If last week the market showed some hesitation on the direction to take, it left no doubt about where it's heading now — after three weeks of chaos, the S&P 500 closed the week above 5500, adding almost 6%, while the Nasdaq jumped close to 8%, and the VIX dropped back below the 25 mark, closing at 24.89.

At this stage, some important questions are starting to emerge, and the most recurrent of them all is a variation of: Is it all over? If we stick to the data, there’s definitely some credence to it.

First on the headline front — despite Monday's pressure, following weekend rumors that Trump might fire Powell (quickly dismissed by Tuesday night), China and the U.S. seem to agree that a ceasefire in the trade war is probably best for everyone.

The market clearly took notice, and that’s mostly what’s been driving the positive sentiment over the past few days.

But — is it all over yet? Only they know. And until something is actually signed, it’s best to assume that a last-minute reversal is always on the table.

Let’s switch to a more data-driven view.

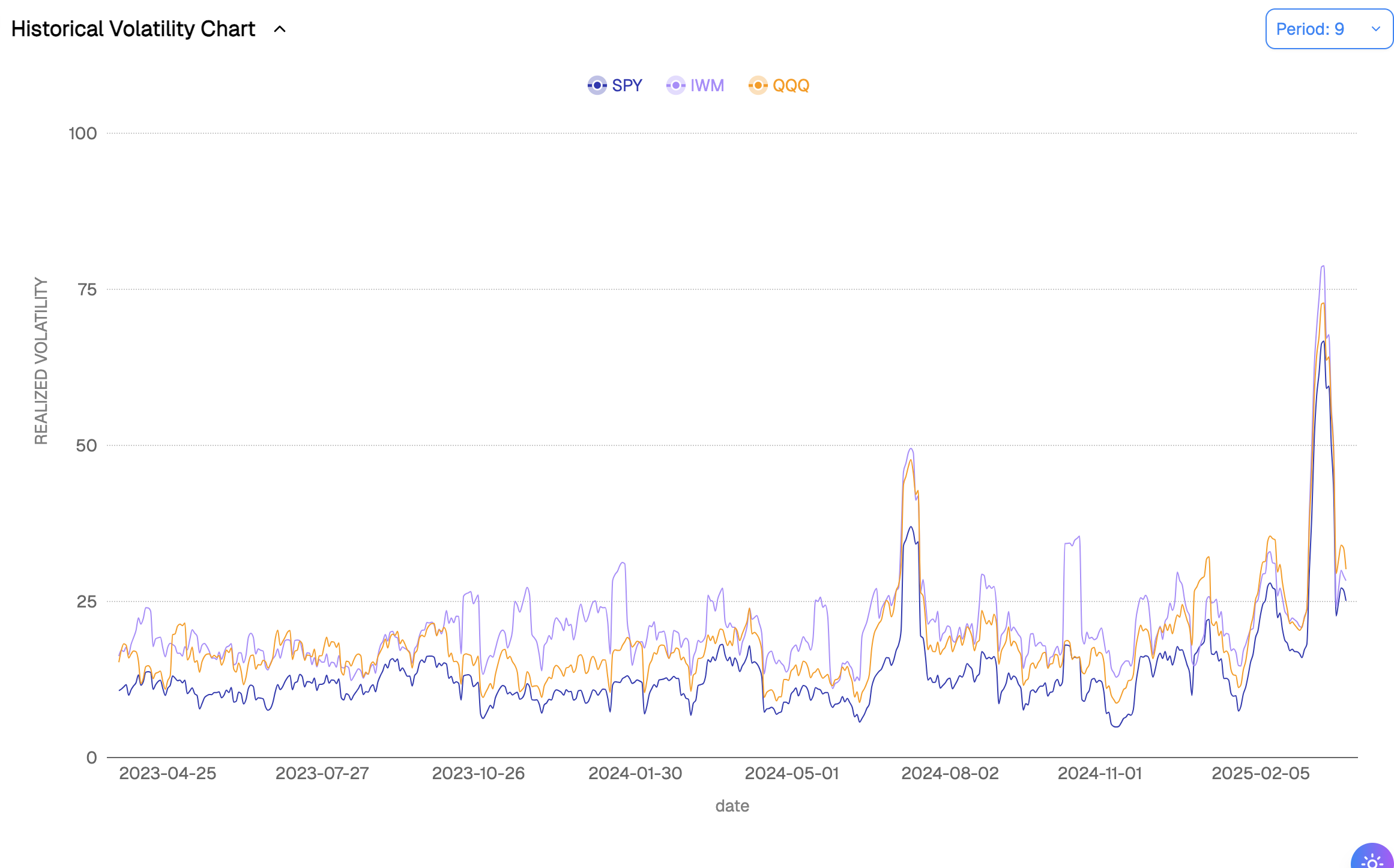

First of all, the 9-day realized volatility across the main ETFs is definitely looking better than a couple of weeks ago. We’re still at the high end of what’s been typical over the past two years — with around 25% realized in the SPY — but the trend is improving.

Yet, the market seems more inclined to believe that realized volatility will keep fading over the next few weeks, rather than accelerating again.

How do we reach this conclusion?

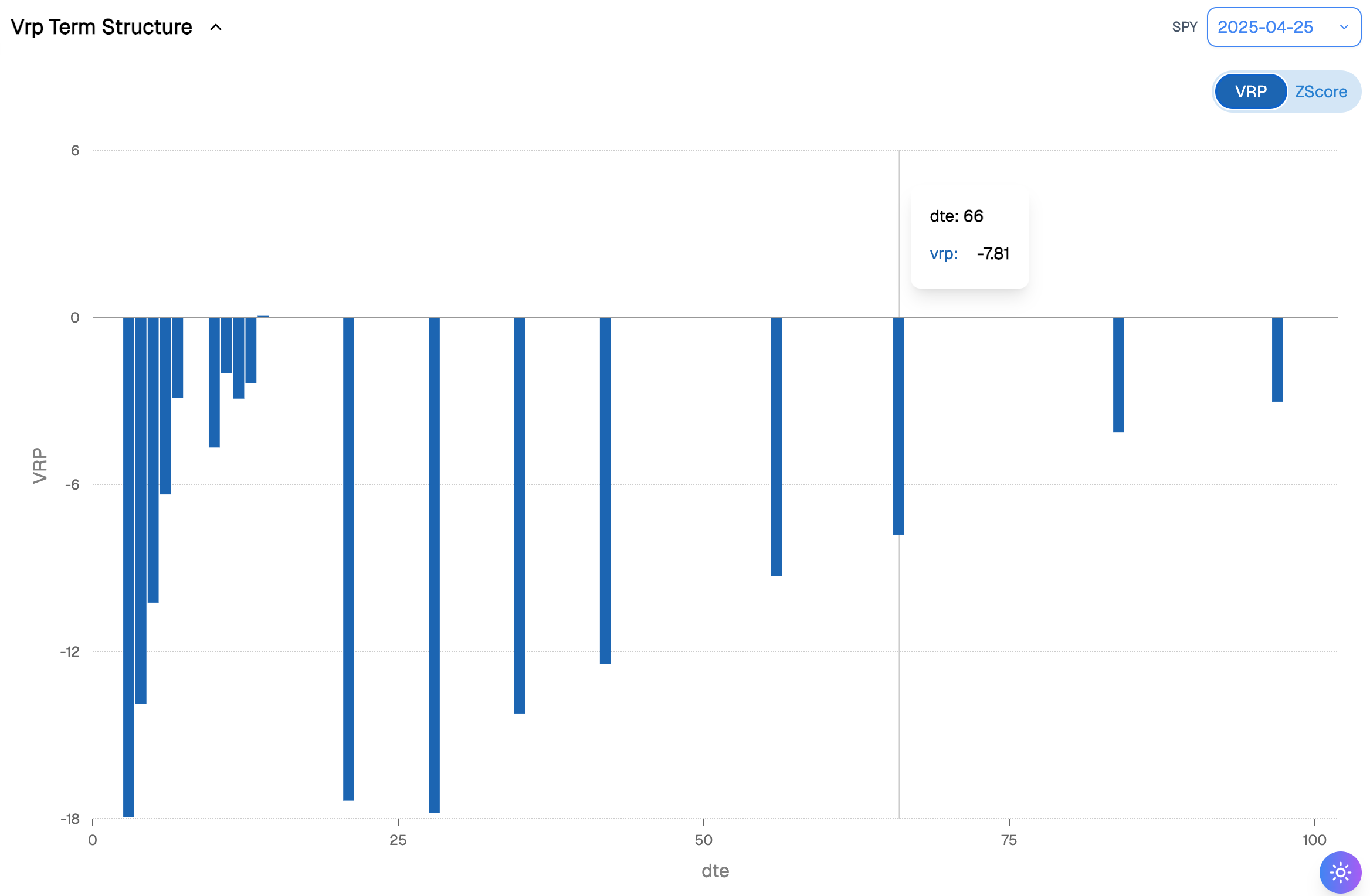

The VRP remains fairly strongly negative across the entire maturity curve.

Don’t get us wrong — under normal circumstances, a negative VRP would have us saying the market may be slightly underestimating risk, and one could easily justify going long volatility.

What changes?

The spike has now been realized. And while it’s not impossible that we spiral down again on another set of terrible headlines, it’s going to be much harder to surprise the market negatively a second time.

Let’s highlight the hypothetical scenarios:

- The Trump administration losing even more credibility by actually firing Powell — extremely unlikely after the strong response earlier this week from President Trump.

- China and the U.S. completely shutting down their trade relationship — unlikely as well, given the current tone.

- A severe deterioration of U.S. economic data.

The last one is key, especially for the retail trading community. When we say severe, we mean severe. Too often we see forums where people complain that the market is rigged because the figure wasn’t good (i.e., lower than expected) and yet the market doesn’t take another impressive/exciting leg on the downside.

The mood is already morose and anxious about the future: unless we see clear signs of meaningful inflation acceleration or an actual recession in the U.S., it’s much more likely the market stays in wait-and-see mode.

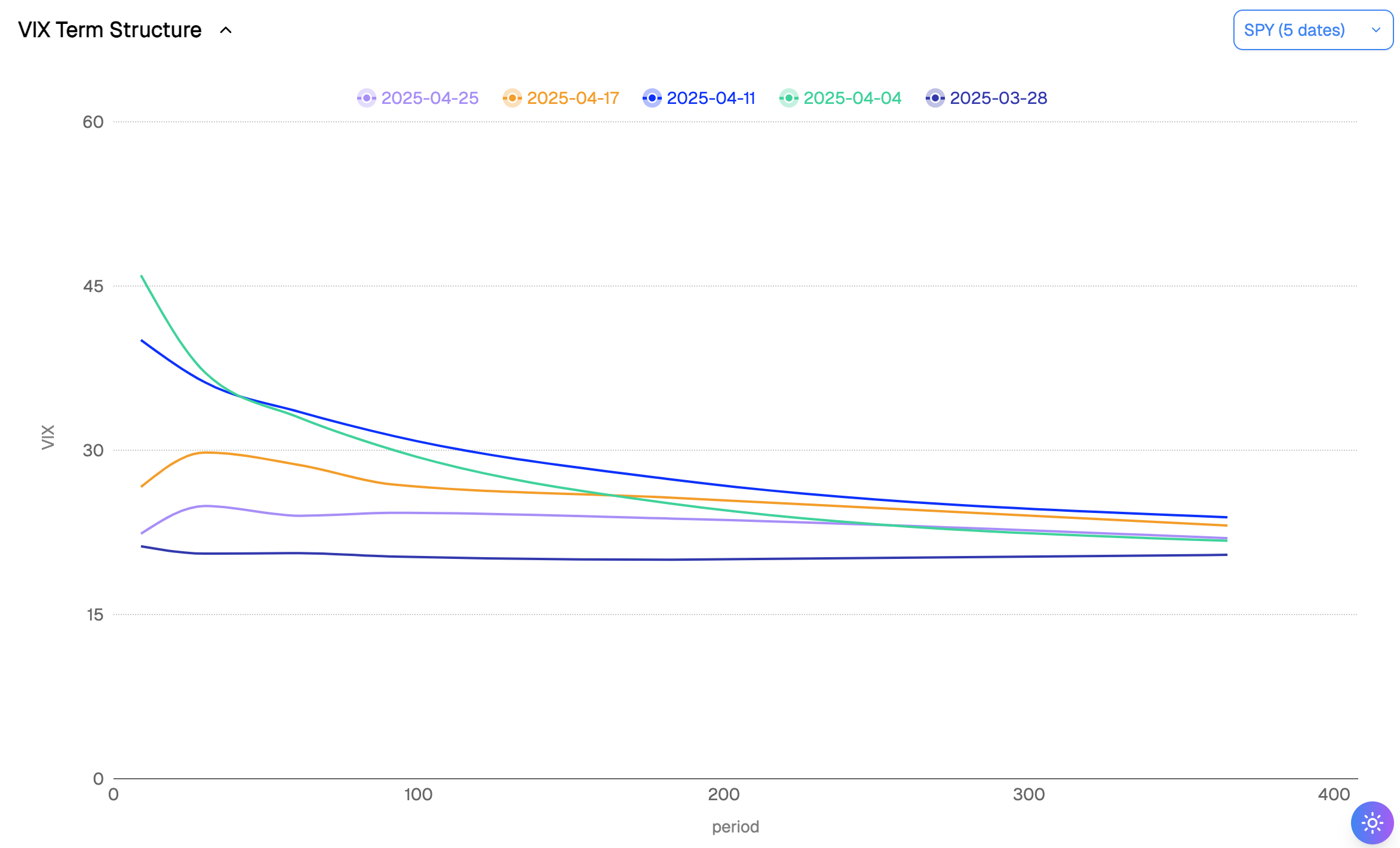

With that in mind, the current term structure for the VIX is totally justified.

Let’s not fall into the trap of seeing a contango where there clearly isn’t one.

The flat-ish shape and the overall level of volatility tell you everything you need to know: the market expects realized volatility to slowly bleed over the next few weeks — but mid-term, nobody knows. And until we get further clarification on all the points mentioned above, we may stay flat like this for a while.

While still slightly more elevated, the term structure now looks much closer to what was priced before Liberation Day than after. So, is it all over?

We’re not saying that either.

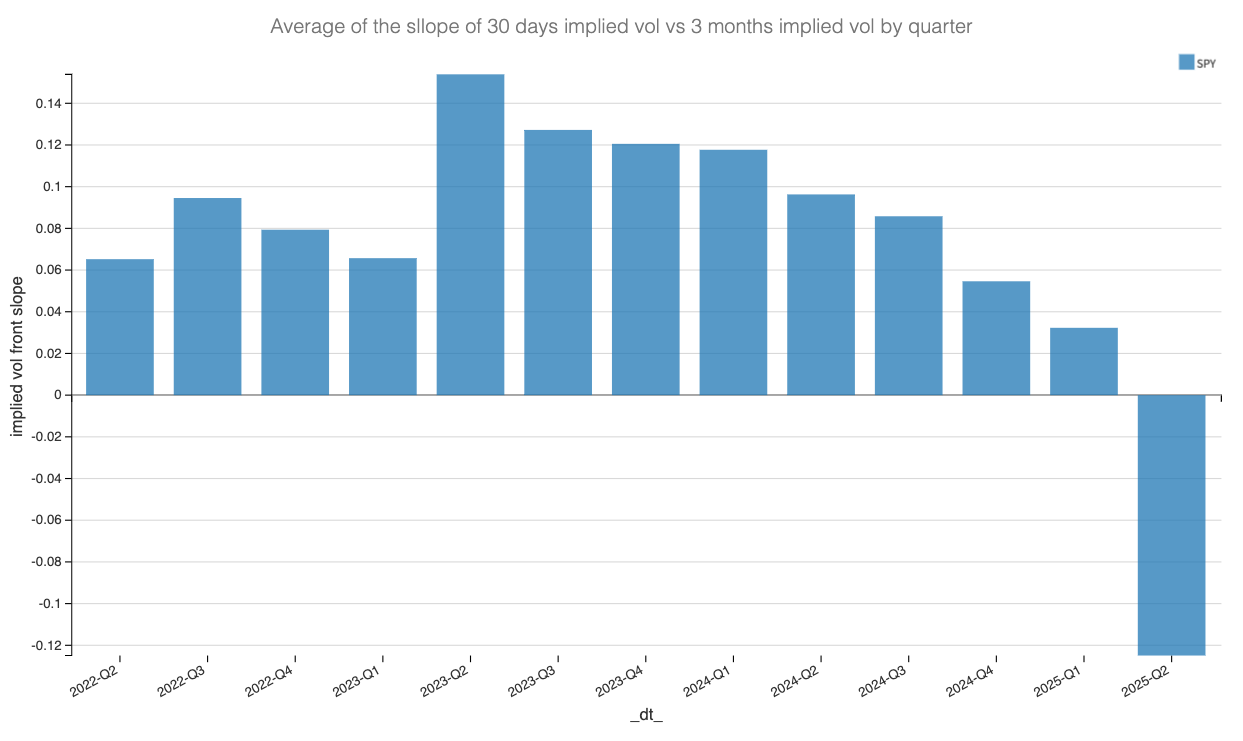

Remember: before the spike, a flat term structure was the default in the months leading into the election — and remained so after: we went from almost 12% on average in the contango between 30 days and 3 months implied volatility to a sporadic 5% in Q4 2024 and even lower in Q1 this year.

It may be better framed as the “Trump disruptor effect,” where short-term volatility trades at a higher premium than the longer end — and for good reason, as we’ve just experienced over the past few weeks.

And while the severe backwardation observed so far in Q2 is more likely to revert back to normal, it leads us to our favorite trades so far in 2025: stay in calendar spreads, yet avoid the short term maturity and focus on selling anything between 1 to 2 months and hedging 3 to 4 months out.

While we do believe realized volatility will slowly fade, the current negative VRP doesn’t justify being outright short straddles or strangles. However, expecting things to slowly but surely normalize over the course of the next few weeks or months is rightly expressed through these longer-term calendar structures.

Naturally, we had to ask the main culprit, who said something along the lines of:

"We don’t actively promote your content. However, it may have been referenced during web research, leading someone to subscribe to your newsletter."

Very interesting — and pretty telling about where big brand budgets might be heading over the next few years.

In fact, according to the FT this weekend, major brands are already spending significant amounts to influence responses given by Claude and ChatGPT — seen as the next frontier for effective SEO.

Does that mean search is dead and Google Ads are a dying breed?

It’s too early to tell, especially as chatbot usage and capabilities continue to evolve almost monthly.

But it’s definitely something investors will be watching closely in Google's earnings.

In the meantime, the giant keeps defying expectations, posting another stellar quarter — including a 10% increase in revenue from its Google Search division.

Thank you for staying with us until the end. As usual, here are a couple of good reads from last week:

- We won’t lie — we tend to stay away from complexity (and deep learning models) when it comes to market analysis.

Yet over the past few months, we’ve seen more and more applications and rigorous testing that make it more than just an intellectual exercise. The latest example comes from , using deep learning to enhance momentum strategies. - And because we can’t seem to spend a week without fixing our own data pipelines to keep bringing meaningful insights to the community, we have to stay in line with the lay of the land. Here’s an excellent piece from Pivotal, exploring the growing moat around data.

That’s it for us this week. We wish you a wonderful (GDP+NFP) week ahead — and, as always, happy trading.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.