Forward Note - 2025/02/02

Ratios and subtle clues.

Out of 52 weeks in a year, our selective memory only keeps a few: when it comes time to recap 2025, this one will undoubtedly be in the top five.

It’s not often that we witness a technological disruption from China shake the foundation of our preconceived notions about U.S. tech dominance. Nor do we regularly hear the world’s long-standing economic leader—one that has thrived on business and trade since the end of the Cold War—suddenly impose tariffs like a mafia boss.

Yet, that’s precisely what happened this week. A 25% levy on its NAFTA neighbors (so much for a free-market agreement), a not-so-subtle warning to its distant cousins, and a 10% tariff on its fiercest competitors—the U.S. has made its stance clear: America first.

From a geopolitical and macroeconomic standpoint, this week could go down in economic textbooks as the official peak of globalization—a turning point that accelerates regionalism, where smaller economic blocs compete fiercely, and mistrust dominates international relations.

That sounds pretty gloomy, doesn’t it? We’ll give you that. Yet, as traders, we firmly believe that understanding what drives market fundamentals is crucial to properly interpreting the data.

Let’s take a concrete example—if I told you that the VIX closed at 16.43 this week, your immediate conclusion would likely be: business as usual, no matter what political shenanigans the powerful are entangled in. And that would be a perfectly reasonable take—when you look at the VIX distribution over the past 20 years, this level is a complete nothing burger.

But what if I told you that the SP500 realized volatility is currently creeping up towards a zone we have seen since 2022? Would that change your perspective?

Markets operate in orderly fashion when the future feels predictable—but when uncertainty creeps in, volatility rises. The fact that the market can’t decide whether it should be buying or ditching assets isn’t a sign of deep conviction. It’s a subtle but clear sign of nervousness.

And that brings us full circle to our opening point—the world is shifting at an increasingly rapid pace, and market participants are feeling it. They’re not sure how to react yet. One day, we hedge. The next, we unwind. Each passing day, that indecision adds another layer of unease.

Here’s another key data point that’s worth paying attention to—VVIX, the implied volatility of VIX options contracts. These contracts serve a specific purpose: they protect against sharp spikes in volatility. So, when VVIX is elevated, it means the market is willing to pay up for that insurance, signaling a heightened fear of volatility surges.

Now, let’s put this into perspective. If you compare the distribution of VVIX levels from 2007 to today, you’ll notice a clear shift in the market’s psychology. Take the 100 level—an arbitrary but relevant threshold:

Since August 2024, a VVIX reading of 100 is barely the 40th percentile.

Compare that to historical data since 2007, where it sits at the 78th percentile.

That’s a major distribution shift. You could dismiss it as a simple aftershock from the big spikes in August and December, assuming the market is just shaking off some nerves. But that would be a dangerous assumption.

Ignoring the subtle cues the market gives you is the first step toward a long and painful journey of losses, inevitably followed by blaming the “deep dark market forces”—the Fed, market makers, Nancy Pelosi, or whatever entity feels like the villain of the day. But here’s the reality: if the market collectively decides it needs to hold volatility hedges, your job isn’t to argue whether it’s right or wrong—it’s to reframe your view of the world accordingly.

Let’s take a step back. How often have you seen the market trade -3% pre-market on a Monday, only to casually rally 200 points and flirt with all-time highs by early Friday? And how often in the past two years have you seen a 1.5% sell-off on the last day of the month—on a Friday, no less?

This isn’t absolute confidence in what’s ahead. This is yet another subtle but important signal—a market on edge, hesitating between embracing risk and hedging against the unknown.

Now that we’ve adjusted our mindset, it’s time for the real game to begin—if VVIX is so expensive, why is VIX still so cheap?

There could be a million reasons, but if we stick to basic supply and demand dynamics, we can simplify the picture into three key points:

People refuse to buy SPX options, an asset that bleeds a little bit every day and hurts performance at the end of the year.

There’s an oversupply of these products: if you believe the volatility space is crowded and options are being dumped into the market, pricing naturally gets suppressed.

A little bit of both.

Whatever the reason, the ratio between VVIX and VIX is currently stretched—not at an all-time high anymore though: it was already flashing red before the DeepSeek saga and has since normalized a bit—but it remains elevated enough to justify selling expensive VIX vol and buying cheap SPX hedge, a position that would have nicely paid off last monday.

Another thing that had us scratching our heads before Friday’s brief sell-off was the contango measured through SPX options (the VIX curve complex: VIX, VIX3M, VIX6M, VIX1Y). It had reached 4 between VIX and VIX6M before the tariff news. Had you looked only at this data point, you would have concluded that the market was fine.

But if you compared it to the VIX futures term structure, the picture got more complicated. The contango between the March and July futures contracts was barely 1. Why would SPX options signal a “normal market” while the futures market wasn’t really buying it?

(Unfortunately, we don’t have a visual for this, so you’ll have to take our word for it.)

But to summarize, we have a market that:

Is buying futures contracts across the term structure,

Refuses to buy SPX options,

While… buying VIX options.

That’s weird enough for us to pay attention.

Deep Seek and the tariffs are unlikely to be the root cause of these market distortions. We started observing them at the very end of 2024, and they only reinforce the idea that market conditions are vastly different from a year ago. Back then, the only real uncertainty was “when is the first rate cut, and how many will follow?”

Now? We’re not even sure if Denmark will still hold Greenland by year-end (sic), nor can we reasonably expect NVDA to remain the most valuable company in the world.

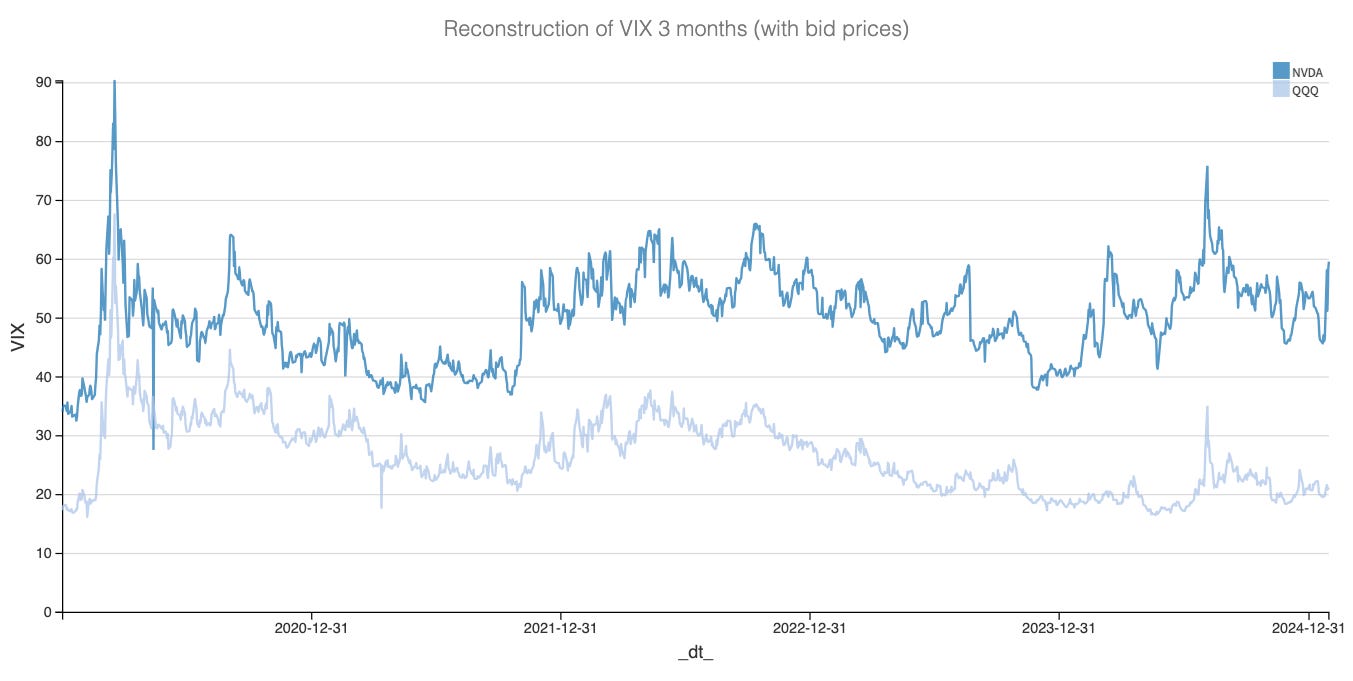

Speaking of which, implied volatility in NVDA at three months is creeping dangerously close to its highest levels in recent years. If we set aside the massive spike last summer, we are now approaching levels last seen in 2022—when every NVDA earnings release sent shockwaves through the entire stock market.

At Sharpe Two, we lean toward nuance, not alarmism: this isn’t a call for doomsday preparation. But uncertainty is undoubtedly building, and the cautious positioning in certain corners of the market should encourage you to do the same.

One final clue—and perhaps the most telling one: how do you reconcile the fact that three-month volatility in NVDA is pushing new highs while three-month volatility in QQQ remains near its lows? One of them is mispriced. Or maybe both.

There’s a world where you sell expensive NVDA strangles and use the proceeds to buy some cheap tails in QQQ—then wait and see. If you truly believe an NVDA crash can happen in isolation, without rippling through the QQQ, you can have a good laugh at our expense. Otherwise, the widening spread between the two deserves your attention.

In other news

Not a single word on the FOMC meeting? Let’s put it this way: Chairman Powell didn’t exactly make it easy for us. As expected, he served up the usual cocktail of boring and data dependency, repeating the carefully rehearsed line: "We are not in a hurry to lower rates."

Yet, with Trump wasting no time in rolling out his economic agenda, that same sentence might now hit differently on Wall Street. Maybe Powell should have at least clarified that he’s also not in a hurry to hike rates—just in case the new administration’s policies prove inflationary.

With that in mind, Friday’s NFP report suddenly carries more weight. If job creation remains strong, the market may start questioning whether the next policy move could, in fact, be in the other direction. And that, right there, could set the tone for the next major price action.

But all that aside, this isn’t even the real story we wanted to highlight in this section.

Buried in a tiny note from the Financial Times, we learned that a Fed official is alleged (with some pretty damning evidence) to have been spying for China for about six years—leaking classified information on the Committee’s rate outlook and economic forecasts. Considering that China holds $786 billion in US debt, you don’t need a PhD in macroeconomics to understand why paying $450k for prime intelligence on your biggest investment is just the cost of doing business.

Yet again, so much for Fed independence, blackout periods, and the illusion that no one, absolutely no one, in the bond market is trading on privileged information. And how, exactly, are we—the little guys—supposed to be 100% certain that last year’s top-performing bond and macro funds didn’t just pay a tiny bit more than the Chinese for the same intel?

After the Bostic scandal last year and the laughably exceptional track record of Nancy Pelosi, it’s getting harder to ignore that something is deeply rotten in the house of the regulators and policy makers.

A side note—this is purely rhetorical speculation on our end. We have nothing but the utmost respect for the money managers in the marketplace and the countless hours they dedicate to research in order to deliver performance for their clients. Likewise, we have no evidence that other Fed members have accepted bribes to share sensitive information.

Thank you for sticking with us until the end. As usual, here are a few great reads from last week:

Everything has been said about DeepSeek, from Ackman’s rather ridiculous interventions to OpenAI crying foul. It’s ironic, really—one built a fortune calling fire on TV (after he bought the insurance, mind you), while the other built its entire tech stack on scrapped web data without paying content creators a dime. Still, here’s the best round-up on the situation we came accress. It is from Michael Spencer and Judy Lin 林昭儀 and every single word is worth it.

And since you clearly haven’t read enough smart takes on DeepSeek—starting with their ArXiv section— Alberto Romero ‘s latest piece on the implications for the U.S.-China tech race is a must-read.

Finally, we live in an era where you can bet on just about anything. Volatility? Of course. Sports? That’s old news. But now, every single geopolitical event is becoming a market. A great article from Scantron invites us to stress a little less about our views and enjoy the world a little more.

That’s it for us this week. We wish you a great (NFP) week ahead.

Oh, and how does the base jumper show up on his first day on Wall Street?

With his wingsuit.

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.