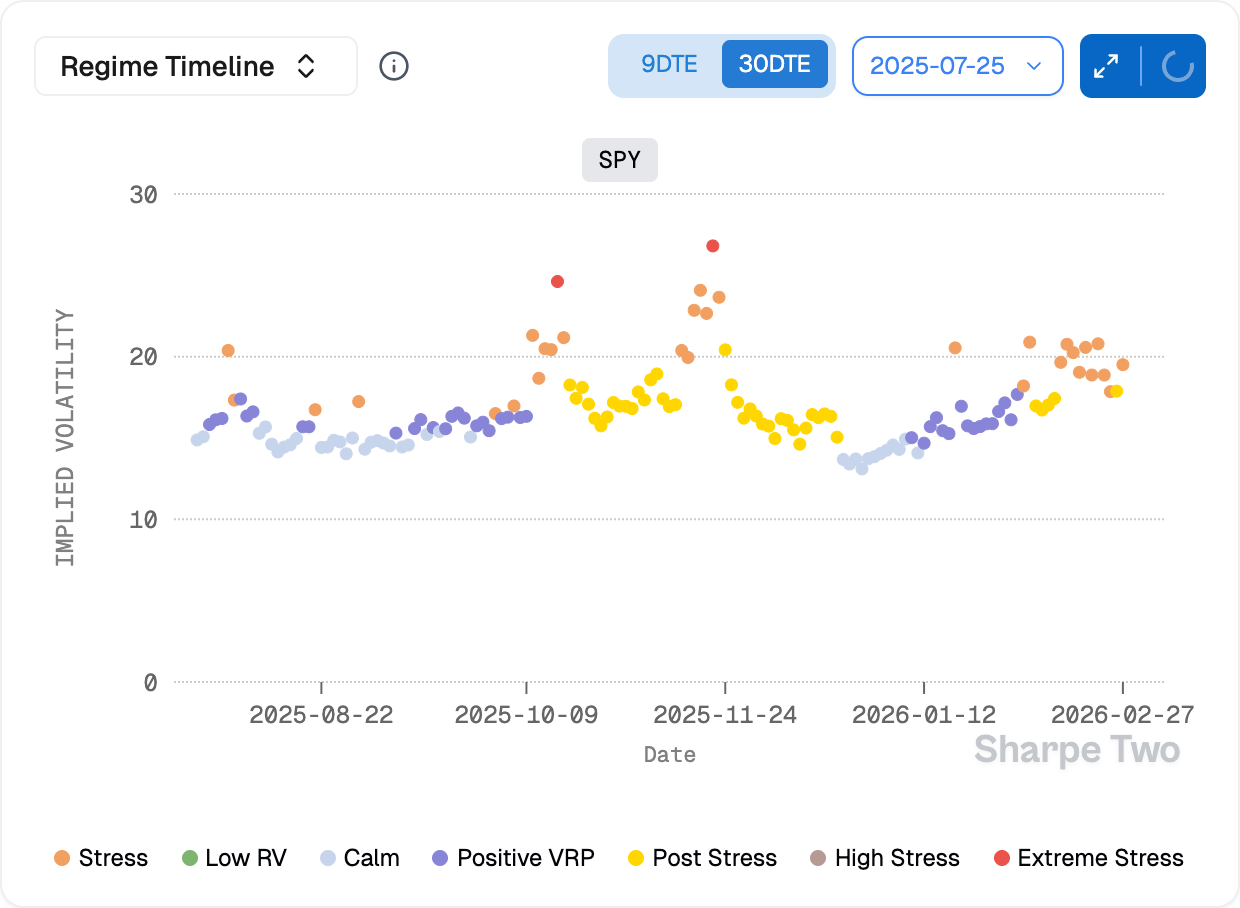

The Strait of Hormuz is now closed, and the impact on oil, gold, and the VIX come Monday is clear — though hard to measure with certainty. By how much will oil gap up? Some reports suggest between 8 and 10%. Could the VIX breach 30? Absolutely. The market rarely rewards particularly intelligent views in moments of high uncertainty. It rewards those who came prepared.

If you were short vol without hedges over the past few weeks, you are likely to experience some rough patches in the days ahead. And while we do not foresee it being as severe as April last year, one must respect the high degree of uncertainty in the air and digest official pieces of information as they come.

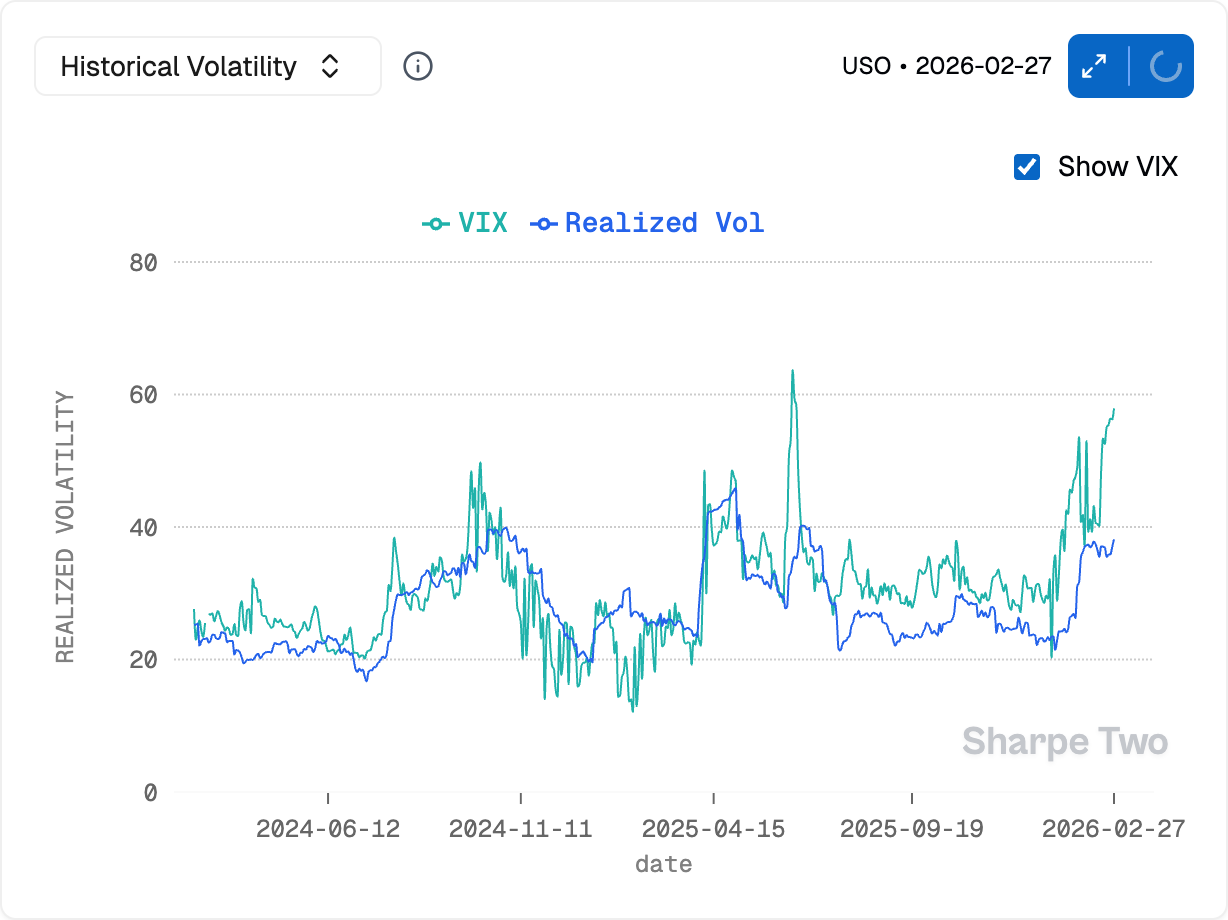

Let us start with those who may have been caught unprepared: implied volatility and demand for options will likely be significantly higher over the next few days. But you do not have to pay extra for the optionality. A delta-one hedge — a short position in equities to offset some of the delta, or an outright long position in USO to offset the directional risk — is often overlooked as a superior and more immediate way to protect your assets.

Take USO: options are already extremely expensive. We certainly do not recommend buying them now. As we said above, you need to think carefully about whether you really need to hedge with options over the next thirty days. Do you have a directional exposure or a volatility exposure? At this stage, while implied vol can certainly go higher, the real pain point is often on the directional side. The same will apply to US equities.

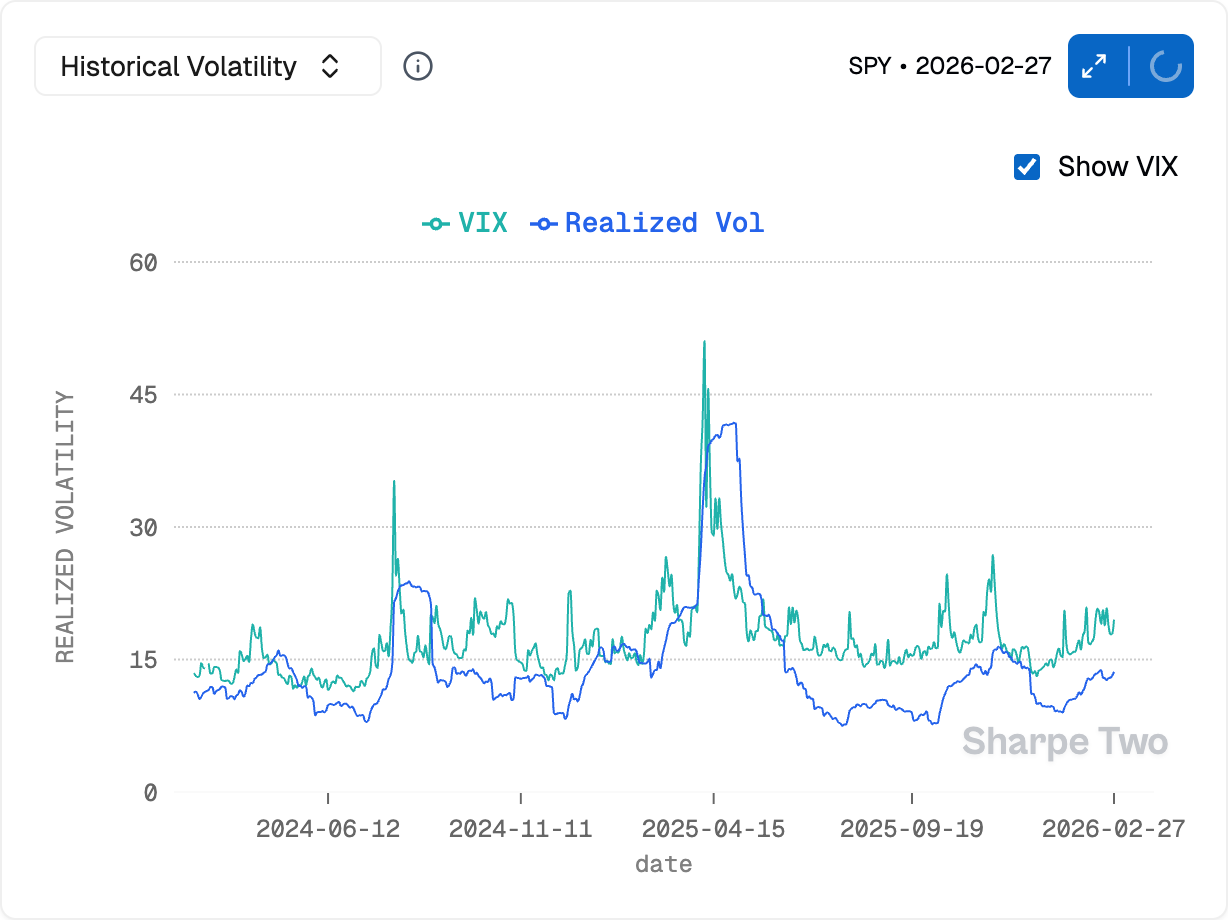

While equities are further removed from the conflict than oil, implied volatility will almost certainly jump to uncomfortable levels for many unprepared sellers over the next few hours. You must assess whether you have a delta problem or a vega problem — and our money, once more, is on delta.

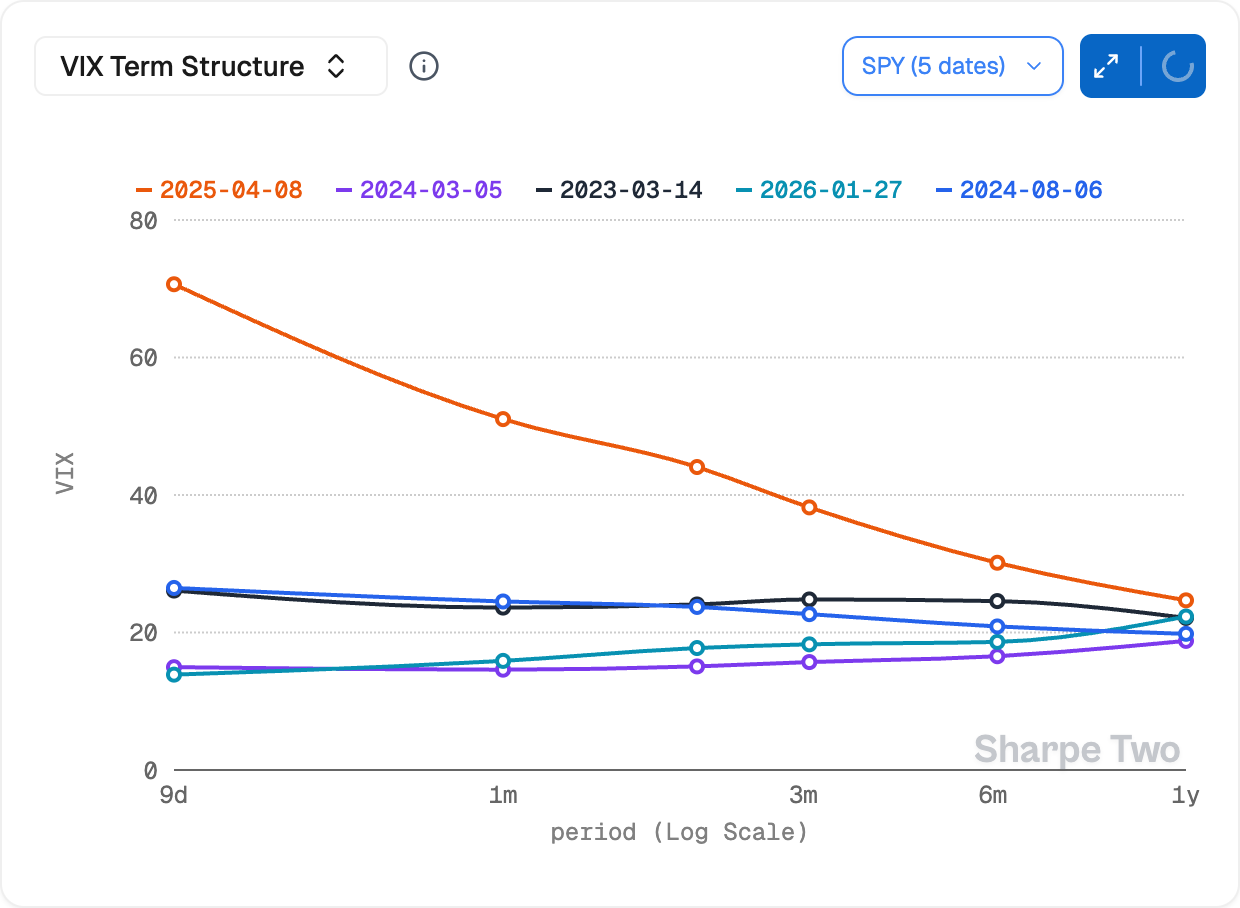

In case you do have a vega problem: the term structure will most likely exhibit backwardation at Monday’s open, and buying front-month options may be ruinously expensive for the risk you are actually trying to hedge. Let us remind you of the dynamics at play: vol spikes, but it also mean-reverts — and in three months from now, it almost certainly will have. Buying the overly expensive front-month is therefore not the best strategy. Those options are already rich, and they carry a high probability of losing value quickly should a resolution emerge — or should the market simply move on, as it always does in wartime.

We brought these term structure charts, exploring a few different periods of recent history, to make the point as clear as day: if you did not buy short-term options ahead of time, you need a serious continuation of the crisis for them to be useful. Otherwise, they will bleed value as time passes — especially now, when realized volatility has not yet caught up. And precisely because realized vol is still somewhat in check, the options at three to six months out remain the ones best positioned to absorb a serious increase in volatility. Their value will not change much on entry nor on exit, you can size up a little, and they may prove useful regardless over the coming months.

Still, it may be tempting to do something in the front months: after all, if the VIX opens at 26 on Monday, it could — with the right catalyst — reach 36 within days. In that case, the counterintuitive yet effective strategy of selling VIX puts is often a great pick. It allows you to be directionally exposed to a rise in volatility while also benefiting if vol comes back down. The goal would not be to profit from it, but simply to exit the insurance contract at no extra cost to your business.

Let us be clear: the environment has been in stressed mode for weeks now, and the latest developments will only raise the temperature. Add to that the domestic concerns around regional banks and potential credit risk in the US, and the marketplace is obviously on edge. In these situations, the goal is not to be a hero. It is to protect your business and your capital, so you are still standing when the dust settles.

And if you had lottery tickets from two months ago, when the VIX was sitting near its lows, Monday and the early part of the week may deliver a handsome payday. Enjoy it while it lasts. Do not fall in love with those wings being deep green — it often does not last. Theta is not your friend when the craziness is at its peak. Monetize them, and reconstruct a balanced portfolio able to weather the incoming storms.

In other news

Jack Dorsey let go of 40% of Block’s workforce overnight on Thursday. Dorsey — one of the legendary founders of Silicon Valley, the talented engineer behind Twitter, and arguably the force behind one of the most significant payment processors of the last 15 years — did not hide behind corporate euphemisms. The business is healthy, he said, but AI and automation allow him to do more with less. He says out loud what other CEOs in tech have been saying politely in different interviews or burying inside broader restructuring plans. Yes, Amazon and Microsoft, we are looking at you.

So — is AI still a bubble? Whatever your opinion on the matter, the transformation it brings starts to feel more real every single day. Anthropic keeps releasing features to the public that are, frankly, mind-blowing regardless of your experience with software engineering, with the promise to now sell work — not just productivity, which was the software industry’s mojo for most of the last two decades.

This did not go unnoticed. The Pentagon tried hard to bring Anthropic into the fold — a lucrative partnership, obviously — which Anthropic refused on ideological grounds. They do not feel comfortable seeing AI, a technology whose scope we cannot fully measure right now, used for mass surveillance or in the pursuit of technological warfare that could lead to the death of people.

Some serious allegations, obviously, about how the Pentagon may be deploying these technologies. And the response from Hegseth was unequivocal: Anthropic is now barred from government contracts. Despite a legal challenge from the company, this could force other US providers to sever ties with Anthropic in the future — a measure normally reserved for companies from adversarial nations like China or Russia.

Yes, ideas can be expensive. And guess who had a very lucrative one? Sam Altman, who raised none of these concerns about how the technology would be used — and won the deal.

What a fantastic way to bring AI openly to the world for the greater good of humanity. Isn’t it, Sam?

Thank you for staying with us until the end. As usual, here are two great reads from last week:

Vibe coding is all the rage, and so is quant vibe coding. We will not lie: we have been happily dabbling in it lately, trying to see where the boundaries of the practice lie. We will report our findings in a few weeks, but in the meantime, we found this piece from Kris particularly à propos. LLMs only know what they have been trained on — and arguably, that is not the best corpus to find edge and test it rigorously. His piece is so good, it is now a safeguard gate in our own LLM stack.

When was the last time you listened to something on Spotify? A few hours ago, if you are like us. It is one of the last businesses we can think of being truly immune to disruption. Yet in this excellent and eye-opening article, we may be much closer to it than we think.

That is it for us. We wish you a peaceful week ahead, and as usual, happy trading.

Ksander