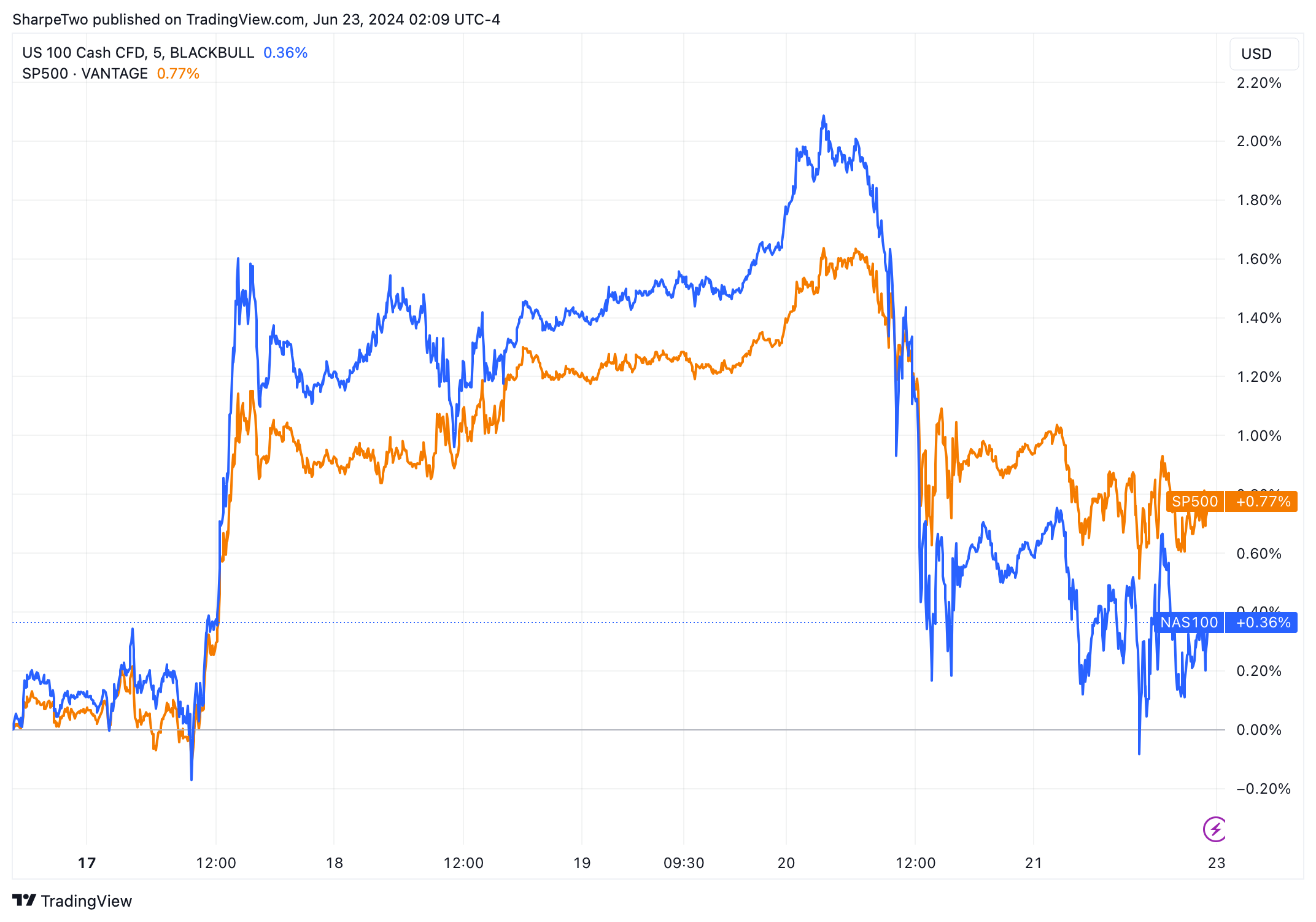

The June quarterly expiration is now behind us and occurred almost in an orderly fashion. "Almost" because many overleveraged long positions may have been caught in the selling pressures observed over Thursday and Friday. Despite the S&P 500 and the Nasdaq 100 closing up for the week at 0.7%, it is "far" from the all-time high on Thursday morning.

The size of NVDA in the indices is such now that you have to consider it to get a clearer picture of your week. With a down move of almost 10% between Thursday morning and Friday's close, the writing was on the wall—there was only a very limited chance to see the market hold its levels.

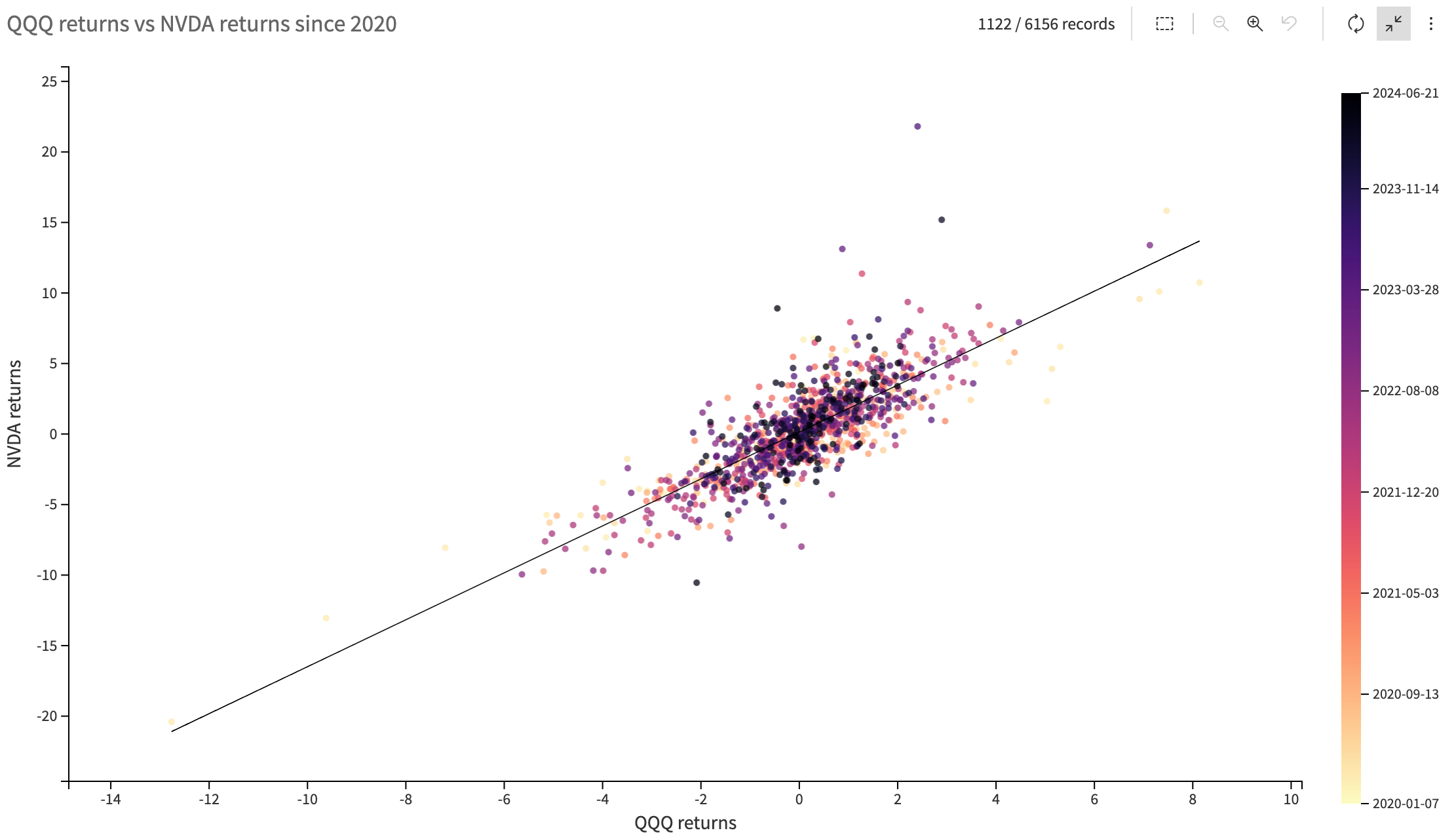

The relationship between the stock and the QQQ is particularly strong, especially now that the periods of heightened volatility from the Covid years and the resulting high inflation are behind us.

Even though we don’t have any rigorous study or data proving our point, there are numerous instances where you can "feel" a reversal or a trend happening in the QQQ based on the intraday movement in NVDA. We are not talking about delays of several hours, but often, a few minutes is all you need to increase your chances of picking the right direction. If you happen to be a data junkie and want to have a go at it, please let us know what you find.

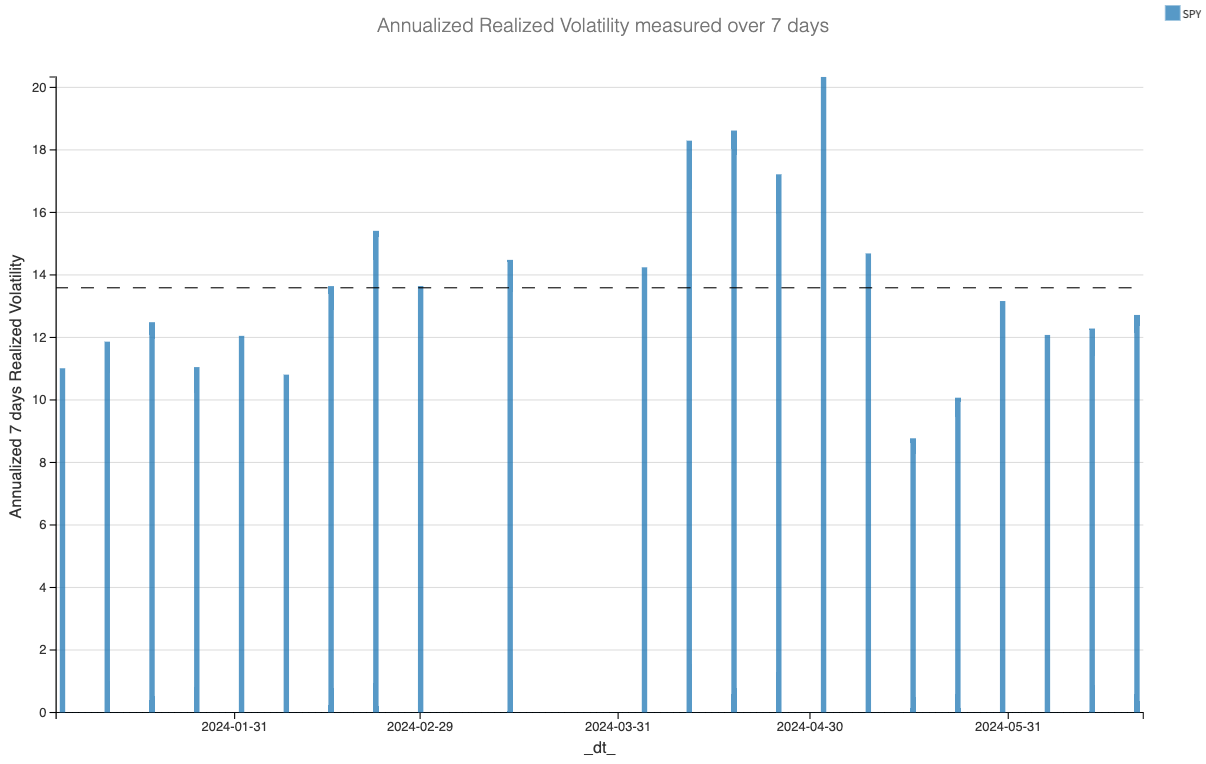

Putting NVDA aside for one second, it was a fairly reasonably quiet week, especially considering it was a quarterly expiration. The realized volatility over seven days in SPY was still below the average of the last six months and right under the median.

So, what’s next? On the macroeconomic front, we have some GDP readings on Thursday, followed by other inflation data. In our Sunday note, we've stated numerous times that we don't think the market is as focused on inflation anymore. However, we will pay attention to the narrative over a potential economic slowdown highlighted by the GDP: the market expects 1.3%, down from 3.4% in the previous reading. It is hard to short an expanding economy. Still, many metrics and analysts consider the equity market expensive—slower growth could certainly contribute to a downshift in sentiment.

This week also marks the end-of-quarter flow, characterized by portfolio rebalancing. Once again, you could observe some interesting developments in the equities or bonds market. Unless you are day trading, we wouldn't read too much into those and instead keep the big picture in mind.

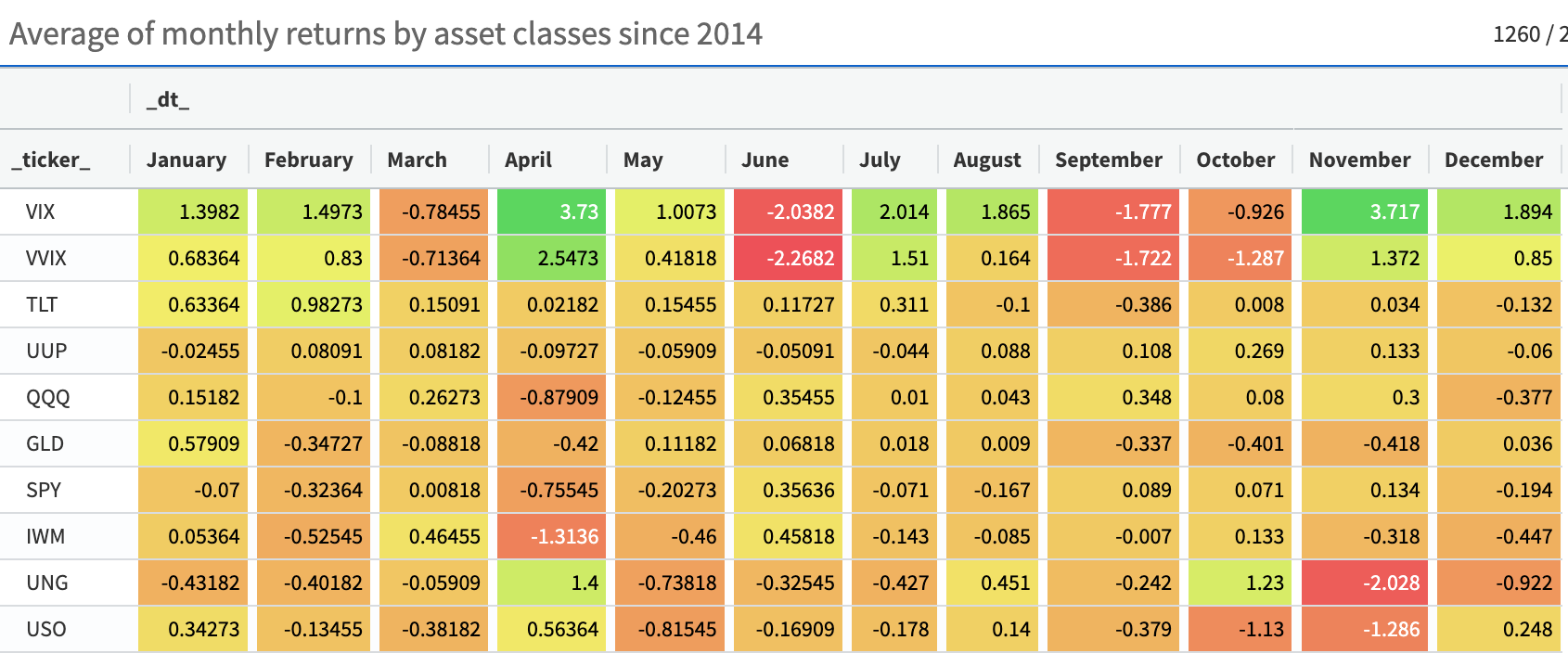

So what’s the view for the summer month? We are on the cusp of the holiday season, and traditionally, realized volatility drops quite a bit in July. However, a current market view is that things often go up in a straight line over the summer. We checked the returns in different asset classes over the past ten years and found interesting results.

First, since 2014, the VIX has, on average, ended up positively throughout the summer, while equities have slightly declined. It’s important to use this information wisely: it doesn’t mean we are betting on a crash this summer. Instead, we are tempering our expectations that everything will be just Pimms and late-night barbecues.

The same is true for the VIX, which ends up being "positive." First, a percentage analysis is never a great way to study the VIX. Second, a 2% increase from 13 is still close… very close to 13. Therefore, do not read this matrix as an invitation to be long on volatility this summer.

That being said, with the race to the final election accelerating and the growing impatience over the first and maybe only rate cut, expected for September, we wouldn’t be surprised if August is a little bit jumpier than what we’ve seen so far this year.

This is all very far in time and speculation at that stage, and for now, the only thing that truly matters is the super-low volatility regime we are in and not quite ready to exit.

Sharpe Two is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

In other news

XLK is a sector ETF giving investors exposure to the tech sector. With the stellar performance of NVDA (up 162% so far this year, 21% in June alone, and down 10% in the last 48 hours — please do not laugh and stay serious until the end of the note), the fund is set to rebalance its holdings: more exposure to NVDA and less to AAPL. This is a logical consequence as NVDA surpassed AAPL in market capitalization.

Therefore, to the condition that NVDA maintains its higher valuation than AAPL by the end of the quarter, XLK managers will need to buy $10 billion of NVDA and sell roughly the equivalent amount of AAPL. Is there a trade here? Perhaps, but it’s curious how much time people spend understanding gamma positioning and dealer flow while overlooking these more predictable market outcomes.

Thank you for staying with us until the end. As usual, here are a few interesting reads from this week:

- Japan is a fascinating country for many in the West (just ask Phil Knight about it), and it has a rich and complex history. published a fantastic review of Fukuzawa's autobiography, an important figure in developing relationships with the West for modern Japan. It's a stunning piece of work.

- It’s easy to see doom and gloom everywhere, and most of the time, we stick to the current market regime. This doesn't mean we should ignore potential risks. In that regard, this analysis from on current fiscal policies is worth checking out.

That’s it for us. We wish you a fantastic week ahead and happy (rebalancing) trading.

Ksander

Data, charts, and analysis are powered by Thetadata and Dataiku DSS.

Have access to our indicators using our API.

Book a consultancy call to talk about the market with us.

Contact at info@sharpetwo.com.

Disclaimer: The information provided is solely informational and should not be considered financial advice. Before selling straddles, be aware that you risk the total loss of your investment. Our services might not be appropriate for every investor. We strongly recommend consulting with an independent financial advisor if you're uncertain about an investment's suitability.